You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- Beyond BeliefDocument4 pagesBeyond Beliefsina.asarniaNo ratings yet

- Money & Banking Project (Best)Document10 pagesMoney & Banking Project (Best)jamilkhannNo ratings yet

- Trading 8.14 Eva WuDocument4 pagesTrading 8.14 Eva WuEvaNo ratings yet

- ECON1192BDocument8 pagesECON1192BLam NguyenNo ratings yet

- Update On Healthcare - March 2021Document3 pagesUpdate On Healthcare - March 2021consilatiotrustNo ratings yet

- SPP Capital Market Update June 2023Document10 pagesSPP Capital Market Update June 2023Jake RoseNo ratings yet

- MentormindDocument23 pagesMentormindSonia GraceNo ratings yet

- 2021 라오스 진출전략Document65 pages2021 라오스 진출전략SunnyNo ratings yet

- Schroders Argentina - Bonos Soberanos Argentinos Hard CurrencyDocument14 pagesSchroders Argentina - Bonos Soberanos Argentinos Hard CurrencyEnzo MayareguaNo ratings yet

- North South University: Economic Conditions of Bangladesh During 1972-2019Document16 pagesNorth South University: Economic Conditions of Bangladesh During 1972-2019Shoaib AhmedNo ratings yet

- Industry Forecast - South Korea Household Characteristics ForecastDocument2 pagesIndustry Forecast - South Korea Household Characteristics ForecastBrandon TanNo ratings yet

- 2020 - An - Inflection - Point - in - Global - Corporate - TaxDocument12 pages2020 - An - Inflection - Point - in - Global - Corporate - Taxds2084No ratings yet

- Analytical Note - Chinas Trading PatternsDocument14 pagesAnalytical Note - Chinas Trading PatternsAnthony TanNo ratings yet

- Week 2 Reading Guide and Practice QuestionsDocument5 pagesWeek 2 Reading Guide and Practice QuestionsCaroline FrisciliaNo ratings yet

- JNJNBNDocument28 pagesJNJNBNrodrigo.santucciNo ratings yet

- Ii, Making LoansDocument10 pagesIi, Making LoansNguyen Ha TrangNo ratings yet

- Across - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFDocument60 pagesAcross - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFQuantDev-MNo ratings yet

- Macroeconomic Data Analysis SG G15 Team 02 Northern Europe and South AsiaDocument25 pagesMacroeconomic Data Analysis SG G15 Team 02 Northern Europe and South AsiaHùng DuyNo ratings yet

- BCG Global PaymentsDocument36 pagesBCG Global PaymentsAdityaMahajanNo ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- Studocu 56304397Document88 pagesStudocu 56304397Fabian Rusmeinka PaneNo ratings yet

- Weekly Economic & Financial Commentary 28octDocument12 pagesWeekly Economic & Financial Commentary 28octErick Abraham MarlissaNo ratings yet

- Bodie Investments 12e PPT CH16Document46 pagesBodie Investments 12e PPT CH16RajonNo ratings yet

- Mgac 1Document7 pagesMgac 1Yah yah yahhhhhNo ratings yet

- Macro FinalDocument14 pagesMacro Finalsteven msusaNo ratings yet

- Interest RatesDocument48 pagesInterest RatesSakshi SharmaNo ratings yet

- QUESTIONSDocument19 pagesQUESTIONSrahidarzooNo ratings yet

- Market Outlook 1705870624Document56 pagesMarket Outlook 1705870624trujo10No ratings yet

- Indonesia Development GoalsDocument12 pagesIndonesia Development Goalstrian hermawanNo ratings yet

- Weekly Economic & Financial Commentary 17junDocument11 pagesWeekly Economic & Financial Commentary 17junErick Abraham MarlissaNo ratings yet

- Debt ProposalsDocument17 pagesDebt ProposalsRoberto DistrilonNo ratings yet

- MACRO + FRA+RISKS - VuHueDocument14 pagesMACRO + FRA+RISKS - VuHueHana VũNo ratings yet

- NG Debt Press Release June 2023 1Document2 pagesNG Debt Press Release June 2023 1Ma. Theresa BerdanNo ratings yet

- Seilern-World-Growth-USD-U-I_EN-Factsheet-as-of-October-30-2023Document3 pagesSeilern-World-Growth-USD-U-I_EN-Factsheet-as-of-October-30-2023catoperinNo ratings yet

- Macrofinancial Linkages Lecture For IFG Lecture Oct 2023Document57 pagesMacrofinancial Linkages Lecture For IFG Lecture Oct 2023drlulu95No ratings yet

- EIFM Tutorial 3Document2 pagesEIFM Tutorial 3Chi YenNo ratings yet

- Investments-Fixed IncomeDocument5 pagesInvestments-Fixed IncomevenugopallNo ratings yet

- Seilern-World-Growth-USD-U-I_EN-Factsheet-as-of-November-30-2023Document3 pagesSeilern-World-Growth-USD-U-I_EN-Factsheet-as-of-November-30-2023catoperinNo ratings yet

- Null 002.2023.issue 121 enDocument26 pagesNull 002.2023.issue 121 enElenita ENo ratings yet

- 2022 Franchising Economic OutlookDocument36 pages2022 Franchising Economic OutlookNguyệt Nguyễn MinhNo ratings yet

- Question Bank - Topic 2 - Time Value of MoneyDocument9 pagesQuestion Bank - Topic 2 - Time Value of MoneyPaolo JoveNo ratings yet

- An Update From Our Cios Transitioning To StagflationDocument11 pagesAn Update From Our Cios Transitioning To Stagflationuwe storzer100% (1)

- BCG - Global Payments 2022Document40 pagesBCG - Global Payments 2022Anupam GuptaNo ratings yet

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Document53 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Committee For a Responsible Federal BudgetNo ratings yet

- Loan Amortization and Compounding vs DiscountingDocument6 pagesLoan Amortization and Compounding vs DiscountingHafiz AbdulwahabNo ratings yet

- DSP Banking & PSU Debt FundDocument1 pageDSP Banking & PSU Debt FundTrivikram AsNo ratings yet

- 7 Step SalesForce CRM March 13 2024Document19 pages7 Step SalesForce CRM March 13 2024resourcesficNo ratings yet

- Global Financial Outlook 1675911594Document57 pagesGlobal Financial Outlook 1675911594yadbhavishyaNo ratings yet

- Econ 116 Problem Set 1 SolutionsDocument4 pagesEcon 116 Problem Set 1 SolutionsCT13No ratings yet

- From The Desk of Business Head and CIO - January 2019: Mr. Prateek AgrawalDocument4 pagesFrom The Desk of Business Head and CIO - January 2019: Mr. Prateek AgrawalAshwin HasyagarNo ratings yet

- Money Market Instrumennts AnalysisDocument5 pagesMoney Market Instrumennts AnalysisManu KrishNo ratings yet

- Historical Mortgage Rates 1970-2020Document11 pagesHistorical Mortgage Rates 1970-2020GoKi VoregisNo ratings yet

- Solid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedDocument4 pagesSolid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedRalph SuarezNo ratings yet

- Finance PaperDocument37 pagesFinance PaperJuan ProsperoNo ratings yet

- Financial Projections Model v6.8.4Document28 pagesFinancial Projections Model v6.8.4george.komnasNo ratings yet

- MF-BB/09/2016/07 Budget Call Circular for 2017-19Document13 pagesMF-BB/09/2016/07 Budget Call Circular for 2017-19sorenttoNo ratings yet

- DCF Model of Bharti Airtel: AssumptionsDocument4 pagesDCF Model of Bharti Airtel: AssumptionsHARSHIL RATHINo ratings yet

- 7 Philippines CRDocument19 pages7 Philippines CRLaura StephanieNo ratings yet

- ACE Advisory Bangladesh Tax Insights 2021 2022Document100 pagesACE Advisory Bangladesh Tax Insights 2021 2022S.M. Hasib Ul IslamNo ratings yet

- Astra Zeneca - D8110C00001 - CSP-v2Document111 pagesAstra Zeneca - D8110C00001 - CSP-v2Urgente24No ratings yet

- Estudio Sobre Respuestas Inmunológicas A Vacunas en Personas Que Ya Tuvieron Covid-19Document5 pagesEstudio Sobre Respuestas Inmunológicas A Vacunas en Personas Que Ya Tuvieron Covid-19Urgente24No ratings yet

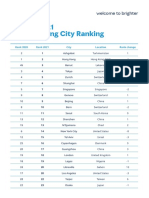

- GL 2021 Cost of Living City Ranking Mercer 0622Document9 pagesGL 2021 Cost of Living City Ranking Mercer 0622Stathis MetsovitisNo ratings yet

- The Lancet Advierte A Gobiernos y Asesores Porqué Ahora La Fase 4 Es Más Importante Que La Fase 3Document3 pagesThe Lancet Advierte A Gobiernos y Asesores Porqué Ahora La Fase 4 Es Más Importante Que La Fase 3Urgente24No ratings yet

- S&F Informe PBA Noviembre 2020.Document20 pagesS&F Informe PBA Noviembre 2020.Urgente24No ratings yet

- FCA Enters Into 6.3 Billion Credit Facility With Intesa SanpaoloDocument3 pagesFCA Enters Into 6.3 Billion Credit Facility With Intesa SanpaoloUrgente24No ratings yet

- Credit Suisse Sobre La Oferta de La ArgentinaDocument3 pagesCredit Suisse Sobre La Oferta de La ArgentinaUrgente24No ratings yet

- Ganadores y Perdedores Según JP MorganDocument10 pagesGanadores y Perdedores Según JP MorganUrgente24No ratings yet

- Canal 9: Falló A Favor de Remigio Ángel González González en Un Litigio Contra El Abogado Carlos Lorefice LynchDocument130 pagesCanal 9: Falló A Favor de Remigio Ángel González González en Un Litigio Contra El Abogado Carlos Lorefice LynchClaudio Andrés De LucaNo ratings yet

- Blackrock - Indicative Debt Restructuring Terms and FrameworkDocument1 pageBlackrock - Indicative Debt Restructuring Terms and FrameworkUrgente24No ratings yet

- Peace To ProsperityDocument181 pagesPeace To ProsperityJoshua Davidovich100% (12)

- Encuesta Sobre La Satisfacción Con La DemocraciaDocument34 pagesEncuesta Sobre La Satisfacción Con La DemocraciaUrgente24No ratings yet

- 2020 World Watch ListDocument68 pages2020 World Watch ListtercerangelNo ratings yet

- El Embargo A Robert BoschDocument3 pagesEl Embargo A Robert BoschUrgente24No ratings yet

- Importante Definición de Sergio MassaDocument1 pageImportante Definición de Sergio MassaUrgente24No ratings yet

- Unclassified Memorandum of Telephone ConversationDocument5 pagesUnclassified Memorandum of Telephone ConversationThe Guardian91% (34)

- Informe Jul19 NacionalDocument30 pagesInforme Jul19 NacionalUrgente24No ratings yet

- La Denuncia Del "Soplón"Document9 pagesLa Denuncia Del "Soplón"Urgente24No ratings yet

- Reigniting Growth in Low-Income en Emerging Market - FMIDocument28 pagesReigniting Growth in Low-Income en Emerging Market - FMIUrgente24No ratings yet

- Elypsis Political Outlook - Pole PositionDocument7 pagesElypsis Political Outlook - Pole PositionUrgente24No ratings yet

- Carta Intendentes A VidalDocument5 pagesCarta Intendentes A VidalUrgente24No ratings yet

- Veeam CDM Report Infographic 2019 ES LATDocument1 pageVeeam CDM Report Infographic 2019 ES LATUrgente24No ratings yet

- ABL Annual Report 2019 LR PDFDocument152 pagesABL Annual Report 2019 LR PDFkrishmasethiNo ratings yet

- Generator Rental AgreementDocument4 pagesGenerator Rental AgreementEneas pollandf75% (4)

- Fake Tata Job Interview Call LetterDocument2 pagesFake Tata Job Interview Call LetterChinmaya Kumar Patra100% (2)

- Supplier Bank DetailsDocument2 pagesSupplier Bank DetailsJoaquina BeloNo ratings yet

- Report On Banking IndustryDocument91 pagesReport On Banking IndustrySachin MittalNo ratings yet

- SCO-06 FeeSched Rev18Document1 pageSCO-06 FeeSched Rev18Marcelo VeronezNo ratings yet

- My MPRDocument58 pagesMy MPRVasundhara BansalNo ratings yet

- DownloadDocument3 pagesDownloadChristina SalliNo ratings yet

- TTMDocument276 pagesTTMRishabh KesharwaniNo ratings yet

- Bank Reconciliation: Prepared By: Nurul Hassanah Binti HamzahDocument9 pagesBank Reconciliation: Prepared By: Nurul Hassanah Binti HamzahNur Amira NadiaNo ratings yet

- Satisfaction Level of Investors With Their Broking FirmDocument81 pagesSatisfaction Level of Investors With Their Broking FirmVijaysinh Parmar50% (2)

- CRISIL Ratings Research Und CRISIL Ratings Rating Scales 2013Document8 pagesCRISIL Ratings Research Und CRISIL Ratings Rating Scales 2013chiragNo ratings yet

- Guaranty and SuretyshipDocument61 pagesGuaranty and SuretyshipFrente ManlapazNo ratings yet

- Ashotosh Bagri e - Post OfficeDocument25 pagesAshotosh Bagri e - Post Officesudheer singhNo ratings yet

- The Canadian Patriot Special: Republic or Colony?Document49 pagesThe Canadian Patriot Special: Republic or Colony?Matthew EhretNo ratings yet

- Question A1: F6 - Taxation (UK)Document38 pagesQuestion A1: F6 - Taxation (UK)osmantaha100% (1)

- Accounting Termini LogyDocument15 pagesAccounting Termini LogyAsif AliNo ratings yet

- Retail Form of Bank of BarodaDocument2 pagesRetail Form of Bank of BarodaVarun SinghNo ratings yet

- Homework Ethics in FinanceDocument4 pagesHomework Ethics in FinanceBby28No ratings yet

- Organization Study On Canara BankDocument77 pagesOrganization Study On Canara Bankmokshasinchana0% (2)

- Laya ClaimDocument2 pagesLaya ClaimManoloNo ratings yet

- General Insurance Quiz For Bank and Insurance Aspirants and IbDocument1 pageGeneral Insurance Quiz For Bank and Insurance Aspirants and Ibnavigatorsoluti7331No ratings yet

- Export ImportDocument10 pagesExport Importgopala_krishna_2No ratings yet

- First Fil-Sin Lending Corp. v. PadilloDocument2 pagesFirst Fil-Sin Lending Corp. v. PadilloCoco Loco100% (1)

- 0452 s18 Ms 12Document14 pages0452 s18 Ms 12Seong Hun LeeNo ratings yet

- Remitly Matteo MazzaDocument4 pagesRemitly Matteo MazzahkbiguivgNo ratings yet

- Saving & Investment Pattern of People in India: A Study OnDocument29 pagesSaving & Investment Pattern of People in India: A Study OnMoumita BeraNo ratings yet

- Understanding warranties in insurance policiesDocument2 pagesUnderstanding warranties in insurance policiesBiboy GSNo ratings yet

- Bangladesh Banking History and SystemDocument10 pagesBangladesh Banking History and SystemmirmoinulNo ratings yet

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet