You might also like

- 14-2001 - Requirements For Tax ExemptionDocument7 pages14-2001 - Requirements For Tax ExemptionArjam B. BonsucanNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- CFA Level I Formula SheetDocument27 pagesCFA Level I Formula SheetAnonymous P1xUTHstHT100% (4)

- GST Return FilingDocument9 pagesGST Return FilingSanthosh K SNo ratings yet

- AP Revised Standard Data 2017-18Document423 pagesAP Revised Standard Data 2017-18dee.angrau76% (25)

- 6.case Study On Input Tax Credit Under GSTDocument17 pages6.case Study On Input Tax Credit Under GSTSUNIL PUJARINo ratings yet

- Caps W 9Document4 pagesCaps W 9api-215255337No ratings yet

- GST Annual Return and AuditDocument10 pagesGST Annual Return and AuditRachit ChhedaNo ratings yet

- Commercial Invoice: Reset FormDocument3 pagesCommercial Invoice: Reset FormBen AliNo ratings yet

- HSC Economics: The Global Economy (Case Study: China)Document12 pagesHSC Economics: The Global Economy (Case Study: China)teresakypham100% (3)

- A Brief Economic History of The WorldDocument29 pagesA Brief Economic History of The Worlddzumbir100% (1)

- Returns GSTDocument25 pagesReturns GSTRahul RockzzNo ratings yet

- GST ReturnDocument7 pagesGST ReturnJCGCFGCGNo ratings yet

- Assignmen GST 5Document10 pagesAssignmen GST 5BhavnaNo ratings yet

- Unit 2 - Part III - Returns Under GST - 30!07!2021Document4 pagesUnit 2 - Part III - Returns Under GST - 30!07!2021Milan ChandaranaNo ratings yet

- GST Returns NotesDocument5 pagesGST Returns NotesvishnureachmeNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- GSTR ReturnDocument136 pagesGSTR Returnyoyorikee0% (1)

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument29 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaManjunathreddy SeshadriNo ratings yet

- Latest Updation in GSTN PortalDocument47 pagesLatest Updation in GSTN PortalVenkat BalaNo ratings yet

- Gstr-2A: TH TH THDocument1 pageGstr-2A: TH TH THTejaswi J DamerlaNo ratings yet

- Indirect Tax Laws 1Document10 pagesIndirect Tax Laws 1GunjanNo ratings yet

- Step by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?Document7 pagesStep by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?arpit jainNo ratings yet

- Day 6 & 7Document23 pagesDay 6 & 7PrasanthNo ratings yet

- Unit 5 GSTDocument3 pagesUnit 5 GSTNishu KatiyarNo ratings yet

- Circular CGST 131 NewDocument5 pagesCircular CGST 131 NewSanjeev BorgohainNo ratings yet

- Returns: FAQ'sDocument25 pagesReturns: FAQ'smun1barejaNo ratings yet

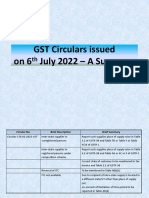

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- GST Return & FilingDocument14 pagesGST Return & Filingjibin samuelNo ratings yet

- FORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedDocument4 pagesFORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedSachin KNNo ratings yet

- GST Returns Assessment and Penal ProvisionsDocument9 pagesGST Returns Assessment and Penal ProvisionsAishuNo ratings yet

- GST Returns and FormsDocument46 pagesGST Returns and FormsSachin KhapareNo ratings yet

- Presentation 09.03.2017 CA - Shivani ShahDocument29 pagesPresentation 09.03.2017 CA - Shivani ShahPARESH KUVADIYANo ratings yet

- GST Pratical ApproachDocument20 pagesGST Pratical ApproachSanthoshNo ratings yet

- Record Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Document16 pagesRecord Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Sha dowNo ratings yet

- Advisory 2710 2Document20 pagesAdvisory 2710 2Pushpraj SinghNo ratings yet

- Concept of Input Tax Credit: © Indirect Taxes Committee, ICAIDocument35 pagesConcept of Input Tax Credit: © Indirect Taxes Committee, ICAIyennamNo ratings yet

- Returns in Goods and Services Tax: Section 37-47 of CGST Act, 2017Document73 pagesReturns in Goods and Services Tax: Section 37-47 of CGST Act, 2017Nikhil PahariaNo ratings yet

- ReturnsDocument12 pagesReturnsPriya DasNo ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument28 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of Indiaatanu karmakarNo ratings yet

- Circular CGST 123Document4 pagesCircular CGST 123AKSHATANo ratings yet

- GST Registration Process and ReturnsDocument7 pagesGST Registration Process and ReturnsAkshay KumarNo ratings yet

- Faqs Viewing Form Gstr-2B Form Gstr-2B: TH TH TH THDocument5 pagesFaqs Viewing Form Gstr-2B Form Gstr-2B: TH TH TH THAsh WNo ratings yet

- Circular No.60Document4 pagesCircular No.60Hr legaladviserNo ratings yet

- Certification DraftDocument47 pagesCertification DraftndNo ratings yet

- GST Returns: BackgroundDocument3 pagesGST Returns: BackgroundPrakash PalanisamyNo ratings yet

- DR - MGR E & RI - Chennai - 28.05.2021-1Document21 pagesDR - MGR E & RI - Chennai - 28.05.2021-1Sha dowNo ratings yet

- Chapter IX of CGST Act Read With CGST Rules, 2017 & Notifications PrescribedDocument26 pagesChapter IX of CGST Act Read With CGST Rules, 2017 & Notifications PrescribedManali PingaleNo ratings yet

- Mygov 1445315831190667 PDFDocument72 pagesMygov 1445315831190667 PDFjitendraktNo ratings yet

- GST - V2 - May 2023Document326 pagesGST - V2 - May 2023FhfhhNo ratings yet

- Chapter 13 - Returns Under GSTDocument11 pagesChapter 13 - Returns Under GSTJay PawarNo ratings yet

- Export of Services in GST RegimeDocument5 pagesExport of Services in GST RegimeNM JHANWAR & ASSOCIATESNo ratings yet

- SPC GST (TDS TCS)Document12 pagesSPC GST (TDS TCS)Aritra BanerjeeNo ratings yet

- Action For Difference in ITC Between 3B and 2ADocument46 pagesAction For Difference in ITC Between 3B and 2Aphani raja kumarNo ratings yet

- Tax Law 2 ProjectDocument16 pagesTax Law 2 Projectrelangi jashwanthNo ratings yet

- Return FormatsDocument56 pagesReturn Formatspuran1234567890No ratings yet

- GST TDS Mechanism - 21062017Document3 pagesGST TDS Mechanism - 21062017Deepak WadhwaNo ratings yet

- Changes in Input Tax Credit Rule 36 (4) in GSTDocument4 pagesChanges in Input Tax Credit Rule 36 (4) in GSTKanhaiya RAthiNo ratings yet

- Refund Forms For Centre and StateDocument20 pagesRefund Forms For Centre and StateShail MehtaNo ratings yet

- Goods and Services Tax Council Standing Committee On Capacity Building and FacilitationDocument61 pagesGoods and Services Tax Council Standing Committee On Capacity Building and FacilitationJeyakar PrabakarNo ratings yet

- Circularno 24 CGSTDocument4 pagesCircularno 24 CGSTHr legaladviserNo ratings yet

- Guidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inDocument4 pagesGuidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inpradeepkumarsnairNo ratings yet

- New Presentation 2Document126 pagesNew Presentation 2prasadtanishquekumarNo ratings yet

- Eturns: After Studying This Chapter, You Will Be Able ToDocument70 pagesEturns: After Studying This Chapter, You Will Be Able ToChandan ganapathi HcNo ratings yet

- Unit 3FDocument21 pagesUnit 3Fbasavaraj nayakNo ratings yet

- Calculation of Tax Liability Assignment: Rishabh KaushikDocument22 pagesCalculation of Tax Liability Assignment: Rishabh KaushikLkNo ratings yet

- Ineligible ITCDocument51 pagesIneligible ITCj84806126No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- ODC Module4 Group7Document26 pagesODC Module4 Group7utkarsh chaudharyNo ratings yet

- Notes For MBA 2Document254 pagesNotes For MBA 2Pramod Vasudev100% (1)

- Croma Juicer WarrantyDocument2 pagesCroma Juicer WarrantyHimanshu YadavNo ratings yet

- Nepal Budget Highlights 2078Document36 pagesNepal Budget Highlights 2078shankarNo ratings yet

- FIN 242 Individual ReportDocument23 pagesFIN 242 Individual ReportNUR SYAMILA MOHD SUKRINo ratings yet

- Exam ReviewDocument87 pagesExam ReviewAdamNo ratings yet

- Audit Under FiscalDocument108 pagesAudit Under FiscalAjay PanwarNo ratings yet

- Materials Management in Voluntary HospitalsDocument20 pagesMaterials Management in Voluntary HospitalsPham PhongNo ratings yet

- Annaprasadam Donor Application 2018 PDFDocument2 pagesAnnaprasadam Donor Application 2018 PDFsureshNo ratings yet

- OCCSTT Short Course - UWI Open Campus SUMMER Online 2021Document26 pagesOCCSTT Short Course - UWI Open Campus SUMMER Online 2021Shamena Hosein0% (1)

- Gross Income 07.01.21Document1 pageGross Income 07.01.21BeaNo ratings yet

- JKT PTI Form For Assets and Liabilities 30 June 2013Document4 pagesJKT PTI Form For Assets and Liabilities 30 June 2013PTI Official100% (4)

- Advanced Taxation - United Kingdom (ATX-UK) : Syllabus and Study GuideDocument26 pagesAdvanced Taxation - United Kingdom (ATX-UK) : Syllabus and Study GuideJonathan GillNo ratings yet

- Mba 3 Sem Tax Planning and Management Kmbfm02 2020Document2 pagesMba 3 Sem Tax Planning and Management Kmbfm02 2020Vinod GuptaNo ratings yet

- Template of Offer LetterDocument2 pagesTemplate of Offer LetterRaj PrasadNo ratings yet

- Tax InvoiceDocument2 pagesTax Invoicearihantjha36No ratings yet

- Agra Final TableDocument4 pagesAgra Final TableJohn Patrick IsraelNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Praveen PujerNo ratings yet

- First Planters Pawnshop v. CIR, G.R. No. 174134, July 30, 2008Document8 pagesFirst Planters Pawnshop v. CIR, G.R. No. 174134, July 30, 2008Emerson NunezNo ratings yet

- Capital Deductions and Value Added Tax 2Document26 pagesCapital Deductions and Value Added Tax 2Nilufar RustamNo ratings yet

- Chapter 07Document27 pagesChapter 07Rollon NinaNo ratings yet

- Holding and SubsidiaryDocument2 pagesHolding and SubsidiaryRizwana BegumNo ratings yet