You might also like

- FeasibilityDocument26 pagesFeasibilitypravmali7No ratings yet

- GTM Marketing Services CatalogueDocument68 pagesGTM Marketing Services CataloguesudiptoNo ratings yet

- Construction Costs: Activities - Core 176 160 Narrative 161 Activities - Elective 179Document30 pagesConstruction Costs: Activities - Core 176 160 Narrative 161 Activities - Elective 179gimasaviNo ratings yet

- CPWD Handbook Office BuildingDocument91 pagesCPWD Handbook Office Buildingexecutive engineer1No ratings yet

- Floor FinishesDocument20 pagesFloor FinishesRatnesh Patel100% (1)

- Building EconomicsDocument20 pagesBuilding EconomicsMahitha Raavi33% (3)

- Bill of Quantities Bill of Quantities (BOQ) :: Specification, Quantity & Costing of Buildings Unit 3Document10 pagesBill of Quantities Bill of Quantities (BOQ) :: Specification, Quantity & Costing of Buildings Unit 3Nidhi Mehta100% (1)

- Materials and Techniques in Low Cost HousingDocument14 pagesMaterials and Techniques in Low Cost HousingNitish Sharma67% (3)

- TOS 1 Unit 3 Transfer of LoadDocument13 pagesTOS 1 Unit 3 Transfer of Loadflower lily100% (1)

- DWG SectionDocument1 pageDWG SectionManish MishraNo ratings yet

- Low Cost Building TechnologiesDocument28 pagesLow Cost Building TechnologiesKriti ModiNo ratings yet

- Low Cost Housing DesignDocument27 pagesLow Cost Housing Designdillishwar bishwaNo ratings yet

- Building Economics PDFDocument133 pagesBuilding Economics PDFHarleen SehgalNo ratings yet

- Banks, Shadow Banking, and FragilityDocument39 pagesBanks, Shadow Banking, and FragilityAdminAliNo ratings yet

- Types of Contracts in ConstructionDocument2 pagesTypes of Contracts in ConstructionAbdul Rahman Sabra100% (2)

- CHAPTER-1 Types of BuildingsDocument32 pagesCHAPTER-1 Types of BuildingsMuaz HararNo ratings yet

- Housing BriefDocument6 pagesHousing BriefManish MishraNo ratings yet

- ABA 2307 Building Economics Notes BATCH 1Document30 pagesABA 2307 Building Economics Notes BATCH 1kent gichuru100% (1)

- 4.2 Factors Affecting Cost Building ElementsDocument18 pages4.2 Factors Affecting Cost Building Elementslucas_haw100% (1)

- Building Economics Int, Role, Scope, ImpDocument17 pagesBuilding Economics Int, Role, Scope, Impritesh100% (1)

- Importance of Building EconomicsDocument7 pagesImportance of Building EconomicsEmime Lee80% (5)

- The Concept of ElasticityDocument11 pagesThe Concept of ElasticityMark Lawrence Lorca FortesNo ratings yet

- Chopra Scm6 Inppt 11Document104 pagesChopra Scm6 Inppt 11Tonmoy RoyNo ratings yet

- Introduction To Building Economics As Related To ArchitectureDocument9 pagesIntroduction To Building Economics As Related To ArchitectureFeritFazliu100% (1)

- Supply Demand Cheat SheetDocument2 pagesSupply Demand Cheat SheetSatz TradesNo ratings yet

- Building Economics Lecture NotesDocument17 pagesBuilding Economics Lecture NotesJackson60% (5)

- Design Variables That Affect Building ConstructionDocument5 pagesDesign Variables That Affect Building ConstructionK_O_Ennin100% (6)

- Building EconomicsDocument20 pagesBuilding EconomicsGurjeet BalNo ratings yet

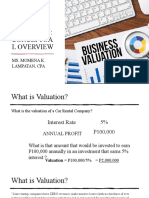

- Conceptual Overview To ValuationDocument23 pagesConceptual Overview To ValuationHazraphine Linso100% (1)

- Methods of Valuation of A BuildingDocument9 pagesMethods of Valuation of A BuildingNanda Kumar100% (1)

- Low Cost Housing TechniquesDocument14 pagesLow Cost Housing TechniquesVarsha bijuNo ratings yet

- Building Economics For Architecture PPT (F)Document54 pagesBuilding Economics For Architecture PPT (F)vaidehi vakil100% (2)

- Chapter Fifteen: Advertising and Public RelationsDocument22 pagesChapter Fifteen: Advertising and Public RelationsNgọc HàNo ratings yet

- Building Materials & Construction TechnologyDocument24 pagesBuilding Materials & Construction TechnologySaurav ShresthaNo ratings yet

- Project On Parle-GDocument21 pagesProject On Parle-GRavi Parmar79% (62)

- Case Study and Analysis of A Low Cost Housing Project in An UrbanDocument8 pagesCase Study and Analysis of A Low Cost Housing Project in An UrbanSteve RichardNo ratings yet

- Cost Estimation: 5.1 Costs Associated With Constructed FacilitiesDocument7 pagesCost Estimation: 5.1 Costs Associated With Constructed FacilitiespriyaarchNo ratings yet

- ARB Student HandbookDocument35 pagesARB Student HandbookManish MishraNo ratings yet

- Analysis of Space Norms For Low Cost Buildings & Laurie BakerDocument17 pagesAnalysis of Space Norms For Low Cost Buildings & Laurie BakerHarsh saxena33% (3)

- Low Rise V/S Medium Rise V/S High Rise in Urban ContextDocument48 pagesLow Rise V/S Medium Rise V/S High Rise in Urban ContextSaasha BambaNo ratings yet

- Building Economics and SociologyDocument138 pagesBuilding Economics and SociologyAnkur Baghel100% (4)

- Cost Effective Costruction TechniquesDocument31 pagesCost Effective Costruction TechniquesbuharimNo ratings yet

- Building Economics NotesDocument2 pagesBuilding Economics Notesneeraja126No ratings yet

- Basic Inputs Into Building ConstructionDocument7 pagesBasic Inputs Into Building ConstructionAnonymous 3hPIuGABNo ratings yet

- Building Economics NotesDocument18 pagesBuilding Economics NotesJacksonNo ratings yet

- Micro Economics Related To Architecture and EngineDocument5 pagesMicro Economics Related To Architecture and EngineMahitha RaaviNo ratings yet

- 1-4 Building Economics and SociologyDocument37 pages1-4 Building Economics and SociologySamreen Khan0% (1)

- Definition of Cost Effective Buildings in Rural and Urban AreaDocument5 pagesDefinition of Cost Effective Buildings in Rural and Urban AreaSmriti SNo ratings yet

- Mud HouseDocument8 pagesMud HouseVarsha KulkarniNo ratings yet

- Non Load Bearing Gypsum BoardsDocument13 pagesNon Load Bearing Gypsum Boardssaahasitha 14No ratings yet

- UNIT 1 Urban Housing PDFDocument68 pagesUNIT 1 Urban Housing PDFAnirudh VijayanNo ratings yet

- Composite WallsDocument41 pagesComposite WallsShivani Snigdha100% (1)

- Course Code: Arl 308 Specifications, Estimation and Costing: Ar. Aditi SharmaDocument27 pagesCourse Code: Arl 308 Specifications, Estimation and Costing: Ar. Aditi Sharmaaditi32100% (1)

- Ar 6016 Unit 3 Conservation PracticeDocument77 pagesAr 6016 Unit 3 Conservation PracticeArjun BS100% (3)

- Professional Practice and EthicsDocument20 pagesProfessional Practice and EthicsHarshene Krishnamurhty100% (1)

- Disaster Management in Context of Vernacular ArchitectureDocument9 pagesDisaster Management in Context of Vernacular ArchitectureHarleenNo ratings yet

- Housing Standards and NormsDocument26 pagesHousing Standards and NormsYuvanshGoelNo ratings yet

- Architectural Project FeasibilityDocument26 pagesArchitectural Project Feasibilityzemran girmaNo ratings yet

- Tubular Steel Monitor Roof Truss - Large Span Constructions - Civil Engineering ProjectsDocument3 pagesTubular Steel Monitor Roof Truss - Large Span Constructions - Civil Engineering ProjectsKranthi Kumar Chowdary ManamNo ratings yet

- Comparative Economic Analysis of Low Rise High Rise BuildingDocument4 pagesComparative Economic Analysis of Low Rise High Rise BuildingJaskiratNo ratings yet

- Modular CoordinationDocument27 pagesModular CoordinationFathima NazrinNo ratings yet

- The Methods of Using Low Cost HousingDocument20 pagesThe Methods of Using Low Cost HousingAamna FatimaNo ratings yet

- Affordable HousingDocument9 pagesAffordable HousingRekha prajapatiNo ratings yet

- Affordable Housing PPT 1Document66 pagesAffordable Housing PPT 1Sanjeev BumbNo ratings yet

- Green Buildings in India Lessons Learnt PDFDocument6 pagesGreen Buildings in India Lessons Learnt PDFAnirudh Jaswal100% (1)

- Professional Practice: Assignment - 1Document18 pagesProfessional Practice: Assignment - 1Sonali SinghNo ratings yet

- Electives Report On Low Cost HousingDocument21 pagesElectives Report On Low Cost HousingSaajan SharmaNo ratings yet

- Internship Training & ReportDocument52 pagesInternship Training & ReportKooi YK100% (1)

- Cidco Low Cost Housing Navi Mumbai: Group MembersDocument45 pagesCidco Low Cost Housing Navi Mumbai: Group Membersprasahnthrk07100% (1)

- Mixed Use Planning in DelhiDocument6 pagesMixed Use Planning in DelhiRuchi SinglaNo ratings yet

- Chapter Two: Financial Analysis 2.1. Scope and Rational For Financial AnalysisDocument16 pagesChapter Two: Financial Analysis 2.1. Scope and Rational For Financial AnalysisWiz Santa100% (1)

- Ders08 - Cost Estimation - YTuDocument89 pagesDers08 - Cost Estimation - YTuJudy HelwaniNo ratings yet

- New Gorakhpur Final - 1-Layout1Document1 pageNew Gorakhpur Final - 1-Layout1Manish MishraNo ratings yet

- Confirming Landuse ChartDocument8 pagesConfirming Landuse ChartManish MishraNo ratings yet

- Orissa High Court Judgement Dated 31012012Document10 pagesOrissa High Court Judgement Dated 31012012Manish MishraNo ratings yet

- Bombay High Court Judgement Dated 11062012Document30 pagesBombay High Court Judgement Dated 11062012Manish MishraNo ratings yet

- Linguistic Code of NationDocument1 pageLinguistic Code of NationManish MishraNo ratings yet

- V3 BOQ Percentage Template 4decimalDocument6 pagesV3 BOQ Percentage Template 4decimalManish MishraNo ratings yet

- Terrace Floor Plan: Scale 1:100Document1 pageTerrace Floor Plan: Scale 1:100Manish MishraNo ratings yet

- CivilDAR 2019 Vol 1Document2 pagesCivilDAR 2019 Vol 1Manish MishraNo ratings yet

- Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal Marks. Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal MarksDocument1 pageNote: - (I) Attempt All Questions. (Ii) Each Question Carries Equal Marks. Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal MarksManish MishraNo ratings yet

- Drinking Water Drinking WaterDocument1 pageDrinking Water Drinking WaterManish MishraNo ratings yet

- Transforming Contemporary Architecture Education in India With Ancient Indian Learning System of GurukulDocument7 pagesTransforming Contemporary Architecture Education in India With Ancient Indian Learning System of GurukulManish Mishra0% (1)

- Prospectus 2013Document30 pagesProspectus 2013Manish MishraNo ratings yet

- AREA APRX. 3000 M : SITE LAYOUT PLAN (Not To Scale)Document1 pageAREA APRX. 3000 M : SITE LAYOUT PLAN (Not To Scale)Manish MishraNo ratings yet

- 2.2 and 2.5 Demand and Linear Demand RSDocument41 pages2.2 and 2.5 Demand and Linear Demand RSSyed HaroonNo ratings yet

- Worlds Population: Chapter 6: Population Growth and Economic DevelopmentDocument10 pagesWorlds Population: Chapter 6: Population Growth and Economic DevelopmentKeYPop FangirlNo ratings yet

- SMM PPT 1Document21 pagesSMM PPT 1Irfan123No ratings yet

- C.B AuditDocument18 pagesC.B Auditamit8615No ratings yet

- Price Analysis of Nike and AdidasDocument8 pagesPrice Analysis of Nike and AdidasDeepanshi Ahuja0% (1)

- Quiz No. 4-2 Entrepreneurship QUIZ NO. 4-2 EntrepreneurshipDocument1 pageQuiz No. 4-2 Entrepreneurship QUIZ NO. 4-2 EntrepreneurshipMutya Neri CruzNo ratings yet

- Forwards and Futures: Futures Exchanges in China, India, and Ethiopia, and E-Choupal in Village IndiaDocument26 pagesForwards and Futures: Futures Exchanges in China, India, and Ethiopia, and E-Choupal in Village IndiaMuhammad AliNo ratings yet

- Introduction On HDFC BankDocument3 pagesIntroduction On HDFC BankAditya Batra50% (2)

- A Framework For Marketing Management: Sixth EditionDocument35 pagesA Framework For Marketing Management: Sixth EditionAbdiasisNo ratings yet

- Strategic Advertising Management: Chapter 5: The Strategic Planning ProcessDocument62 pagesStrategic Advertising Management: Chapter 5: The Strategic Planning ProcessYesfoo Al RiffaayNo ratings yet

- NISM Series XX Taxation in Securities Markets Workbook June 2021Document353 pagesNISM Series XX Taxation in Securities Markets Workbook June 2021Karthick S NairNo ratings yet

- Kotler S SoftDocument238 pagesKotler S SoftMohit LakhotiaNo ratings yet

- Omnichannel Nykaa Rajesh, Mamta, Priyanka, AnupmaaDocument27 pagesOmnichannel Nykaa Rajesh, Mamta, Priyanka, AnupmaaRajesh KumarNo ratings yet

- Mbkuf09 Key8Document7 pagesMbkuf09 Key8rocky_rocks_55No ratings yet

- AkhileshKrishnan (3 1)Document2 pagesAkhileshKrishnan (3 1)Ayisha PatnaikNo ratings yet

- B.A. ProgrammeDocument92 pagesB.A. ProgrammeBhavna MuthyalaNo ratings yet

- Introduction To Ecommerce Lec 1Document14 pagesIntroduction To Ecommerce Lec 1ifra ghaffarNo ratings yet

- Microeconomic Analysis NotesDocument23 pagesMicroeconomic Analysis NotesMinira JafarovaNo ratings yet

- Questionnaire For New Product Development For Pharma CompaniesDocument5 pagesQuestionnaire For New Product Development For Pharma Companiesprofessorchanakya0% (1)

- CFT IchimokuDocument1 pageCFT IchimokuGlenden KhewNo ratings yet

- Measuring and Managing Economic ExposureDocument27 pagesMeasuring and Managing Economic Exposureksinghania98No ratings yet

- A. Contrution Margin 45 B. Contribution Margin Ratio 0.25 C. Break-Even Point in Unit 12.5 D. Break-Even Point in Dollar 2250Document36 pagesA. Contrution Margin 45 B. Contribution Margin Ratio 0.25 C. Break-Even Point in Unit 12.5 D. Break-Even Point in Dollar 2250Bành Đức HảiNo ratings yet