You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- SSP QuestionsDocument15 pagesSSP QuestionsER Shopify0% (2)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Law On Sales ReviewerDocument1 pageLaw On Sales ReviewerNath BongalonNo ratings yet

- Intangible AssetDocument2 pagesIntangible AssetNath BongalonNo ratings yet

- (Ex. Liquors) (Ex. Grape Wine) (Ex. Beer) (Ex. Chewing Tobacco)Document1 page(Ex. Liquors) (Ex. Grape Wine) (Ex. Beer) (Ex. Chewing Tobacco)Nath BongalonNo ratings yet

- Relevant Costing For Non Routine Decision Making - Managment ScienceDocument1 pageRelevant Costing For Non Routine Decision Making - Managment ScienceNath BongalonNo ratings yet

- Introduction To Bank ReconciliationDocument8 pagesIntroduction To Bank ReconciliationNath Bongalon100% (1)

- Recognizing Expenses When Incurred Rather Than When PaidDocument2 pagesRecognizing Expenses When Incurred Rather Than When PaidNath BongalonNo ratings yet

- A Case Study On The Effects of Bullying To Teenagers With Broken FamilyDocument5 pagesA Case Study On The Effects of Bullying To Teenagers With Broken FamilyNath BongalonNo ratings yet

- Sample ProblemDocument5 pagesSample ProblemNath BongalonNo ratings yet

- TiuaonsgtdnDocument2 pagesTiuaonsgtdnNath BongalonNo ratings yet

- 1st PPT GEO3Document17 pages1st PPT GEO3Nath BongalonNo ratings yet

- Dalton's Atomic TheoryDocument2 pagesDalton's Atomic TheoryNath BongalonNo ratings yet

- Learning or Not: Active and Passive ClassesDocument6 pagesLearning or Not: Active and Passive ClassesNath Bongalon60% (5)

- The LithosphereDocument8 pagesThe LithosphereNath Bongalon100% (1)

- 12 Acctg Ed 1 - Notes Receivable PDFDocument17 pages12 Acctg Ed 1 - Notes Receivable PDFNath BongalonNo ratings yet

- Classification of TrianglesDocument4 pagesClassification of TrianglesNath BongalonNo ratings yet

- George Polya: December 1887 - September 1985Document1 pageGeorge Polya: December 1887 - September 1985Nath BongalonNo ratings yet

- 08 Acctg Ed 1 - Bank Reconciliation PDFDocument3 pages08 Acctg Ed 1 - Bank Reconciliation PDFNath BongalonNo ratings yet

- 13 Acctg Ed 1 - Loan ReceivableDocument17 pages13 Acctg Ed 1 - Loan ReceivableNath BongalonNo ratings yet

- 15 Acctg Ed 1 - Receivable Financing 2Document10 pages15 Acctg Ed 1 - Receivable Financing 2Nath BongalonNo ratings yet

- 14 Acctg Ed 1 - Receivable FinancingDocument19 pages14 Acctg Ed 1 - Receivable FinancingNath BongalonNo ratings yet

- 11 Acctg Ed 1 - Estimation of Doubtful Accounts PDFDocument12 pages11 Acctg Ed 1 - Estimation of Doubtful Accounts PDFNath BongalonNo ratings yet

- Auditing Theory - Day 04Document2 pagesAuditing Theory - Day 04Nath BongalonNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsNath BongalonNo ratings yet

- Charles DarwinDocument4 pagesCharles DarwinNath BongalonNo ratings yet

- Triangle Classification: Sides AnglesDocument2 pagesTriangle Classification: Sides AnglesNath BongalonNo ratings yet

- Accounting FOR Partnership SDocument3 pagesAccounting FOR Partnership SNath BongalonNo ratings yet

- Whodoyousayiam? Who Said It?: Chapter/Ve RseDocument3 pagesWhodoyousayiam? Who Said It?: Chapter/Ve RseNath BongalonNo ratings yet

- RECEIVABLESDocument12 pagesRECEIVABLESNath BongalonNo ratings yet

- Taxation New Topics Cpa Borad Exam As of October 2017Document2 pagesTaxation New Topics Cpa Borad Exam As of October 2017Nath BongalonNo ratings yet

- 03 Acctg Ed 1 - Conceptual Framework 2 PDFDocument5 pages03 Acctg Ed 1 - Conceptual Framework 2 PDFNath BongalonNo ratings yet

- MKTG 2126 Syllabus SS 2024Document9 pagesMKTG 2126 Syllabus SS 2024itsandrewabsiNo ratings yet

- HSBC Bank Usa, N.A.: Trade & Supply Chain Foreign Exchange and Risk ManagementDocument13 pagesHSBC Bank Usa, N.A.: Trade & Supply Chain Foreign Exchange and Risk ManagementStephen BgoyaNo ratings yet

- Acc117 AssignmentDocument13 pagesAcc117 AssignmentAIDID IZHAN RUSSELINo ratings yet

- W4 Module 6 Preparation of Financial Statement Part 1Document11 pagesW4 Module 6 Preparation of Financial Statement Part 1leare ruazaNo ratings yet

- Linkedin LimitedDocument16 pagesLinkedin LimitedSameer MhalasNo ratings yet

- Young Entrepreneur From J-K's Shopian Sells Kashmiri Apples Online, Introduces New PackagingDocument1 pageYoung Entrepreneur From J-K's Shopian Sells Kashmiri Apples Online, Introduces New PackagingJatinder SinghNo ratings yet

- Mcdonald'S: CRM AssignmentDocument26 pagesMcdonald'S: CRM AssignmentSOMYA JAISWALNo ratings yet

- 24.02.2023 - Tender For Project Management Consultancy ServicesDocument88 pages24.02.2023 - Tender For Project Management Consultancy ServicesArichandran ANo ratings yet

- Certificate of Incorporation After Change of NameDocument1 pageCertificate of Incorporation After Change of Nameshishirgupta2007No ratings yet

- Geeta Associations & Maharshatra DirectoriesDocument12 pagesGeeta Associations & Maharshatra DirectoriesREACHLaw Chemical Regulatory Training Services0% (1)

- Marketin G MixDocument38 pagesMarketin G MixYada ElNo ratings yet

- Request For Quotation (Apple)Document1 pageRequest For Quotation (Apple)Joseph NoblezaNo ratings yet

- Operation Improvement Plan Report Final Exam Part One Operations Management MM5004Document15 pagesOperation Improvement Plan Report Final Exam Part One Operations Management MM5004Atikah RizkiyaNo ratings yet

- Lesson Plan - ME 3193 - Industrial - ManagementDocument4 pagesLesson Plan - ME 3193 - Industrial - ManagementxoxoNo ratings yet

- Digital Signature 2DB064DCDocument1 pageDigital Signature 2DB064DCAli MustafaNo ratings yet

- Financial: 1, AN INDocument9 pagesFinancial: 1, AN INCity Legal OfficeNo ratings yet

- BCLE 2000C PG 02 Jan2019Document26 pagesBCLE 2000C PG 02 Jan2019myturtle gameNo ratings yet

- Project For Sustainable Electric VehicleDocument2 pagesProject For Sustainable Electric VehicleRui SvenssonNo ratings yet

- Remote Work and Maintaining Employee Motivation - EditedDocument11 pagesRemote Work and Maintaining Employee Motivation - EditedPhillis MwangiNo ratings yet

- ISL Election of Directors and ProfilesDocument12 pagesISL Election of Directors and ProfilesDawood ShaikhNo ratings yet

- Aloe Vera Candy - For GrammarianDocument92 pagesAloe Vera Candy - For GrammarianErne FlorNo ratings yet

- NPV CalculationDocument4 pagesNPV CalculationRajesh1 SrinivasanNo ratings yet

- Marketing NotesDocument22 pagesMarketing NotesPardon SsamsonNo ratings yet

- Internal Marketing Journal PDFDocument26 pagesInternal Marketing Journal PDFIndiani Putri Datik100% (1)

- Check List Inspection Equipements de LevageDocument1 pageCheck List Inspection Equipements de LevageIssam GhannouchiNo ratings yet

- Uppsala Essay: A Critical AnalysisDocument8 pagesUppsala Essay: A Critical AnalysisMainak RayNo ratings yet

- Special CorporationsDocument12 pagesSpecial CorporationsDinah BaluyutNo ratings yet

- Zmot Case Study Travel DomainDocument24 pagesZmot Case Study Travel DomainSameer SippyNo ratings yet

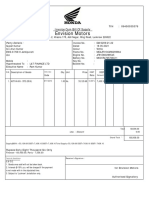

- Envision Motors: Invoice Cum Bill of SupplyDocument1 pageEnvision Motors: Invoice Cum Bill of SupplyEnvision MotorsNo ratings yet