You might also like

- Chapte 2Document58 pagesChapte 2Rabaa DooriiNo ratings yet

- MGT ScienceDocument83 pagesMGT ScienceKyla Renz de LeonNo ratings yet

- Chapter 2 (Big M & Sensitivity)Document25 pagesChapter 2 (Big M & Sensitivity)Yohannes BelaynehNo ratings yet

- Lesson 19 - Applied OptimizationDocument17 pagesLesson 19 - Applied Optimizationallyzamaevaliente012002No ratings yet

- SEO-OPTIMIZED TITLE FOR GRADEUP PERCENTAGE ARTICLEDocument4 pagesSEO-OPTIMIZED TITLE FOR GRADEUP PERCENTAGE ARTICLENupur VarshneyNo ratings yet

- BRAC Linear ProgrammingDocument37 pagesBRAC Linear ProgrammingMohasena MowmiNo ratings yet

- Graphical Method of Solution: Product-Mix ProblemDocument7 pagesGraphical Method of Solution: Product-Mix ProblemSami YNo ratings yet

- BRAC Linear ProgrammingDocument37 pagesBRAC Linear Programmingfireballhunter646100% (1)

- SSG 811 Solution To AssignmentDocument15 pagesSSG 811 Solution To AssignmentSmartLeoMekilisNo ratings yet

- Chapter 3Document22 pagesChapter 3Bereket Desalegn100% (3)

- Solving Mixture and Solution Verbal ProblemsDocument5 pagesSolving Mixture and Solution Verbal Problemsmikeful mirallesNo ratings yet

- Operations Research - Lecture 6 - Linear ProgrammingDocument6 pagesOperations Research - Lecture 6 - Linear ProgrammingIan Ng'Ang'ANo ratings yet

- Linear Programming Examples A Maximization Model ExampleDocument22 pagesLinear Programming Examples A Maximization Model ExampleUTTAM KOIRALA100% (1)

- Linear - Functions - Intersection - of - Straight - Lines Part 2Document26 pagesLinear - Functions - Intersection - of - Straight - Lines Part 2Abhijit NairNo ratings yet

- Chapter 05 Sensitivity Analysis GraphicalDocument7 pagesChapter 05 Sensitivity Analysis Graphicaldalrine rajanNo ratings yet

- 2P1 Linear Programming Graphical Method SC Intro Graphics Blackwater Cases SCxlsDocument46 pages2P1 Linear Programming Graphical Method SC Intro Graphics Blackwater Cases SCxlsRenz ArgarinNo ratings yet

- LP12 Sensitivity AnalysisDocument9 pagesLP12 Sensitivity Analysisjanu2k31No ratings yet

- Quantitative Methods Lecture 4Document22 pagesQuantitative Methods Lecture 4Osman Abdul-MuminNo ratings yet

- 301final SolDocument16 pages301final SolDamas AlexanderNo ratings yet

- Integer Programming Formulation ExamplesDocument16 pagesInteger Programming Formulation ExamplesAlokSinghNo ratings yet

- New Abyssinia CollegeDocument14 pagesNew Abyssinia CollegeE talkNo ratings yet

- Or1 4 LP2Document11 pagesOr1 4 LP2kristian prestinNo ratings yet

- Lecture 3Document22 pagesLecture 3degife deshaNo ratings yet

- Linear Programming ExampleDocument3 pagesLinear Programming Examplecellea98roseNo ratings yet

- Day - 5: Chemistry Class Notes: Biomentors Classes Online, MumbaiDocument4 pagesDay - 5: Chemistry Class Notes: Biomentors Classes Online, MumbaiSmit PatelNo ratings yet

- Permutations and Combinations: Applications of Mulitnomial Theorem and Miscellaneous ProblemsDocument8 pagesPermutations and Combinations: Applications of Mulitnomial Theorem and Miscellaneous ProblemsGURUMARUTHI KUMARNo ratings yet

- Linear ProgrammingDocument17 pagesLinear ProgrammingRahul ChakrabortyNo ratings yet

- Module 1 Lesson 1.2. Graphical MethodDocument9 pagesModule 1 Lesson 1.2. Graphical MethodMaddyyyNo ratings yet

- Linear Programming: Model Formulation and Graphical SolutionDocument13 pagesLinear Programming: Model Formulation and Graphical Solution在于在No ratings yet

- Hmwk1 Solutions WatermarkDocument6 pagesHmwk1 Solutions Watermarkv8p4prncfxNo ratings yet

- Properties of Operations: Converting Fractions To Decimal and Vice VersaDocument20 pagesProperties of Operations: Converting Fractions To Decimal and Vice VersaNeleh IlanNo ratings yet

- Sensityvity AnalysisDocument44 pagesSensityvity AnalysisArnab ShyamalNo ratings yet

- Chapter 2 SlidesDocument55 pagesChapter 2 SlidesaliNo ratings yet

- Chapter 3 Unconstrained OptimizationDocument21 pagesChapter 3 Unconstrained OptimizationRoba Jirma BoruNo ratings yet

- Formula Sheet: Calculating The Mean (Average)Document3 pagesFormula Sheet: Calculating The Mean (Average)jedNo ratings yet

- SolverDocument32 pagesSolverARCHIT KUMARNo ratings yet

- Dual in Linear ProgrammingDocument5 pagesDual in Linear ProgrammingNica BantaNo ratings yet

- PDF 3Document3 pagesPDF 3Quỳnh Anh ShineNo ratings yet

- LP Solved ProblemsDocument5 pagesLP Solved ProblemsAaronLumibao100% (1)

- Lecture 23: Optimization Problems: Today: Applications To Finance and 3D GeometryDocument3 pagesLecture 23: Optimization Problems: Today: Applications To Finance and 3D GeometryRupsayar DasNo ratings yet

- Notes 3Document8 pagesNotes 3Sriram BalasubramanianNo ratings yet

- Lecture 2 (Introduction To LPP)Document29 pagesLecture 2 (Introduction To LPP)Shipra NarauneyNo ratings yet

- Optimization Methods MIT 6.255/15.093 - Fall 2008 Midterm ExamDocument8 pagesOptimization Methods MIT 6.255/15.093 - Fall 2008 Midterm ExamAnup scribdNo ratings yet

- Linear Programming (LP) FundamentalsDocument57 pagesLinear Programming (LP) FundamentalsPratibha GoswamiNo ratings yet

- LPP Graphical and Simplex Method GuideDocument105 pagesLPP Graphical and Simplex Method GuideGirik KhullarNo ratings yet

- OR6205 M9 Practice Exam 2Document5 pagesOR6205 M9 Practice Exam 2Mohan BollaNo ratings yet

- Linear Programming Sensitivity Analysis ExplainedDocument21 pagesLinear Programming Sensitivity Analysis Explainedamanraaj100% (1)

- 14, 42, 61 Or1 LPDocument120 pages14, 42, 61 Or1 LPPaola Pecolera100% (1)

- ECO402 Assignment 1 Solution 2023Document2 pagesECO402 Assignment 1 Solution 2023Rabbani KingNo ratings yet

- Assignment 1Document8 pagesAssignment 1addisNo ratings yet

- Applications of Derivatives in Business and EconomicsDocument6 pagesApplications of Derivatives in Business and EconomicsTed Bryan D. Cabagua100% (1)

- Linear ProgrammingDocument11 pagesLinear ProgrammingNaima PaguitalNo ratings yet

- Chapter - 3: Linear Programming-Graphical SolutionDocument14 pagesChapter - 3: Linear Programming-Graphical SolutionAbhinav AggarwalNo ratings yet

- Operation ResearchDocument21 pagesOperation ResearchEstfnous MeladNo ratings yet

- Linear Equations and Applications, Inequalities and Absolute ValuesDocument22 pagesLinear Equations and Applications, Inequalities and Absolute ValuesEdward John100% (1)

- Post Optimality AnalysisDocument10 pagesPost Optimality AnalysisNabuteNo ratings yet

- Terminology of Solutions For A LP Model: A SolutionDocument17 pagesTerminology of Solutions For A LP Model: A SolutionMohamedAhmedAbdelazizNo ratings yet

- Mathematics of Management NotesDocument51 pagesMathematics of Management Notesraja kashyapNo ratings yet

- Sensitivity analysis insightsDocument4 pagesSensitivity analysis insightsRajesh LambaNo ratings yet

- Chapter - Practical Example of Degeneracy and Vam SolutionDocument18 pagesChapter - Practical Example of Degeneracy and Vam SolutionRajesh LambaNo ratings yet

- Conflict and NegotiationDocument37 pagesConflict and NegotiationRajesh LambaNo ratings yet

- Sensitivity analysis insightsDocument4 pagesSensitivity analysis insightsRajesh LambaNo ratings yet

- Chapter - Pert and CPMDocument29 pagesChapter - Pert and CPMRajesh LambaNo ratings yet

- Chapter - Game TheoryDocument25 pagesChapter - Game TheoryRajesh LambaNo ratings yet

- Minimizing Costs with the Hungarian Assignment MethodDocument37 pagesMinimizing Costs with the Hungarian Assignment MethodRajesh LambaNo ratings yet

- Case StudyDocument27 pagesCase StudyRajesh Lamba100% (2)

- Barriers To CommunicationDocument20 pagesBarriers To CommunicationRajesh LambaNo ratings yet

- Conflict (MBA)Document27 pagesConflict (MBA)Rajesh LambaNo ratings yet

- Barriers To CommunicationDocument16 pagesBarriers To CommunicationRajesh LambaNo ratings yet

- Brand Love - Concept and Dimensions-GibsDocument16 pagesBrand Love - Concept and Dimensions-GibsRajesh LambaNo ratings yet

- Elements of Organizational StructureDocument14 pagesElements of Organizational StructureRajesh LambaNo ratings yet

- Foundation of Individual BehaviorDocument16 pagesFoundation of Individual BehaviorRajesh LambaNo ratings yet

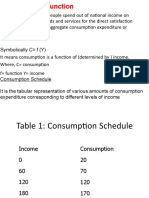

- Consumption Is An Increasing Function of IncomeDocument18 pagesConsumption Is An Increasing Function of IncomeRajesh Lamba100% (1)

- E - Waste Management in IndiaDocument42 pagesE - Waste Management in IndiaRajesh LambaNo ratings yet

- Effective Resume WritingDocument31 pagesEffective Resume WritingRajesh LambaNo ratings yet

- Women Entreprenuership in India (Seminar)Document16 pagesWomen Entreprenuership in India (Seminar)Rajesh LambaNo ratings yet

- OLIGOPOLYDocument20 pagesOLIGOPOLYRajesh LambaNo ratings yet

- Product Mix DecisionsDocument31 pagesProduct Mix DecisionsRajesh LambaNo ratings yet

- Consumer Buying BehaviorDocument29 pagesConsumer Buying BehaviorRajesh Lamba50% (4)

- Objectives of The FirmDocument17 pagesObjectives of The FirmRajesh LambaNo ratings yet

- Barriers To CommunicationDocument16 pagesBarriers To CommunicationRajesh LambaNo ratings yet

- Ocd MbaDocument43 pagesOcd MbaRajesh LambaNo ratings yet

- PMB November 2011 exam timetableDocument9 pagesPMB November 2011 exam timetableNombuso Mbuso Gal Shabangu0% (1)

- For All Sanfoundry MCQ (1000+ MCQ) JOIN Telegram Group : Prev NextDocument368 pagesFor All Sanfoundry MCQ (1000+ MCQ) JOIN Telegram Group : Prev Nextsuraj rautNo ratings yet

- Spaghetti Math Regression ActivityDocument4 pagesSpaghetti Math Regression ActivityjhutchisonbmcNo ratings yet

- Sta 301 NotesDocument9 pagesSta 301 NotesbaniNo ratings yet

- Calculator TipsDocument6 pagesCalculator TipsCNo ratings yet

- TK Solver 5.0 Users Guide PDFDocument766 pagesTK Solver 5.0 Users Guide PDFJustinCaseNo ratings yet

- Fem 9Document22 pagesFem 9tilahun yeshiyeNo ratings yet

- UT Dallas Syllabus For Nats4390.002.11f Taught by Homer Montgomery (Mont)Document9 pagesUT Dallas Syllabus For Nats4390.002.11f Taught by Homer Montgomery (Mont)UT Dallas Provost's Technology GroupNo ratings yet

- Unpacking Worksheets 1 24 12 1Document22 pagesUnpacking Worksheets 1 24 12 1api-316827848100% (1)

- Intr 04Document104 pagesIntr 04Daniel KunstekNo ratings yet

- Arvi Soil Test Reports NewDocument12 pagesArvi Soil Test Reports NewsugumarasbNo ratings yet

- ST 2Document11 pagesST 2yyNo ratings yet

- Integral Calculus Lectures on CatenariesDocument9 pagesIntegral Calculus Lectures on CatenariesJeric PonterasNo ratings yet

- Least Leared Skills 2ND 2018Document10 pagesLeast Leared Skills 2ND 2018marichu_labra_1No ratings yet

- Pen Tool WorksheetDocument3 pagesPen Tool WorksheetHadi RazakNo ratings yet

- Caie As Level: MATHS (9709)Document13 pagesCaie As Level: MATHS (9709)MichelleNo ratings yet

- The Case For The UFO (Unidentified Flying Object) (PDFDrive)Document152 pagesThe Case For The UFO (Unidentified Flying Object) (PDFDrive)Prince Joseph100% (1)

- Hyper Geometric ProbabilityDocument8 pagesHyper Geometric ProbabilitySangita Sangam0% (1)

- Clojure Cheat Sheet (Clojure 1.6 - 1.9, sheet v44Document2 pagesClojure Cheat Sheet (Clojure 1.6 - 1.9, sheet v44Bogdan IvanovNo ratings yet

- Hamilton, Rodrigues, and The Quaternion Scandal: Mathematics MagazineDocument19 pagesHamilton, Rodrigues, and The Quaternion Scandal: Mathematics MagazineG CNo ratings yet

- Mathematical IntuitionDocument23 pagesMathematical IntuitionAnup SaravanNo ratings yet

- Functional Geometry and The Traite de LutherieDocument9 pagesFunctional Geometry and The Traite de Lutheriejsennek100% (1)

- How To Succeed in A College Math ClassDocument4 pagesHow To Succeed in A College Math ClassShashidhar BelagaviNo ratings yet

- Prelim ExamDocument2 pagesPrelim ExamMonica Benitez RicoNo ratings yet

- Tied-State HMMs + Introduction To NN-based AMsDocument37 pagesTied-State HMMs + Introduction To NN-based AMsSammy KNo ratings yet

- APMA1170 HW4 SolutionDocument8 pagesAPMA1170 HW4 Solutionbilo044No ratings yet

- 06 Permutation Combination Revision Notes QuizrrDocument68 pages06 Permutation Combination Revision Notes QuizrrDivyansh KaraokeNo ratings yet

- t13 PDFDocument8 pagest13 PDFMaroshia MajeedNo ratings yet

- October 2017 (IAL) QP - C12 EdexcelDocument48 pagesOctober 2017 (IAL) QP - C12 EdexcelSalman KhanNo ratings yet

- MQ 10 Surds AnswersDocument68 pagesMQ 10 Surds Answershey148No ratings yet