You might also like

- Group Activity: University of People BUS 5110 Group Activity Case StudyDocument11 pagesGroup Activity: University of People BUS 5110 Group Activity Case Studychristian allos100% (15)

- Case Study Unit 5Document4 pagesCase Study Unit 5Hilkiah MusNo ratings yet

- BUS 5113 Group Assignment - Group 0001A - Global Washer and Dryer Manufacturer Case StudyDocument12 pagesBUS 5113 Group Assignment - Group 0001A - Global Washer and Dryer Manufacturer Case StudyPaw Akou-edi100% (2)

- UNIT 1-Written Assignment-BUS 5110Document5 pagesUNIT 1-Written Assignment-BUS 5110Aliyazahra Kamila100% (1)

- BUS 5110 Portfolio Activity Unit-4 BUS 5110 Portfolio Activity Unit-4Document5 pagesBUS 5110 Portfolio Activity Unit-4 BUS 5110 Portfolio Activity Unit-4Emmanuel Gift Bernard100% (3)

- Discussion Assignment Unit-8 BUS 5110Document5 pagesDiscussion Assignment Unit-8 BUS 5110Djahan Rana100% (2)

- Written Assignment Unit 4Document3 pagesWritten Assignment Unit 4कुनाल सिंहNo ratings yet

- Writting - Unit - 5 - Papaya Case Study 1 PDFDocument4 pagesWritting - Unit - 5 - Papaya Case Study 1 PDFFrancis Desoliviers Winner-BluheartNo ratings yet

- Bus 5110 Managerial Accounting Written Assignment Unit 47Document7 pagesBus 5110 Managerial Accounting Written Assignment Unit 47Emmanuel Gift Bernard100% (2)

- Written Assignment Unit 7 Business Law 5115Document7 pagesWritten Assignment Unit 7 Business Law 5115Ola leahNo ratings yet

- Bus 5110 Written Assignment Unit 7Document7 pagesBus 5110 Written Assignment Unit 7KonanRogerKouakouNo ratings yet

- BUS 5110 - Written Assignment - Unit 5 - MADocument5 pagesBUS 5110 - Written Assignment - Unit 5 - MAAliyazahra Kamila100% (1)

- BUS 5110 - Written Assignment - Unit 6Document5 pagesBUS 5110 - Written Assignment - Unit 6Aliyazahra KamilaNo ratings yet

- Unit 1 Written Assignment - Updated VersionDocument6 pagesUnit 1 Written Assignment - Updated VersionSimran Pannu100% (1)

- 5111 Written Assignment Unit 7Document6 pages5111 Written Assignment Unit 7Rachell Ann UsonNo ratings yet

- Written Assignment Unit 5 BUS 5110Document6 pagesWritten Assignment Unit 5 BUS 5110nefelikokNo ratings yet

- Written Assignment Unit 1 - Polly's Pet ProductsDocument3 pagesWritten Assignment Unit 1 - Polly's Pet ProductsJheralene Apple VistroNo ratings yet

- Bus 5111 Financial Management Written Assignment Unit 48Document8 pagesBus 5111 Financial Management Written Assignment Unit 48dinesh kumarNo ratings yet

- BUS 5115 - Unit 2 - Written AssignmentDocument5 pagesBUS 5115 - Unit 2 - Written AssignmentNitesh Shrestha50% (2)

- Bus 5110 Unit 2 AssignmentDocument5 pagesBus 5110 Unit 2 Assignmentwonnetta nicholson0% (1)

- BUS 5115 - PF Unit 4Document5 pagesBUS 5115 - PF Unit 4christian allos100% (3)

- Written Assignment Unit 2 - AANSUDocument6 pagesWritten Assignment Unit 2 - AANSUSamer Sowidan100% (1)

- Written Assignment Unit 6Document8 pagesWritten Assignment Unit 6rony alexander75% (4)

- Bus 5115 Unit 1 Written AssignmentDocument7 pagesBus 5115 Unit 1 Written Assignmentchristian allosNo ratings yet

- Bus 5115 Unit 1 Written AssignmentDocument7 pagesBus 5115 Unit 1 Written Assignmentchristian allosNo ratings yet

- BUS 5115 - PF Unit 4Document5 pagesBUS 5115 - PF Unit 4christian allos100% (3)

- MicroeconomicsDocument1 pageMicroeconomicsJoy Angelique JavierNo ratings yet

- Bus 5110 - Managerial Accounting - Unit 2 - Written AssignmentDocument5 pagesBus 5110 - Managerial Accounting - Unit 2 - Written AssignmentLeslie100% (1)

- Polly's Pet ProductsDocument7 pagesPolly's Pet Productsseles23734No ratings yet

- BUS 5110 Managerial Accounting - Written Assignment Unit 7Document7 pagesBUS 5110 Managerial Accounting - Written Assignment Unit 7LaVida LocaNo ratings yet

- Bus 5110-WK 4-Written AssignmentDocument3 pagesBus 5110-WK 4-Written Assignmentdavid olayiwolaNo ratings yet

- Bus 5110 Discussion Forum Unit 5 SubmissionDocument3 pagesBus 5110 Discussion Forum Unit 5 SubmissionAhmad Hafez100% (1)

- Book1 Group Act5110Document9 pagesBook1 Group Act5110SAMNo ratings yet

- BUS 5110 Managerial Accounting Discussion Assignment Unit 6: Running Head: (Shortened Title Up To 50 Characters) 1Document5 pagesBUS 5110 Managerial Accounting Discussion Assignment Unit 6: Running Head: (Shortened Title Up To 50 Characters) 1Emmanuel Gift Bernard0% (1)

- BUS 5110 - Managerial Accounting - Written Assignment Unit 4Document5 pagesBUS 5110 - Managerial Accounting - Written Assignment Unit 4Leslie100% (2)

- Bus 5111 Discussion Assignment Unit 2Document2 pagesBus 5111 Discussion Assignment Unit 2Sheu Abdulkadir Basharu100% (1)

- Written Assignment Unit01Document6 pagesWritten Assignment Unit01Michael Aboelkhair100% (1)

- BUS 5115 Unit 4 Portfolio Activity - Docx-SampleDocument5 pagesBUS 5115 Unit 4 Portfolio Activity - Docx-SampleRamy ahmed0% (1)

- BUS 5110 Portfolio Activity Unit 5 BUS 5110 Portfolio Activity Unit 5Document5 pagesBUS 5110 Portfolio Activity Unit 5 BUS 5110 Portfolio Activity Unit 5ifeanyi ukachukwuNo ratings yet

- Income, Cash Flow, and Balance Sheet For Polly's Pet ProductsDocument3 pagesIncome, Cash Flow, and Balance Sheet For Polly's Pet ProductskashNo ratings yet

- Unit 2 Second PortfolioDocument3 pagesUnit 2 Second PortfolioSimran PannuNo ratings yet

- Written Assignment - BUS 5115 - Week 4Document8 pagesWritten Assignment - BUS 5115 - Week 4christian allos100% (1)

- BUS 5110 Written Assignment Unit 7 DoneDocument7 pagesBUS 5110 Written Assignment Unit 7 DoneSimran PannuNo ratings yet

- Written Assignment Unit 3 BUS 5115-01Document7 pagesWritten Assignment Unit 3 BUS 5115-01modar KhNo ratings yet

- Written Assignment Unit 2-Bus5110Document4 pagesWritten Assignment Unit 2-Bus5110Franklyn Doh-Nani100% (1)

- Portfolio Activity Unit 5 University of The PeopleDocument5 pagesPortfolio Activity Unit 5 University of The Peoplechristian allosNo ratings yet

- BUS 5111 - Financial Management - Written Assignment Unit 4Document5 pagesBUS 5111 - Financial Management - Written Assignment Unit 4LaVida LocaNo ratings yet

- BUS 5110 - Assignment 1Document6 pagesBUS 5110 - Assignment 1michelle100% (1)

- BUS 5110 Assignment Unit 7Document7 pagesBUS 5110 Assignment Unit 7Charles Irikefe100% (1)

- Bus 5110 Managerial Accounting Written Assignment Unit 74 PDFDocument10 pagesBus 5110 Managerial Accounting Written Assignment Unit 74 PDFEmmanuel Gift BernardNo ratings yet

- BUS 5110 Port. Act Unit 7Document3 pagesBUS 5110 Port. Act Unit 7christian allos100% (3)

- Writting Assignement Unit 7Document2 pagesWritting Assignement Unit 7Paw Akou-ediNo ratings yet

- Bus 5113 - Unit 4 BREAKTHROUGH IMPROVEMENT PLAN CASEDocument4 pagesBus 5113 - Unit 4 BREAKTHROUGH IMPROVEMENT PLAN CASEmynalawal50% (2)

- Bus 5111 Discussion Assignment Unit 6Document2 pagesBus 5111 Discussion Assignment Unit 6Sheu Abdulkadir Basharu33% (3)

- Assignment 5Document3 pagesAssignment 5Hilkiah MusNo ratings yet

- University of The People: BUS 5110 Managerial Accounting Portfolio Assignment 6Document4 pagesUniversity of The People: BUS 5110 Managerial Accounting Portfolio Assignment 6Emmanuel Gift BernardNo ratings yet

- BUS 5113 Group 46C Activity Project (Hiring Selection Case) - Draft 2Document13 pagesBUS 5113 Group 46C Activity Project (Hiring Selection Case) - Draft 2Khadijat SmileNo ratings yet

- BUS 5111 - Financial Management - Written Assignment Unit 3Document5 pagesBUS 5111 - Financial Management - Written Assignment Unit 3LaVida LocaNo ratings yet

- BUS 5115 - WK 3 - Written AssignmentDocument4 pagesBUS 5115 - WK 3 - Written AssignmentEzekiel Patrick100% (1)

- Bus 5111 Discussion Assignment Unit 7 18Document8 pagesBus 5111 Discussion Assignment Unit 7 18ifeanyi ukachukwu100% (1)

- Written Assignment Unit 3Document6 pagesWritten Assignment Unit 3Aby ZuñigaNo ratings yet

- BUS 5110 Managerial Accounting - Written Assignment Unit 5Document5 pagesBUS 5110 Managerial Accounting - Written Assignment Unit 5LaVida LocaNo ratings yet

- BUS 5110 - Written Assignment Unit 5Document5 pagesBUS 5110 - Written Assignment Unit 5Yusuf Gbenga AyodeleNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Written Assignment Unit 1Document6 pagesWritten Assignment Unit 1christian allosNo ratings yet

- Written Assignment - BUS 5115 - Week 4Document8 pagesWritten Assignment - BUS 5115 - Week 4christian allos100% (1)

- Ethics in Finance: University of PeopleDocument5 pagesEthics in Finance: University of Peoplechristian allosNo ratings yet

- Portfolio Activity Unit 5 University of The PeopleDocument5 pagesPortfolio Activity Unit 5 University of The Peoplechristian allosNo ratings yet

- BUS 5110 Port. Act Unit 7Document3 pagesBUS 5110 Port. Act Unit 7christian allos100% (3)

- Bus 5115 - Discussion Forum Unit 1 University of The PeopleDocument5 pagesBus 5115 - Discussion Forum Unit 1 University of The Peoplechristian allosNo ratings yet

- BUS 5110 - PA Unit 6Document6 pagesBUS 5110 - PA Unit 6christian allosNo ratings yet

- BUS 5110 Port. Act Unit 7Document3 pagesBUS 5110 Port. Act Unit 7christian allos100% (3)

- Quadratic Equations - MathigonDocument4 pagesQuadratic Equations - MathigonJemeraldNo ratings yet

- Drug Supply Management-Participants ManualDocument153 pagesDrug Supply Management-Participants ManualClara Undap100% (1)

- MKTG1025 Week8 TutorialDocument31 pagesMKTG1025 Week8 TutorialMagedaNo ratings yet

- Road Construction DUPADocument277 pagesRoad Construction DUPARhodwillNo ratings yet

- Do Global Factors Impact Bitcoin PricesDocument39 pagesDo Global Factors Impact Bitcoin Pricesnannous1986No ratings yet

- Tesla Capital RaiseDocument89 pagesTesla Capital RaiseFred LamertNo ratings yet

- Tender 2388Document93 pagesTender 2388atulchurchaNo ratings yet

- Cambridge Assessment International Education: EconomicsDocument21 pagesCambridge Assessment International Education: Economicsganza.dorian.sNo ratings yet

- Chapter 5Document26 pagesChapter 5Deep ShahNo ratings yet

- Compensation Plan: RomaniaDocument11 pagesCompensation Plan: RomaniaAlex VimanNo ratings yet

- DIEDRICHSEN-On Surplus Value in ArtDocument18 pagesDIEDRICHSEN-On Surplus Value in ArtramblingunitNo ratings yet

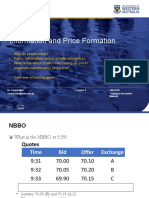

- Information and Price FormationDocument36 pagesInformation and Price FormationDylan AdrianNo ratings yet

- Ib Economics GlossaryDocument10 pagesIb Economics GlossaryValeriia IvanovaNo ratings yet

- Ebay Consumer BehaviorDocument13 pagesEbay Consumer BehaviordharitridalviNo ratings yet

- Dana - 1Document47 pagesDana - 1Dana Denisse RicaplazaNo ratings yet

- Preview: Walden UniversityDocument24 pagesPreview: Walden UniversityHodan HaruriNo ratings yet

- Practiceproblem1 23839Document3 pagesPracticeproblem1 23839Karamveer SinghNo ratings yet

- International Business - Who Make The Apple's IphoneDocument2 pagesInternational Business - Who Make The Apple's IphoneTito R. GarcíaNo ratings yet

- SBI3Document31 pagesSBI3bhaskarrao01No ratings yet

- Case Study Analysis: Team: Zeus ThunderboltDocument3 pagesCase Study Analysis: Team: Zeus ThunderboltSIDDHANT SWAIN100% (1)

- Managerial Economics AssignmentDocument17 pagesManagerial Economics AssignmentDeepshikha Gupta50% (2)

- Market Equilibrium AnswersDocument35 pagesMarket Equilibrium Answerschandanays323No ratings yet

- Cec 004 NotesDocument4 pagesCec 004 NotesChastity LoveNo ratings yet

- The Implementation of Target Costing in The United States: Theory Versus PracticeDocument14 pagesThe Implementation of Target Costing in The United States: Theory Versus PracticeAldi SBPNo ratings yet

- Kanpur Confectionaries BP0268A PDFDocument7 pagesKanpur Confectionaries BP0268A PDFAditya MehraNo ratings yet

- Relevance of Economics in LawDocument30 pagesRelevance of Economics in LawsamNo ratings yet

- Chips & Chicken GuideDocument28 pagesChips & Chicken GuideMatata MuthokaNo ratings yet

- Quiz No. 1 Discount SeriesDocument2 pagesQuiz No. 1 Discount SeriesAngelicaHermoParas100% (1)

- Latihan Bab 9Document2 pagesLatihan Bab 9Lanang TanuNo ratings yet