You might also like

- Bodie Essentials of Investments 12e Chapter 05 PPT AccessibleDocument37 pagesBodie Essentials of Investments 12e Chapter 05 PPT AccessibleEdna DelantarNo ratings yet

- Documentary Requirements: Estate TaxDocument19 pagesDocumentary Requirements: Estate TaxAubrey CaballeroNo ratings yet

- Bruhat Bangalore Mahanagara Palike: Revenue Department Frequently Asked QuestionsDocument2 pagesBruhat Bangalore Mahanagara Palike: Revenue Department Frequently Asked Questionsnayansharma19485No ratings yet

- Procedures For Filing of ESTATE TAXDocument2 pagesProcedures For Filing of ESTATE TAXJennylyn Biltz AlbanoNo ratings yet

- Tax Rates Effective January 1, 1998 Up To PresentDocument8 pagesTax Rates Effective January 1, 1998 Up To PresentJasmin AlapagNo ratings yet

- How To Obtain Solvency CertificateDocument3 pagesHow To Obtain Solvency Certificatebonniga2001100% (2)

- Annual Information Return For High Value Financial Transactions' - An OverviewDocument2 pagesAnnual Information Return For High Value Financial Transactions' - An OverviewAbhinav GuptaNo ratings yet

- For Taxable Year 2008, The Following Transitory Personal and Additional Exemptions Shall Be UsedDocument2 pagesFor Taxable Year 2008, The Following Transitory Personal and Additional Exemptions Shall Be UsedCk Bongalos AdolfoNo ratings yet

- Estate Tax RatesDocument5 pagesEstate Tax RatesJohn Carlos WeeNo ratings yet

- Sponsored By:: The Chanrobles GroupDocument9 pagesSponsored By:: The Chanrobles Groupbaby.torpee9117No ratings yet

- Agree-Bop 2019 Final DraftDocument12 pagesAgree-Bop 2019 Final DraftKwasi AdarkwaNo ratings yet

- RMC No. 68-2019 - DigestDocument3 pagesRMC No. 68-2019 - DigestAMNo ratings yet

- Tax Rates Description Tax Form Documentary Requirements Procedures Deadlines Related Revenue Issuances Codal Reference Frequently Asked QuestionsDocument10 pagesTax Rates Description Tax Form Documentary Requirements Procedures Deadlines Related Revenue Issuances Codal Reference Frequently Asked Questionsshawn7800No ratings yet

- GTCPhase4 - Terms N ConditionDocument28 pagesGTCPhase4 - Terms N ConditionMitraNo ratings yet

- Guidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsDocument1 pageGuidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsAlyssa Hallasgo-Lopez AtabeloNo ratings yet

- Agree-Property Rate 2019 Final DraftDocument12 pagesAgree-Property Rate 2019 Final DraftKwasi AdarkwaNo ratings yet

- Punjab Excise and Property Tax LawDocument4 pagesPunjab Excise and Property Tax LawNishat AhmedNo ratings yet

- January 14, 2011: DescriptionDocument11 pagesJanuary 14, 2011: DescriptionRosselle GuevarraNo ratings yet

- RMC No 1-2018Document3 pagesRMC No 1-2018Larry Tobias Jr.No ratings yet

- Tax Agents and PractitionersDocument5 pagesTax Agents and PractitionerskawaiimiracleNo ratings yet

- Wealth Tax Wealth Tax ReturnDocument4 pagesWealth Tax Wealth Tax ReturnB GANAPATHYNo ratings yet

- RR 3-02Document6 pagesRR 3-02matinikkiNo ratings yet

- Taxpayers Bill of RightsDocument7 pagesTaxpayers Bill of RightsbubblingbrookNo ratings yet

- Estate Tax: BIR Form 1801Document13 pagesEstate Tax: BIR Form 1801Renalyn GardeNo ratings yet

- VAT Procedure in MaharashtraDocument14 pagesVAT Procedure in MaharashtraDeva DrillTechNo ratings yet

- Settlement CommissionDocument13 pagesSettlement CommissionParvathi Devi VaranasiNo ratings yet

- PenaltiesDocument2 pagesPenaltiesfatmaaleahNo ratings yet

- Estate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andDocument4 pagesEstate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andRey PerosaNo ratings yet

- 2000 June 2006 (Back)Document1 page2000 June 2006 (Back)Rica Santos-vallesteroNo ratings yet

- RMC 39-2013Document2 pagesRMC 39-2013Kram Ynothna BulahanNo ratings yet

- 0605 (July 1999)Document1 page0605 (July 1999)Yulo Vincent Bucayu PanuncioNo ratings yet

- Maize GuidelinesDocument3 pagesMaize GuidelinesSANGBIT ROYNo ratings yet

- Bacore 3 Course Packet 2Document15 pagesBacore 3 Course Packet 2Jenifer Borja BacayoNo ratings yet

- Taxation: 4. Other Percentage TaxDocument6 pagesTaxation: 4. Other Percentage TaxMarkuNo ratings yet

- Abci V Cir DigestDocument9 pagesAbci V Cir DigestSheilaNo ratings yet

- BIR Form 0614-EVAP Payment Form Guidelines and Instructions: Who Shall Use This FormDocument1 pageBIR Form 0614-EVAP Payment Form Guidelines and Instructions: Who Shall Use This FormMhel GollenaNo ratings yet

- Rmo 1982Document343 pagesRmo 1982Mary graceNo ratings yet

- BIR Form No. 2551M Percentage Tax Return Guidelines and InstructionsDocument2 pagesBIR Form No. 2551M Percentage Tax Return Guidelines and InstructionsseanjharodNo ratings yet

- Module VIDocument13 pagesModule VIRenz Joshua Quizon MunozNo ratings yet

- Who Are Not Required To File Income Tax ReturnsDocument2 pagesWho Are Not Required To File Income Tax ReturnsCarolina VillenaNo ratings yet

- Payments For Specified Energy Property in Lieu of Tax Credits Under The American Recovery and Reinvestment Act of 2009Document20 pagesPayments For Specified Energy Property in Lieu of Tax Credits Under The American Recovery and Reinvestment Act of 2009Terrence Murray100% (2)

- Checklist Housing LoanDocument2 pagesChecklist Housing LoanDevendra ChavhanNo ratings yet

- Unit IVDocument19 pagesUnit IVsatyabratadas688No ratings yet

- BIR Form 1701QDocument2 pagesBIR Form 1701QfileksNo ratings yet

- Individuals: Income Tax DescriptionDocument17 pagesIndividuals: Income Tax DescriptionMichael Olmedo NeneNo ratings yet

- Item No. 1 - Taxable Period: 1. Purely Compensation Income Earner BIR Annual Income Tax Return (ITR) Form No. 1700Document48 pagesItem No. 1 - Taxable Period: 1. Purely Compensation Income Earner BIR Annual Income Tax Return (ITR) Form No. 1700Miguel CasimNo ratings yet

- Sei - ItrDocument36 pagesSei - ItrMiguel CasimNo ratings yet

- Part C 1 - CIR Vs Avon Products ManufacturingDocument4 pagesPart C 1 - CIR Vs Avon Products ManufacturingCyruz TuppalNo ratings yet

- Part C 1 - CIR Vs Avon Products ManufacturingDocument4 pagesPart C 1 - CIR Vs Avon Products ManufacturingCyruz Tuppal75% (4)

- Executor Estate TaxDocument1 pageExecutor Estate TaxJessirie VillanuevaNo ratings yet

- RR 2-98 (As Amended)Document74 pagesRR 2-98 (As Amended)Mariano RentomesNo ratings yet

- Income Tax Description: IndividualsDocument13 pagesIncome Tax Description: IndividualsJAYAR MENDZNo ratings yet

- Income TaxDocument15 pagesIncome TaxJessNo ratings yet

- Digest RR 12-2018Document5 pagesDigest RR 12-2018Jesi CarlosNo ratings yet

- 7.d Citibank NA vs. CA (G.R. No. 107434 October 10, 1997) - H DigestDocument2 pages7.d Citibank NA vs. CA (G.R. No. 107434 October 10, 1997) - H DigestHarleneNo ratings yet

- Income TaxDocument14 pagesIncome TaxArielle CabritoNo ratings yet

- NBFA Application Form InstructionsDocument3 pagesNBFA Application Form InstructionsArvind GangwarNo ratings yet

- Assessment ReturnDocument10 pagesAssessment ReturnTriila manillaNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Covid 19 Pandemic and Abnormal Stock Returns of Listed Companies in VietnamDocument19 pagesCovid 19 Pandemic and Abnormal Stock Returns of Listed Companies in VietnamDaphne CasanovaNo ratings yet

- Final Year Report of BBS 4th YearDocument49 pagesFinal Year Report of BBS 4th Yearnepalfinance987No ratings yet

- Maint RateDocument3 pagesMaint RateMuani HmarNo ratings yet

- Amount in Words Is Rupees Eleven Thousand Six OnlyDocument1 pageAmount in Words Is Rupees Eleven Thousand Six OnlyGunaganti MaheshNo ratings yet

- Topic: Privatisation and Regulation: 211.business, Government and SocietyDocument10 pagesTopic: Privatisation and Regulation: 211.business, Government and SocietyManisha YadavNo ratings yet

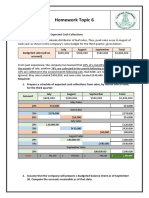

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- GMF 2019 2038 Airbus Commercial Aircraft Book PDFDocument86 pagesGMF 2019 2038 Airbus Commercial Aircraft Book PDFjuan manuel100% (1)

- M and S Responsible Cotton Sourcing PolicyDocument5 pagesM and S Responsible Cotton Sourcing PolicyvictoriawildmanNo ratings yet

- Karina Dan Setiadi, 2020Document13 pagesKarina Dan Setiadi, 2020Iwan SetiadiNo ratings yet

- Mary Kay Cosmetics FinalDocument17 pagesMary Kay Cosmetics FinalChetan SaxenaNo ratings yet

- Thai Restaurant Cash FlowDocument33 pagesThai Restaurant Cash FlowElizabethNo ratings yet

- EF3333 - Financial Systems, Markets and InstrumentsDocument13 pagesEF3333 - Financial Systems, Markets and InstrumentsLi Man KitNo ratings yet

- May June Austrian 2023 0Document40 pagesMay June Austrian 2023 0Elena HernadezNo ratings yet

- QuestionsDocument5 pagesQuestionsneelam khanNo ratings yet

- Total IncomeDocument7 pagesTotal IncomeVaishali SharmaNo ratings yet

- MDRRMC Resolution Canaman Revised - 11 02 22Document5 pagesMDRRMC Resolution Canaman Revised - 11 02 22Mara Kenia BarcelonNo ratings yet

- Does A One Size Fits All Minimum Wage Cause Financial Stress For Small Businesses?Document3 pagesDoes A One Size Fits All Minimum Wage Cause Financial Stress For Small Businesses?Cato InstituteNo ratings yet

- Item 11 - Imperfect CompetitionDocument42 pagesItem 11 - Imperfect CompetitionTiviyaNo ratings yet

- Agreement Termination NoticeDocument1 pageAgreement Termination NoticeBadri PrasadNo ratings yet

- 533 - Lucky Brimblecombe Fitzpatrick Referrals Invoice 1-88682Document1 page533 - Lucky Brimblecombe Fitzpatrick Referrals Invoice 1-88682himanshu kNo ratings yet

- Module 5 - Foreign Direct InvestmentDocument9 pagesModule 5 - Foreign Direct InvestmentMarjon DimafilisNo ratings yet

- Managerial Accounting: Assignment: 02Document5 pagesManagerial Accounting: Assignment: 02Asma HatamNo ratings yet

- 12 Political Science - Globalisation - NotesDocument5 pages12 Political Science - Globalisation - NotesNishi MishraNo ratings yet

- Annuity DueDocument27 pagesAnnuity Duebayu fajarNo ratings yet

- The United Arab Republic An Assessment of Its FailureDocument19 pagesThe United Arab Republic An Assessment of Its FailureDeepak KumarNo ratings yet

- Mobile Crane Lifting PermitDocument2 pagesMobile Crane Lifting PermitMusadiq HussainNo ratings yet

- Uganda FrameworkDocument375 pagesUganda FrameworkFree UgandaNo ratings yet

- Hazel Henderson Creating Alternative FuturesDocument203 pagesHazel Henderson Creating Alternative FuturesShawn SpannNo ratings yet

- Session 1 & 2 - Introduction To Operations ManagementDocument38 pagesSession 1 & 2 - Introduction To Operations ManagementArka BandyopadhyayNo ratings yet