You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

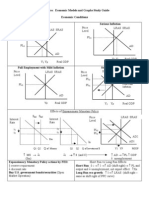

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Aramis: User Manual - SoftwareDocument129 pagesAramis: User Manual - Softwareotipicni6969No ratings yet

- The Importance of Quantitative Research Across FieldsDocument2 pagesThe Importance of Quantitative Research Across FieldsWilson100% (2)

- Textbook of Interventional Cardiology 8Th Edition Eric J Topol Full ChapterDocument67 pagesTextbook of Interventional Cardiology 8Th Edition Eric J Topol Full Chapterora.bowman920100% (9)

- Kinematics 2D (Projectile Motion) - NEET Previous Year Question With Complete SolutionDocument4 pagesKinematics 2D (Projectile Motion) - NEET Previous Year Question With Complete SolutionrevathyNo ratings yet

- Eng Sca 0001 RedDocument64 pagesEng Sca 0001 RedAndrea GibsonNo ratings yet

- QMS Assignment 1Document3 pagesQMS Assignment 1John Michael PadillaNo ratings yet

- Atsap Briefing SheetDocument1 pageAtsap Briefing Sheetapi-20616942No ratings yet

- MARUTI Vision and MissionDocument10 pagesMARUTI Vision and MissionAarif Raheem Rather80% (5)

- Weibull DistributionDocument5 pagesWeibull Distributionknight1410No ratings yet

- Project Review and Administrative AspectsDocument22 pagesProject Review and Administrative Aspectsamit861595% (19)

- 2016 Challenger CAT 01.pdfDocument81 pages2016 Challenger CAT 01.pdfAditya SuruNo ratings yet

- Python Lab Manual - III BCA (1 To 10)Document23 pagesPython Lab Manual - III BCA (1 To 10)sp2392546No ratings yet

- Follow Instructions Safely Take Careful Measurements.: Investigating Force, Mass and AccelerationDocument14 pagesFollow Instructions Safely Take Careful Measurements.: Investigating Force, Mass and AccelerationSamuel KalemboNo ratings yet

- Proview Datasheet - SM MDVR 401 4G - INDDocument2 pagesProview Datasheet - SM MDVR 401 4G - INDSlamat AgungNo ratings yet

- Bilal ThesisDocument63 pagesBilal ThesisKashif Ur RehmanNo ratings yet

- Ee3101 Lab Report ExpDocument16 pagesEe3101 Lab Report ExpyucesNo ratings yet

- Cafeteria and Management ReviewerDocument16 pagesCafeteria and Management ReviewerGhibi TrinidadNo ratings yet

- 9702 PHYSICS: MARK SCHEME For The May/June 2012 Question Paper For The Guidance of TeachersDocument7 pages9702 PHYSICS: MARK SCHEME For The May/June 2012 Question Paper For The Guidance of TeachersxiaokiaNo ratings yet

- Service Manual: Model: SR500ADocument24 pagesService Manual: Model: SR500ASari Barak VE YehudaNo ratings yet

- Economics II Assignment 1: Chapter 15 Measuring GDPDocument9 pagesEconomics II Assignment 1: Chapter 15 Measuring GDP許雅婷No ratings yet

- Mar 2019 SGVDocument24 pagesMar 2019 SGVBien Bowie A. CortezNo ratings yet

- Review - An Invitation To Cognitive Science Methods, Models, and Conceptual IssuesDocument2 pagesReview - An Invitation To Cognitive Science Methods, Models, and Conceptual IssuesTaisei ChujoNo ratings yet

- 1015Document11 pages1015Crystal Audrey Malinda NelsonNo ratings yet

- Strategic Action Fields of Digital TransformationDocument21 pagesStrategic Action Fields of Digital TransformationHeldi SahputraNo ratings yet

- Long Slot Array For Wireless Power Transmission: Mauro Ettorre, Waleed A. Alomar, Anthony GrbicDocument2 pagesLong Slot Array For Wireless Power Transmission: Mauro Ettorre, Waleed A. Alomar, Anthony GrbichosseinNo ratings yet

- Tarjetas Electronicas ServoDocument2 pagesTarjetas Electronicas ServoChris HANo ratings yet

- Office of The Additional Director General of Police (T&Ap) Cum Chairman S.L.P.R.B. Assam, Ulubari, Guwahati - 7Document16 pagesOffice of The Additional Director General of Police (T&Ap) Cum Chairman S.L.P.R.B. Assam, Ulubari, Guwahati - 7Jayanta Kumar NathNo ratings yet

- 7 MODULE 7 Nervous SystemDocument29 pages7 MODULE 7 Nervous SystemCHARIEMAE CA�AZARESNo ratings yet

- APC2100 Device Number Key V2.0Document1 pageAPC2100 Device Number Key V2.0mmbb89No ratings yet