You might also like

- USA V Guinto (Case Digest)Document2 pagesUSA V Guinto (Case Digest)haruhime08100% (8)

- Teacher Payout Document-1st Sept PDFDocument7 pagesTeacher Payout Document-1st Sept PDFJayantNo ratings yet

- Blue Moon Esignature Services Document Id: 378689181Document88 pagesBlue Moon Esignature Services Document Id: 378689181Faheem Mahmood ButtNo ratings yet

- Complete Guide About Auditor Appointment PDFDocument6 pagesComplete Guide About Auditor Appointment PDFshreya charmiNo ratings yet

- Company Law AssignmentDocument9 pagesCompany Law Assignmentrohanjaiswal290301No ratings yet

- Auditing Unit - 5 by Anitha RDocument16 pagesAuditing Unit - 5 by Anitha RAnitha RNo ratings yet

- Chapter 10Document48 pagesChapter 10garimamittalNo ratings yet

- Appointment and Position of Auditors: Corporate Law-IiDocument12 pagesAppointment and Position of Auditors: Corporate Law-Iivinay sharmaNo ratings yet

- Auditors' Independence and AccountabilityDocument29 pagesAuditors' Independence and Accountabilitysana khanNo ratings yet

- A 6.4 Audit Unit 4Document11 pagesA 6.4 Audit Unit 4Gaurav MahajanNo ratings yet

- CL Kaush PrintDocument9 pagesCL Kaush PrintWork 2018No ratings yet

- Auditing & Indirect Tax ProjectDocument10 pagesAuditing & Indirect Tax ProjectAnkush KhyoriaNo ratings yet

- Company Law - 46 and 49Document12 pagesCompany Law - 46 and 49sourav0% (1)

- Auditor Under Company LawDocument13 pagesAuditor Under Company Lawruchika jha100% (1)

- C10 Audit Question BankDocument39 pagesC10 Audit Question BankVINUS DHANKHARNo ratings yet

- Key Answer Test 2Document6 pagesKey Answer Test 2Vaishnavi SNo ratings yet

- Co. Act - 2013: Secretarial AuditDocument5 pagesCo. Act - 2013: Secretarial AuditofficemvaNo ratings yet

- F4 Chapter19Document31 pagesF4 Chapter19Husnain SattiNo ratings yet

- Auditor-Role, Duties, QualificationsDocument98 pagesAuditor-Role, Duties, Qualificationsmuch ntgNo ratings yet

- 6 - Audit of Limited CompaniesDocument16 pages6 - Audit of Limited CompaniesBhagaban DasNo ratings yet

- Audit Assignment 3Document12 pagesAudit Assignment 3Anam FatimaNo ratings yet

- What Is An Auditor?: Key TakeawaysDocument9 pagesWhat Is An Auditor?: Key TakeawaysMohit RanaNo ratings yet

- @ProCA - Inter Company Audit Correct & IncorrectDocument10 pages@ProCA - Inter Company Audit Correct & IncorrectSonu SharmaNo ratings yet

- Unit - 2 Study Material ACGDocument18 pagesUnit - 2 Study Material ACGAbhijeet UpadhyayNo ratings yet

- Auditor Company Law Assignment - ALOK COMPANY IIDocument9 pagesAuditor Company Law Assignment - ALOK COMPANY IIAditya SinhaNo ratings yet

- Auditors Appointment, Role and Removal Under The Companies ActDocument11 pagesAuditors Appointment, Role and Removal Under The Companies ActManoj SJNo ratings yet

- Chapter 10 Audit and Auditors Lyst8195Document21 pagesChapter 10 Audit and Auditors Lyst8195Rambo HereNo ratings yet

- Appointment of Auditor: Group MembersDocument14 pagesAppointment of Auditor: Group Memberszahid_497No ratings yet

- Unit 5 - Audit - CGDocument57 pagesUnit 5 - Audit - CGRalfNo ratings yet

- Auditors PPT FinalDocument31 pagesAuditors PPT FinalSri V N Prakash Sharma, Asst. Professor, Management & Commerce, SSSIHLNo ratings yet

- Nov 2018 Auditing SGDocument15 pagesNov 2018 Auditing SGNaruto UzumakiNo ratings yet

- Companies Act 2013Document4 pagesCompanies Act 2013Y TEJASWININo ratings yet

- WWW - Edutap.co - In: Chapter X of Companies Act - Audit and Auditors Sections 140 To 142Document11 pagesWWW - Edutap.co - In: Chapter X of Companies Act - Audit and Auditors Sections 140 To 142Suvojit DeshiNo ratings yet

- External Audit (Group B)Document12 pagesExternal Audit (Group B)PRABAL ROYNo ratings yet

- Company Law: Accounts and AuditDocument18 pagesCompany Law: Accounts and AuditPratima SrivastavaNo ratings yet

- Now Let's Talk About, Who Is Eligible To Conduct Secretarial Audit in India?Document3 pagesNow Let's Talk About, Who Is Eligible To Conduct Secretarial Audit in India?Paras MittalNo ratings yet

- SEBI Grade A 2020 Companies Act Chapter XDocument8 pagesSEBI Grade A 2020 Companies Act Chapter Xnit07No ratings yet

- Company LawDocument11 pagesCompany LawRohan DuaNo ratings yet

- Company Audit MaterialDocument22 pagesCompany Audit Materialbipin papnoi100% (2)

- Appointment of AuditorDocument16 pagesAppointment of Auditorshahnawaz243No ratings yet

- Clause 49 Listing AgreementDocument10 pagesClause 49 Listing AgreementAarti MaanNo ratings yet

- Discuss The Qualifications and Disqualifications of Auditor of The CompanyDocument9 pagesDiscuss The Qualifications and Disqualifications of Auditor of The CompanyDebabrata DasNo ratings yet

- Who Is An Auditor?Document15 pagesWho Is An Auditor?Aman ChauhanNo ratings yet

- 8 Company Auditor: JectivesDocument6 pages8 Company Auditor: JectivesRishabh GuptaNo ratings yet

- The Project Report On The Topic: University Institute of Legal Studies Panjab University, ChandigarhDocument10 pagesThe Project Report On The Topic: University Institute of Legal Studies Panjab University, ChandigarhÅPEX々 N33JÜNo ratings yet

- Audit Part 2 29Document5 pagesAudit Part 2 29Anshul RathiNo ratings yet

- Comapny QuestionsDocument36 pagesComapny QuestionsvinodNo ratings yet

- Pervezvikiyo - 3498 - 17836 - 2 - Intro To Assurance & Legal (Oct 11, 2020)Document9 pagesPervezvikiyo - 3498 - 17836 - 2 - Intro To Assurance & Legal (Oct 11, 2020)Sadia AbidNo ratings yet

- Unit 3Document6 pagesUnit 3Saniya HashmiNo ratings yet

- Auditing Unit-3Document11 pagesAuditing Unit-3swethaswetty06No ratings yet

- Statutory AuditDocument20 pagesStatutory Auditkalpesh mhatreNo ratings yet

- Auditors PPT FinalDocument31 pagesAuditors PPT Finaldewashish mahatha100% (1)

- Auditors Qualification 2.1Document39 pagesAuditors Qualification 2.1Sayraj Siddiki AnikNo ratings yet

- AuditorsDocument14 pagesAuditorsjaoceelectricalNo ratings yet

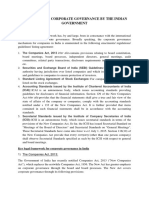

- Initiatives On Corporate Governance by The Indian GovernmentDocument2 pagesInitiatives On Corporate Governance by The Indian GovernmentRamesh BaglaNo ratings yet

- The Institute of Chartered Accountants of Bangladesh Professional Stage: Knowledge Level Additional Sheet - Concept of and Need For AssuranceDocument4 pagesThe Institute of Chartered Accountants of Bangladesh Professional Stage: Knowledge Level Additional Sheet - Concept of and Need For AssuranceShahid MahmudNo ratings yet

- Chapter - 4 (Short Notes)Document5 pagesChapter - 4 (Short Notes)Aakansha SinghNo ratings yet

- Company AuditorDocument13 pagesCompany AuditorjaoceelectricalNo ratings yet

- KC Audit CommitteeDocument3 pagesKC Audit CommitteeBijoyBhawanNo ratings yet

- Module 1: Company Auditor: SynopsisDocument18 pagesModule 1: Company Auditor: SynopsisRuthvik RevanthNo ratings yet

- MR Ial-2018Document20 pagesMR Ial-2018sajedulNo ratings yet

- Syllabus LLB LLM PHD PDFDocument2 pagesSyllabus LLB LLM PHD PDFIshaan JainNo ratings yet

- B.A.LL.B. V Sem.2015-16Document7 pagesB.A.LL.B. V Sem.2015-16Shubham RawatNo ratings yet

- Zara Terms and Conditions en - IN 20190115 PDFDocument12 pagesZara Terms and Conditions en - IN 20190115 PDFNancygirdherNo ratings yet

- Indian Law Institute Journal of The Indian Law InstituteDocument19 pagesIndian Law Institute Journal of The Indian Law InstituteJayantNo ratings yet

- 5 Semester Ballb PDFDocument11 pages5 Semester Ballb PDFThakur Digvijay SinghNo ratings yet

- NOTICE AdmissionLLB V3 PDFDocument2 pagesNOTICE AdmissionLLB V3 PDFJayantNo ratings yet

- MAMScEntranceSyllabus 2019Document2 pagesMAMScEntranceSyllabus 2019mohit chauhanNo ratings yet

- NH7304216332726 E-Voucher PDFDocument2 pagesNH7304216332726 E-Voucher PDFJayantNo ratings yet

- Circumstantial EvidenceDocument8 pagesCircumstantial EvidenceMahendra SinghNo ratings yet

- Circumstantial EvidenceDocument8 pagesCircumstantial EvidenceMahendra SinghNo ratings yet

- Project Profile Doctrine of Feeding TheDocument21 pagesProject Profile Doctrine of Feeding Themonali raiNo ratings yet

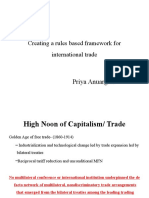

- Creating A Rules Based Framework For International Trade: Priya AnuarginiDocument14 pagesCreating A Rules Based Framework For International Trade: Priya AnuarginiJayantNo ratings yet

- Legal Theory Skepticism and Philosophical Skepticism: Comparison, Contrast, and AssessmentDocument2 pagesLegal Theory Skepticism and Philosophical Skepticism: Comparison, Contrast, and AssessmentJayantNo ratings yet

- Zara Terms and Conditions en - IN 20190115 PDFDocument12 pagesZara Terms and Conditions en - IN 20190115 PDFNancygirdherNo ratings yet

- Title: Principles of Natural Justice: in The Light of Administrative LAWDocument15 pagesTitle: Principles of Natural Justice: in The Light of Administrative LAWJayantNo ratings yet

- 2017 Paper PDFDocument8 pages2017 Paper PDFNitin GuptaNo ratings yet

- Rights and Liabilities of Mortgagor: Nikhil SolankiDocument8 pagesRights and Liabilities of Mortgagor: Nikhil SolankiJayantNo ratings yet

- Judicial Activism and EnvironmentDocument20 pagesJudicial Activism and EnvironmentGaurav PandeyNo ratings yet

- EL Material Part IIDocument76 pagesEL Material Part IIJayantNo ratings yet

- India and Anti Dumping Under The WTO: K. Narayanan and Lalithambal NatarajanDocument26 pagesIndia and Anti Dumping Under The WTO: K. Narayanan and Lalithambal NatarajanparmeshwarNo ratings yet

- Judicial Process and Human Rights in IndiaDocument19 pagesJudicial Process and Human Rights in IndiaMamatha RangaswamyNo ratings yet

- PDFDocument13 pagesPDFJayantNo ratings yet

- 201902061549471886U.P.JUDICIAL - SERVICES - (CIVIL JUDGE) - (Jr. - Div.) - (P) - EXAM - 2018 (GK) - (Exam - Held - On - 16 - Dec - 2018) PDFDocument29 pages201902061549471886U.P.JUDICIAL - SERVICES - (CIVIL JUDGE) - (Jr. - Div.) - (P) - EXAM - 2018 (GK) - (Exam - Held - On - 16 - Dec - 2018) PDFJayantNo ratings yet

- EL Material Part IDocument10 pagesEL Material Part IJayantNo ratings yet

- Judicial Activism and EnvironmentDocument20 pagesJudicial Activism and EnvironmentGaurav PandeyNo ratings yet

- Climate2030 IndiaDocument54 pagesClimate2030 IndiaPawan NabiyalNo ratings yet

- E-Waste Management in India: Current Practices and ChallengesDocument14 pagesE-Waste Management in India: Current Practices and ChallengesJayantNo ratings yet

- Audit Assignment NewDocument20 pagesAudit Assignment NewJayantNo ratings yet

- Petitioner Respondent: Second DivisionDocument5 pagesPetitioner Respondent: Second DivisionSeok Gyeong KangNo ratings yet

- Wyoming (2027-2029) - Amended (00396220xC146B)Document5 pagesWyoming (2027-2029) - Amended (00396220xC146B)Matt BrownNo ratings yet

- Compliance To Restrictions To Doing Business or Operating Business in The PhilippinesDocument11 pagesCompliance To Restrictions To Doing Business or Operating Business in The PhilippinesmgeeNo ratings yet

- Identifying Conflicts of Interest Coi RicsDocument2 pagesIdentifying Conflicts of Interest Coi Ricssafiya alaminNo ratings yet

- Vocabulary For English: Term Difinition Translati OnDocument7 pagesVocabulary For English: Term Difinition Translati OnBuzdugan NicoletaNo ratings yet

- Satar Kata Sutra 2Document2 pagesSatar Kata Sutra 2Yogesh MehtaNo ratings yet

- Dupont Artistri Product Offering: Textile Inks and AuxiliariesDocument2 pagesDupont Artistri Product Offering: Textile Inks and AuxiliariesAymen HajjiNo ratings yet

- Women DirectorDocument6 pagesWomen DirectorMayank Sen100% (1)

- Policing, Custodial Torture and Human Rights: Designing A Policy Framework For PakistanDocument124 pagesPolicing, Custodial Torture and Human Rights: Designing A Policy Framework For PakistanWasimNo ratings yet

- PT Indofood CBP Sukses Makmur TBK Silvia Ayuni (1961117) Ks1aDocument7 pagesPT Indofood CBP Sukses Makmur TBK Silvia Ayuni (1961117) Ks1aSilvia AyuniNo ratings yet

- Lakeview Gold and Country Club v. NayonDocument6 pagesLakeview Gold and Country Club v. NayonKristienne Carol PuruggananNo ratings yet

- DS11 CompleteDocument6 pagesDS11 CompletesarahNo ratings yet

- Lawyers: Is Money"Document19 pagesLawyers: Is Money"Emane EbubeNo ratings yet

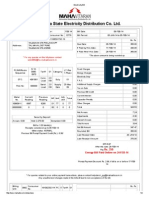

- Electricity BillDocument2 pagesElectricity Billrahuldbajaj2011No ratings yet

- Dadizon V CA - Sy-Santos, Kyra S.Document1 pageDadizon V CA - Sy-Santos, Kyra S.KyraNo ratings yet

- Equity and Law PPT 2 2020726132360Document7 pagesEquity and Law PPT 2 2020726132360UMANG COMPUTERSNo ratings yet

- Debulgado v. CSCDocument20 pagesDebulgado v. CSCJune DoriftoNo ratings yet

- Co Kim Cham vs. Tan Keh and DizonDocument2 pagesCo Kim Cham vs. Tan Keh and DizonMARIANNE DILANGALENNo ratings yet

- Remedial Law Bar 2018 With Suggested Answers 1Document107 pagesRemedial Law Bar 2018 With Suggested Answers 1Malvin Aragon BalletaNo ratings yet

- Real Estate Mortgage AgreementDocument3 pagesReal Estate Mortgage AgreementKen BaxNo ratings yet

- Iso 02380-2-2004Document10 pagesIso 02380-2-2004rtsultanNo ratings yet

- Trump v. Cohen - Plaintiff's ComplaintDocument32 pagesTrump v. Cohen - Plaintiff's ComplaintDaily Caller News FoundationNo ratings yet

- Abyip 2021 Ibuan Final 2023Document1 pageAbyip 2021 Ibuan Final 2023Dexter OndaNo ratings yet

- Substantive Due Process of LawDocument66 pagesSubstantive Due Process of LawJeff WinchesterNo ratings yet

- ASTM D610 - Standard Practice For Evaluating Degree of Rusting On Painted Steel SurfacesDocument6 pagesASTM D610 - Standard Practice For Evaluating Degree of Rusting On Painted Steel SurfacesRoger SchvepperNo ratings yet

- Makati Sports v. ChengDocument7 pagesMakati Sports v. ChengZazaNo ratings yet

- Sahara India Scam PDFDocument15 pagesSahara India Scam PDFShehnila AtharNo ratings yet