You might also like

- 9.refund VoucherDocument18 pages9.refund VoucherSamrat ManchekarNo ratings yet

- Fiscal PolicyDocument24 pagesFiscal Policyરહીમ હુદ્દાNo ratings yet

- EconomicsDocument32 pagesEconomicsSahil BansalNo ratings yet

- Jaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Document4 pagesJaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Saurabh SinghNo ratings yet

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018From EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No ratings yet

- Resident Status For IndividualDocument24 pagesResident Status For IndividualMalabaris Malaya Umar SiddiqNo ratings yet

- Self Employment Guidance - Form 1040 Schedule C IndividualsDocument2 pagesSelf Employment Guidance - Form 1040 Schedule C IndividualsGlenda100% (1)

- INFOLINK COLLEGE (Public Finance)Document138 pagesINFOLINK COLLEGE (Public Finance)arsen lupin100% (1)

- Roger Weliner v. CirDocument1 pageRoger Weliner v. CirChiiNo ratings yet

- Quasar Telecom Consultants Pvt. LTD.: #1, Old Veterinary Hospital Road, Basavanagudi, Bangalore - 560 004Document1 pageQuasar Telecom Consultants Pvt. LTD.: #1, Old Veterinary Hospital Road, Basavanagudi, Bangalore - 560 004Hari KumarNo ratings yet

- Fiscal PolicyDocument6 pagesFiscal Policynarayan100% (2)

- VK TradersDocument16 pagesVK TradersMOHAN ChandNo ratings yet

- Fiscal PolicyDocument29 pagesFiscal Policyjay100% (1)

- Fiscal PolicyDocument5 pagesFiscal PolicyAmnaAnwar100% (1)

- 7F Arthaland Century Pacific Tower, 5 Avenue Corner 30 ST., Bonifacio Global City, Taguig City 1634 T (632) 4036910 F (632) 4036908Document2 pages7F Arthaland Century Pacific Tower, 5 Avenue Corner 30 ST., Bonifacio Global City, Taguig City 1634 T (632) 4036910 F (632) 4036908anna sheillaNo ratings yet

- US Citizens Cannot Deduct Foreign Taxes from Philippine IncomeDocument2 pagesUS Citizens Cannot Deduct Foreign Taxes from Philippine IncomeShariqah Hanimai Indol Macumbal-YusophNo ratings yet

- Project Report: Name and Address:-Of The ApplicantDocument10 pagesProject Report: Name and Address:-Of The Applicantakki_6551No ratings yet

- Fiscal and Monetary Policy OverviewDocument13 pagesFiscal and Monetary Policy OverviewThouseef AhmedNo ratings yet

- CHAPTER I - Introduction-to-Public-FinanceDocument12 pagesCHAPTER I - Introduction-to-Public-FinanceMaricel GoNo ratings yet

- Managerial Economics Unit VDocument14 pagesManagerial Economics Unit VTanmay JainNo ratings yet

- Topic 8 Fiscal Policy, The Deficit, and Debt - JBNDocument24 pagesTopic 8 Fiscal Policy, The Deficit, and Debt - JBNleimarNo ratings yet

- Fiscal Policy Instruments and Objectives in 40 CharactersDocument4 pagesFiscal Policy Instruments and Objectives in 40 CharactersRABINDRA KHATIWADANo ratings yet

- Fiscal Policy of PakistanDocument15 pagesFiscal Policy of PakistanAXAD BhattiNo ratings yet

- Some Important TopicsDocument5 pagesSome Important TopicsStuti DeopaNo ratings yet

- FInal Eco Project For SubmissionDocument45 pagesFInal Eco Project For SubmissionAakankshaNo ratings yet

- Budget PolicyDocument9 pagesBudget PolicyahmedknightNo ratings yet

- Fiscal Policy MacroDocument15 pagesFiscal Policy MacroHassan FarooqNo ratings yet

- Module 6 - Lect 2 - Fiscal PolicyDocument19 pagesModule 6 - Lect 2 - Fiscal PolicyBHAVYA GOPAL 18103096No ratings yet

- Fiscal PolicyDocument13 pagesFiscal PolicyAakash SaxenaNo ratings yet

- Fiscal Policy ExplainedDocument10 pagesFiscal Policy ExplainedSamad Raza KhanNo ratings yet

- XII - ECONOMICS - UNIT Government Budget and The Economy - NotesDocument7 pagesXII - ECONOMICS - UNIT Government Budget and The Economy - NotesJanvi AhluwaliaNo ratings yet

- Fiscal PolicyDocument25 pagesFiscal PolicyJivanjot SinghNo ratings yet

- Macroeconomics - Fiscal PolicyDocument29 pagesMacroeconomics - Fiscal PolicydahliagingerNo ratings yet

- Fiscal PolicyDocument19 pagesFiscal PolicyShreya SharmaNo ratings yet

- Fiscal PolicyDocument11 pagesFiscal PolicyVenkata RamanaNo ratings yet

- Government BudgetDocument8 pagesGovernment Budgettrishandas180No ratings yet

- Teja Economics ProjectDocument43 pagesTeja Economics ProjectSuseendar RaviNo ratings yet

- PFT HandOutDocument14 pagesPFT HandOutyechale tafereNo ratings yet

- Fiscal Policy MeaningDocument27 pagesFiscal Policy MeaningVikash SinghNo ratings yet

- Class XII Government Budget NotesDocument8 pagesClass XII Government Budget NotesHarshit AgarwalNo ratings yet

- How fiscal policy impacts economiesDocument13 pagesHow fiscal policy impacts economiesAnuradha SharmaNo ratings yet

- Government Budget - A Financial StatementDocument15 pagesGovernment Budget - A Financial StatementJsmBhanotNo ratings yet

- Budget DeficitDocument6 pagesBudget Deficityamikanimapwetechere23No ratings yet

- Fiscal Policy Business EnvironmentDocument37 pagesFiscal Policy Business EnvironmentvikashkalpNo ratings yet

- Fiscal Policy in 40 CharactersDocument5 pagesFiscal Policy in 40 CharactersZubair NajarNo ratings yet

- Unit 4-Fiscal PolicyDocument55 pagesUnit 4-Fiscal Policyironman73500No ratings yet

- Fiscal Policy: Why It MattersDocument8 pagesFiscal Policy: Why It MatterspriyaNo ratings yet

- Fiscal and Monetary Policy: What Is Fiscal Policy?Document7 pagesFiscal and Monetary Policy: What Is Fiscal Policy?sana shahidNo ratings yet

- Fiscal policy explainedDocument4 pagesFiscal policy explainedPrashant SinghNo ratings yet

- Fiscal Policy and Public Debt - RevisedDocument70 pagesFiscal Policy and Public Debt - Revisedtxn5j29mmqNo ratings yet

- Government Budget Notes (CBSE) PDFDocument10 pagesGovernment Budget Notes (CBSE) PDFHarshit AgarwalNo ratings yet

- Government Budget IndiaDocument7 pagesGovernment Budget IndiaNikhil Goel100% (1)

- Fiscal PolicyDocument6 pagesFiscal Policynoor fatimaNo ratings yet

- Fin - Elective 4 ActivitiesDocument2 pagesFin - Elective 4 Activitiesapplejane janeaNo ratings yet

- Public Finance-PARANADA, Diana, QUEJADO, Narcisa TAGLE, EugeneDocument54 pagesPublic Finance-PARANADA, Diana, QUEJADO, Narcisa TAGLE, EugeneJERRALYN ALVANo ratings yet

- Fiscal Policy MeaningDocument6 pagesFiscal Policy MeaningsurindersalhNo ratings yet

- Government of India Budget: Meaning, Elements, Objectives and TypesDocument7 pagesGovernment of India Budget: Meaning, Elements, Objectives and TypesBirendar JainNo ratings yet

- Government BudgetDocument9 pagesGovernment BudgetShawnNo ratings yet

- Fiscal Policy WrittenDocument4 pagesFiscal Policy WrittenKenneth Rae QuirimoNo ratings yet

- Ethiopian Public Finance Budgeting and Revenue StructureDocument16 pagesEthiopian Public Finance Budgeting and Revenue StructuremengistuNo ratings yet

- Publicfinance 171028062357Document77 pagesPublicfinance 171028062357Al MahmudNo ratings yet

- Macro Economic Policy InstrumentsDocument11 pagesMacro Economic Policy InstrumentsThankachan CJNo ratings yet

- Fiscal PolicyDocument20 pagesFiscal PolicyPranav VaidNo ratings yet

- Fiscal Policy (ECONOMICS)Document20 pagesFiscal Policy (ECONOMICS)Rajneesh DeshmukhNo ratings yet

- What Is Fiscal Policy and Its Role in Economic GrowthDocument4 pagesWhat Is Fiscal Policy and Its Role in Economic GrowthsmartysusNo ratings yet

- Chapter-One Overview of Public Finance & TaxationDocument211 pagesChapter-One Overview of Public Finance & Taxationarsen lupinNo ratings yet

- Fiscal Policy Assignment 2Document9 pagesFiscal Policy Assignment 2Shafique UR Rehman JuttNo ratings yet

- Business Economics: Business Strategy & Competitive AdvantageFrom EverandBusiness Economics: Business Strategy & Competitive AdvantageNo ratings yet

- Fundamentals of Business Economics Study Resource: CIMA Study ResourcesFrom EverandFundamentals of Business Economics Study Resource: CIMA Study ResourcesNo ratings yet

- Jaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Document7 pagesJaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Saurabh SinghNo ratings yet

- Imc Project Report On IkeaDocument10 pagesImc Project Report On IkeaSaurabh SinghNo ratings yet

- Jaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Document13 pagesJaipuria Institute of Management, Vineet Khand, Gomti Nagar Lucknow - 226 010Saurabh SinghNo ratings yet

- CB Individual Project1Document4 pagesCB Individual Project1Saurabh SinghNo ratings yet

- Ferns and Petals Pioneered Organized Flower Retailing in IndiaDocument6 pagesFerns and Petals Pioneered Organized Flower Retailing in IndiaSaurabh SinghNo ratings yet

- CB Individual ProjectDocument6 pagesCB Individual ProjectSaurabh SinghNo ratings yet

- SMBD ProjectDocument8 pagesSMBD ProjectSaurabh SinghNo ratings yet

- Amazon KindleDocument7 pagesAmazon KindleSaurabh SinghNo ratings yet

- SegmentationDocument2 pagesSegmentationSaurabh SinghNo ratings yet

- Hidesign Identity Positioning CaseDocument4 pagesHidesign Identity Positioning CaseSaurabh SinghNo ratings yet

- SegmentationDocument2 pagesSegmentationSaurabh SinghNo ratings yet

- Case 1 1. As Expressed For The Situation, The New York Times Decided To Convey TheirDocument2 pagesCase 1 1. As Expressed For The Situation, The New York Times Decided To Convey TheirSaurabh SinghNo ratings yet

- Jaipuria Institute of Management Individual Assignment Topic: Customer Management Practices at Top Retail Brands IKEA, Nordstrom, and NikeDocument4 pagesJaipuria Institute of Management Individual Assignment Topic: Customer Management Practices at Top Retail Brands IKEA, Nordstrom, and NikeSaurabh SinghNo ratings yet

- Major Brands in MarketDocument4 pagesMajor Brands in MarketSaurabh SinghNo ratings yet

- Case 1 1. As Expressed For The Situation, The New York Times Decided To Convey TheirDocument2 pagesCase 1 1. As Expressed For The Situation, The New York Times Decided To Convey TheirSaurabh SinghNo ratings yet

- Industry OverviewDocument7 pagesIndustry OverviewSaurabh SinghNo ratings yet

- SegmentationDocument2 pagesSegmentationSaurabh SinghNo ratings yet

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document7 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)Saurabh SinghNo ratings yet

- SegmentationDocument2 pagesSegmentationSaurabh SinghNo ratings yet

- Receipt - SIP REPORTDocument1 pageReceipt - SIP REPORTSaurabh SinghNo ratings yet

- Applicartion FormDocument1 pageApplicartion FormSaurabh SinghNo ratings yet

- PARLEDocument16 pagesPARLESaurabh SinghNo ratings yet

- MDocument5 pagesMsandeep kumarNo ratings yet

- SegmentationDocument2 pagesSegmentationSaurabh SinghNo ratings yet

- BEE (2019-20) Handout 03 Aggregate Expenditure Aggregate OutputDocument6 pagesBEE (2019-20) Handout 03 Aggregate Expenditure Aggregate OutputSaurabh SinghNo ratings yet

- Bajaj Allianz Two Wheeler Insurance SummaryDocument5 pagesBajaj Allianz Two Wheeler Insurance SummarySaurabh SinghNo ratings yet

- BEE (2019-20) Handout 01 (Economic Systems and Classification of Economies)Document3 pagesBEE (2019-20) Handout 01 (Economic Systems and Classification of Economies)sandeep kumarNo ratings yet

- BEE (2019-20) Handout 09 (Exchange Rate Determination)Document3 pagesBEE (2019-20) Handout 09 (Exchange Rate Determination)tyagi9334No ratings yet

- Estate Tax Exam Multiple Choice QuestionsDocument8 pagesEstate Tax Exam Multiple Choice Questionsrey mark hamacNo ratings yet

- Superannuation Withdrawal FormDocument5 pagesSuperannuation Withdrawal FormGaneshNo ratings yet

- The Indian Partnership Act 1932 Application For Registration of Firm by TheDocument2 pagesThe Indian Partnership Act 1932 Application For Registration of Firm by ThesanthoshputhoorNo ratings yet

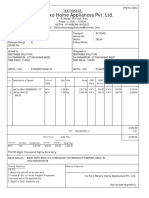

- 3 Sales Invoice RelaxoDocument3 pages3 Sales Invoice RelaxoSantosh OjhaNo ratings yet

- GST in India: A Report on Goods and Services TaxDocument99 pagesGST in India: A Report on Goods and Services TaxcameyNo ratings yet

- Cori Preftakes Cash Flow Analysis ToolDocument6 pagesCori Preftakes Cash Flow Analysis ToolcpreftakesNo ratings yet

- Annex 37 - QSRP - CabangtalanDocument12 pagesAnnex 37 - QSRP - CabangtalanLikey PromiseNo ratings yet

- House Property Declaration - 2011-12Document2 pagesHouse Property Declaration - 2011-12Pradeep KumarNo ratings yet

- SME Taxation in EuropeDocument631 pagesSME Taxation in EuropeAnonymous 4x7MVHcNo ratings yet

- Core Plus Homeowner Relocation Package Summary: Component DescriptionDocument6 pagesCore Plus Homeowner Relocation Package Summary: Component DescriptionKaviayNo ratings yet

- Return of Income, Revised Return, Incomplete Return & Income Escaping AssessmentDocument7 pagesReturn of Income, Revised Return, Incomplete Return & Income Escaping AssessmentAjinkya NaikNo ratings yet

- 19-Financial Documents For Eligibility CheckDocument1 page19-Financial Documents For Eligibility CheckGLAIZA PALATINONo ratings yet

- Sam and Neneng capital contribution and profit sharing calculationsDocument19 pagesSam and Neneng capital contribution and profit sharing calculationsJasmine ActaNo ratings yet

- Receipt Voucher: Tvs Electronics LimitedDocument1 pageReceipt Voucher: Tvs Electronics LimitedKrishna SrivathsaNo ratings yet

- Consolidated StatementDocument1 pageConsolidated StatementParameswararao BillaNo ratings yet

- 57Document14 pages57Saif UzZol100% (1)

- Khush Fashion Palace: # Description Price Quantity Discount TotalDocument1 pageKhush Fashion Palace: # Description Price Quantity Discount TotalKarimPrinceAddoNo ratings yet

- BE4-1. The Adjusted Trial Balance of Pacific Scientific Corporation OnDocument10 pagesBE4-1. The Adjusted Trial Balance of Pacific Scientific Corporation OnNguyễn Linh NhiNo ratings yet

- Old RegimeDocument4 pagesOld RegimePRITHIKA DASGUPTA 19212441No ratings yet

- UntitledDocument9 pagesUntitledShohag AlamNo ratings yet

- What Is An ESOP Infographic 2022Document1 pageWhat Is An ESOP Infographic 2022Erwin MainsteinNo ratings yet