You might also like

- Public GoodsDocument41 pagesPublic GoodsYugeshPandayNo ratings yet

- Bureaucracy and Flypaper Effect PDFDocument30 pagesBureaucracy and Flypaper Effect PDFYugeshPandayNo ratings yet

- Bureaucracy and Flypaper Effect PDFDocument30 pagesBureaucracy and Flypaper Effect PDFYugeshPandayNo ratings yet

- Share Intergovernmental Grants Public Economics PDFDocument7 pagesShare Intergovernmental Grants Public Economics PDFYugeshPandayNo ratings yet

- The Flypaper Effect PDFDocument16 pagesThe Flypaper Effect PDFYugeshPandayNo ratings yet

- Ulrich HR Competency ModelsDocument6 pagesUlrich HR Competency ModelsYugeshPanday100% (1)

- Inruled Working Papers - Zep Mar2013Document50 pagesInruled Working Papers - Zep Mar2013YugeshPandayNo ratings yet

- Career Development and ManagementDocument14 pagesCareer Development and ManagementYugeshPandayNo ratings yet

- Why We Hate HRDocument8 pagesWhy We Hate HRYugeshPandayNo ratings yet

- Education Act 1957 of Mauritius (Amended)Document18 pagesEducation Act 1957 of Mauritius (Amended)Treep Dia100% (1)

- ExternalitiesDocument10 pagesExternalitiesYugeshPandayNo ratings yet

- OECD Paper On The Recruitment of TeachersDocument2 pagesOECD Paper On The Recruitment of TeachersYugeshPandayNo ratings yet

- 02 Alvesson 2e CH 02Document38 pages02 Alvesson 2e CH 02Akrivi PapadakiNo ratings yet

- Educational Change and Policy Transfer in Developing CountriesDocument19 pagesEducational Change and Policy Transfer in Developing CountriesYugeshPandayNo ratings yet

- STD 5 - Unit 1 - Our Natural Environment - To COMPLETEDocument9 pagesSTD 5 - Unit 1 - Our Natural Environment - To COMPLETEYugeshPandayNo ratings yet

- ICT and Education: Enabling Two Rural Western Kenyan Schools ToDocument6 pagesICT and Education: Enabling Two Rural Western Kenyan Schools ToYugeshPandayNo ratings yet

- African Leadership in ICTDocument54 pagesAfrican Leadership in ICTYugeshPanday100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CIT Vs Shree Meenakshi Mills LTDDocument6 pagesCIT Vs Shree Meenakshi Mills LTDKomalpreet KaurNo ratings yet

- Accounting Mcqs 3Document6 pagesAccounting Mcqs 3Mohd AyazNo ratings yet

- Don't Fight The Fed - A Wealth of Common SenseDocument4 pagesDon't Fight The Fed - A Wealth of Common SensebiddingersNo ratings yet

- John Hay People's Alternative Coalition Vs Lim - 119775 - October 24, 2003 - JDocument12 pagesJohn Hay People's Alternative Coalition Vs Lim - 119775 - October 24, 2003 - JFrances Ann TevesNo ratings yet

- The Original Version of James Tansey's Growing Pains ReportDocument19 pagesThe Original Version of James Tansey's Growing Pains ReportIan Young100% (1)

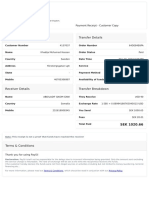

- Sender Details Transfer Details: Payment Receipt - CustomerDocument1 pageSender Details Transfer Details: Payment Receipt - CustomerAbshira Abdi AliNo ratings yet

- CV - FormatDocument2 pagesCV - FormatRafidul IslamNo ratings yet

- Partnership Formation and Dissolution Case StudyDocument13 pagesPartnership Formation and Dissolution Case StudyElma Joyce BondocNo ratings yet

- Jean-Louis Tourne PresentationDocument20 pagesJean-Louis Tourne PresentationeatnutesNo ratings yet

- Cib ExamDocument3 pagesCib ExamAhmed HakimNo ratings yet

- SAP Cutover PlanDocument32,767 pagesSAP Cutover PlanMichelle FossNo ratings yet

- Investment Decision RulesDocument14 pagesInvestment Decision RulesprashantgoruleNo ratings yet

- AOVPS7267Q - Show Cause Notice Us 270A - 1045781439 (1) - 21092022Document1 pageAOVPS7267Q - Show Cause Notice Us 270A - 1045781439 (1) - 21092022Basavaraj KorishettarNo ratings yet

- Cobcsrg Case 2Document20 pagesCobcsrg Case 2Sophia FernandezNo ratings yet

- Capital Markets Senior Vice President in New York City Resume David GrossmanDocument3 pagesCapital Markets Senior Vice President in New York City Resume David GrossmanDavidGrossman3No ratings yet

- Cup - AuditDocument7 pagesCup - AuditJerauld BucolNo ratings yet

- Value Driven Maintenance & Asset Management: Competing With Aging AssetsDocument5 pagesValue Driven Maintenance & Asset Management: Competing With Aging AssetsMILTON ANDRES ANGULO MORRISNo ratings yet

- Philippine Tax Exemption Form GuideDocument6 pagesPhilippine Tax Exemption Form GuideBobby Olavides SebastianNo ratings yet

- Rice Bistro Business PlanDocument69 pagesRice Bistro Business PlanChienny HocosolNo ratings yet

- Chapter 2 - The Accounting Equation and The Double Entry SystemDocument3 pagesChapter 2 - The Accounting Equation and The Double Entry SystemalonNo ratings yet

- Staff-Budget Preparation and ManagementDocument26 pagesStaff-Budget Preparation and ManagementRaniNo ratings yet

- Service Sector Growth in Bihar Driven by Telecom BoomDocument5 pagesService Sector Growth in Bihar Driven by Telecom BoomAditya KumarNo ratings yet

- Bank Loan Interest CalculatorDocument2 pagesBank Loan Interest CalculatorgodabariNo ratings yet

- Personal Assets: AssetDocument6 pagesPersonal Assets: AssetDipak NandeshwarNo ratings yet

- Provisions Of Companies Act 1956Document15 pagesProvisions Of Companies Act 19569986212378No ratings yet

- Narra Nickel Mining Vs Redmont PDFDocument35 pagesNarra Nickel Mining Vs Redmont PDFLemuel Angelo M. EleccionNo ratings yet

- Quick Tests Unit 1 and Unit 2Document47 pagesQuick Tests Unit 1 and Unit 2junjun100% (2)

- Zavyalova EkaterinaDocument82 pagesZavyalova EkaterinaPrashant SinghNo ratings yet

- BADM 510 Global Business Strategic ManagementDocument71 pagesBADM 510 Global Business Strategic Managementclarknj100% (1)