You might also like

- Tax on Property Transfer Below Market ValueDocument2 pagesTax on Property Transfer Below Market ValueJT GalNo ratings yet

- AI-KNOWLEDGE INSPIRATION TRAINING EVENTS INC. Articles of IncorporationDocument5 pagesAI-KNOWLEDGE INSPIRATION TRAINING EVENTS INC. Articles of IncorporationJT GalNo ratings yet

- Check ListDocument2 pagesCheck ListJT GalNo ratings yet

- Alv Answers To Sultan's QuestionsDocument2 pagesAlv Answers To Sultan's QuestionsJT GalNo ratings yet

- Documents Which Must Be Submitted Cornersteel Systems Corporation Per RMC 47Document2 pagesDocuments Which Must Be Submitted Cornersteel Systems Corporation Per RMC 47JT GalNo ratings yet

- LRA Circular No. 11-2002 - Schedule of Fess of The LRADocument16 pagesLRA Circular No. 11-2002 - Schedule of Fess of The LRAMelvin BanzonNo ratings yet

- Transfer of Rights Over Real Property Not Subject To Capital Gains Tax, BIR Ruling No. 083-99, (June 22, 1999Document2 pagesTransfer of Rights Over Real Property Not Subject To Capital Gains Tax, BIR Ruling No. 083-99, (June 22, 1999JT GalNo ratings yet

- Cases Ruling On The Admission of FOE Despite Failure To Timely File The SameDocument6 pagesCases Ruling On The Admission of FOE Despite Failure To Timely File The SameJT GalNo ratings yet

- What Are The Grounds For Filing A Criminal Complaint?Document3 pagesWhat Are The Grounds For Filing A Criminal Complaint?JT GalNo ratings yet

- Mendoza Antero & Associates: Sheriff Edmund RaguidDocument1 pageMendoza Antero & Associates: Sheriff Edmund RaguidJT GalNo ratings yet

- Amendment and Alteration of A Certificate of TitleDocument2 pagesAmendment and Alteration of A Certificate of TitleJT GalNo ratings yet

- Research Motion For ReconsiderationDocument4 pagesResearch Motion For ReconsiderationJT GalNo ratings yet

- En Banc: Resolution No. 9 - 2020Document2 pagesEn Banc: Resolution No. 9 - 2020JT GalNo ratings yet

- Republic Vs OrbecidoDocument1 pageRepublic Vs OrbecidoJT GalNo ratings yet

- Procedure For BIR MAKATIDocument5 pagesProcedure For BIR MAKATIJT GalNo ratings yet

- Erd.1.f.001 EeeDocument11 pagesErd.1.f.001 EeePaul GeorgeNo ratings yet

- Procedure For BIR MAKATIDocument5 pagesProcedure For BIR MAKATIJT GalNo ratings yet

- Comelec Gun BanDocument7 pagesComelec Gun BanJT GalNo ratings yet

- G.R. No. 175587 September 21, 2007 Philippine Commercial International Bank, Petitioner, Joseph Anthony M. Alejandro, RespondentDocument9 pagesG.R. No. 175587 September 21, 2007 Philippine Commercial International Bank, Petitioner, Joseph Anthony M. Alejandro, RespondentJT GalNo ratings yet

- 2 Ways of Committing Grave CoercionDocument2 pages2 Ways of Committing Grave Coercionrandolphken86% (14)

- VatDocument13 pagesVatJT GalNo ratings yet

- C.T.A. CASE NO. 9449. October 18, 2018Document25 pagesC.T.A. CASE NO. 9449. October 18, 2018JT GalNo ratings yet

- Comelec Gun BanDocument7 pagesComelec Gun BanJT GalNo ratings yet

- POS JurisprudenceDocument8 pagesPOS JurisprudenceJT GalNo ratings yet

- Labay Vs SandiganbayanDocument14 pagesLabay Vs SandiganbayanJT GalNo ratings yet

- Da Itad Bir Ruling No. 017-07Document13 pagesDa Itad Bir Ruling No. 017-07JT GalNo ratings yet

- Ao 186Document2 pagesAo 186JT GalNo ratings yet

- Deutche Bank CaseDocument3 pagesDeutche Bank CaseJT GalNo ratings yet

- Orbe Vs - FilivestDocument18 pagesOrbe Vs - FilivestJT GalNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Assignment 21 - EXERCISE 4.0Document2 pagesAssignment 21 - EXERCISE 4.0Ravi TNo ratings yet

- Contirbution For The Month of OCTOBER 2019Document6 pagesContirbution For The Month of OCTOBER 2019michael cadizNo ratings yet

- Syllabus - LABOR LAW 1-Atty. TiofiloDocument12 pagesSyllabus - LABOR LAW 1-Atty. TiofiloJeffrey MendozaNo ratings yet

- Canucks 2011-12 schedule and resultsDocument3 pagesCanucks 2011-12 schedule and resultsTBaby038392No ratings yet

- FAST TEK GROUP, LLC v. PLASTECH ENGINEERED PRODUCTS, INC. - Document No. 10Document2 pagesFAST TEK GROUP, LLC v. PLASTECH ENGINEERED PRODUCTS, INC. - Document No. 10Justia.comNo ratings yet

- 18 Financial StatementsDocument35 pages18 Financial Statementswsahmed28No ratings yet

- C C CC CCC !"#C CDocument4 pagesC C CC CCC !"#C CmojagminaNo ratings yet

- Adjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Document7 pagesAdjudication Order in Respect of Datar Switchgear LTD in The Matter of Non Redressal of Investor Complaints.Shyam SunderNo ratings yet

- Introduction To Philippine HistoryDocument20 pagesIntroduction To Philippine HistoryCatie Raw AyNo ratings yet

- DL Services Acknowledgement RohitDocument1 pageDL Services Acknowledgement RohitHoney SinghNo ratings yet

- Dhaka Club Areya BaseDocument63 pagesDhaka Club Areya BaseAbu Bakkar Siddiq100% (1)

- HR Executive - International HomewareDocument4 pagesHR Executive - International HomewareS.M. MohiuddinNo ratings yet

- Corporate Finance: Project ReportDocument10 pagesCorporate Finance: Project ReportNeha ShawNo ratings yet

- Rbi Guidelines On NRODocument6 pagesRbi Guidelines On NROGahininathJagannathGadeNo ratings yet

- Lista AuspiciadoresDocument2 pagesLista AuspiciadoresWanda MendezNo ratings yet

- Investment Pattern of Salaried Persons in MumbaiDocument62 pagesInvestment Pattern of Salaried Persons in MumbaiyopoNo ratings yet

- PR HawcoplastDocument2 pagesPR HawcoplastRohan JoshiNo ratings yet

- Robina Farms Cebu v. VillaDocument3 pagesRobina Farms Cebu v. VillaMaribel Nicole LopezNo ratings yet

- MCQDocument6 pagesMCQArup Kumar DasNo ratings yet

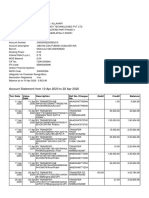

- Account activity and balance from 10 Apr to 22 AprDocument2 pagesAccount activity and balance from 10 Apr to 22 AprSRIDHAR allhari0% (1)

- Dáil Eireann Debate OF PESCO EU ARMY IN SECRETDocument488 pagesDáil Eireann Debate OF PESCO EU ARMY IN SECRETRita CahillNo ratings yet

- Petitioner MemorialDocument36 pagesPetitioner MemorialAshish singh86% (7)

- Solution Manual For Options Futures and Other Derivatives 10th Edition John C HullDocument24 pagesSolution Manual For Options Futures and Other Derivatives 10th Edition John C HullFeliciaJohnsonjode100% (49)

- Bocconi Financial Reporting and Analysis CourseworkDocument7 pagesBocconi Financial Reporting and Analysis CourseworkLuigi NocitaNo ratings yet

- Overview of Financial Services Act 2013Document11 pagesOverview of Financial Services Act 2013FatehahNo ratings yet

- Test Series: March, 2022 Mock Test Paper 1 Final Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionDocument10 pagesTest Series: March, 2022 Mock Test Paper 1 Final Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionDimple KhandheriaNo ratings yet

- Caselman DIY AMG + Multimedia (Copyleft)Document106 pagesCaselman DIY AMG + Multimedia (Copyleft)cliftoncage100% (1)

- Form GST Mov-02 Order For Physical VerificationDocument1 pageForm GST Mov-02 Order For Physical VerificationShruti SantoshNo ratings yet

- ETSO-C127a CS-ETSO 0Document6 pagesETSO-C127a CS-ETSO 0Anurag MishraNo ratings yet

- Psref 325Document285 pagesPsref 325Alex OmegaNo ratings yet