You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Tax1 Syllabus SY 2021-2022Document31 pagesTax1 Syllabus SY 2021-2022Shanon Cristy GacaNo ratings yet

- Quicknotes in Income TaxDocument13 pagesQuicknotes in Income TaxTrelle DiazNo ratings yet

- 2019legislation - RA 11232 REVISED CORPORATION CODE 2019 PDFDocument73 pages2019legislation - RA 11232 REVISED CORPORATION CODE 2019 PDFCris Anonuevo100% (1)

- Pre-Trial & Rights of The AccusedDocument112 pagesPre-Trial & Rights of The AccusedShiela AdlawanNo ratings yet

- QDEDocument14 pagesQDEShiela AdlawanNo ratings yet

- Income Tax Final Exam 1st Sem 2019 2020 BSA PDFDocument11 pagesIncome Tax Final Exam 1st Sem 2019 2020 BSA PDFMae Dela Pena100% (1)

- Final Taxation PreboardDocument14 pagesFinal Taxation PreboardEmerita Modesto25% (4)

- Chapter 13 Principles of DeductionDocument5 pagesChapter 13 Principles of DeductionJason Mables100% (1)

- Income Tax Schemes, Accounting Periods, Accounting Methods and Reporting C4Document73 pagesIncome Tax Schemes, Accounting Periods, Accounting Methods and Reporting C4Diane CassionNo ratings yet

- DOJ Circular No. 70Document3 pagesDOJ Circular No. 70Sharmen Dizon Gallenero100% (1)

- Sec Memo No. 8, s2013Document2 pagesSec Memo No. 8, s2013Jennilyn TugelidaNo ratings yet

- 2nd TAX SYLLABUS - CONTINUATIONDocument5 pages2nd TAX SYLLABUS - CONTINUATIONShiela AdlawanNo ratings yet

- TAX SYLLABUS With NOTESDocument41 pagesTAX SYLLABUS With NOTESShiela AdlawanNo ratings yet

- CASES Arrange Per YearDocument1 pageCASES Arrange Per YearShiela AdlawanNo ratings yet

- Part 4 Cases (Full Text)Document5 pagesPart 4 Cases (Full Text)Shiela AdlawanNo ratings yet

- LTD SYLLABUS With NOTESSDocument9 pagesLTD SYLLABUS With NOTESSShiela AdlawanNo ratings yet

- Corpo DoctrinesDocument40 pagesCorpo DoctrinesShiela AdlawanNo ratings yet

- (6-6-91) Sec Op Sacred Heart Memorial CorpDocument2 pages(6-6-91) Sec Op Sacred Heart Memorial CorpShiela AdlawanNo ratings yet

- G.R. No. 164317 - Ching v. Secretary of JusticeDocument33 pagesG.R. No. 164317 - Ching v. Secretary of JusticePatrick D GuetaNo ratings yet

- Interport Resources Corp Vs Securities Specialists, Inc., 792 SCRA 155 (2016)Document9 pagesInterport Resources Corp Vs Securities Specialists, Inc., 792 SCRA 155 (2016)Shiela AdlawanNo ratings yet

- Powell 1994 PDFDocument33 pagesPowell 1994 PDFJhosiel GarcíaNo ratings yet

- Wilson Gamboa V Secretary Teves, GR No. 176579, June 28, 2011Document35 pagesWilson Gamboa V Secretary Teves, GR No. 176579, June 28, 2011Shiela AdlawanNo ratings yet

- ABS-CBN V Gozon, 753 SCRA 1 (2015)Document23 pagesABS-CBN V Gozon, 753 SCRA 1 (2015)Shiela AdlawanNo ratings yet

- Filipinas Broadcasting Network V AMEC-BCCM, GR 141994, January 17, 2005Document11 pagesFilipinas Broadcasting Network V AMEC-BCCM, GR 141994, January 17, 2005Shiela AdlawanNo ratings yet

- ABS-CBN V Court of Appeals, 301 SCRA 589 (1999)Document19 pagesABS-CBN V Court of Appeals, 301 SCRA 589 (1999)Shiela AdlawanNo ratings yet

- Asset Privatization Trust V Court of Appeals, 300 SCRA 579 (1998) PDFDocument41 pagesAsset Privatization Trust V Court of Appeals, 300 SCRA 579 (1998) PDFShiela AdlawanNo ratings yet

- 22.2 Resolution - Gamboa - v. - TevesDocument105 pages22.2 Resolution - Gamboa - v. - TevesShiela AdlawanNo ratings yet

- First Lepanto-Taisho Insurance Corporation V Chevron, 663 SCRA 309 (2012)Document8 pagesFirst Lepanto-Taisho Insurance Corporation V Chevron, 663 SCRA 309 (2012)Shiela AdlawanNo ratings yet

- Full Text PropertyDocument32 pagesFull Text PropertyShiela AdlawanNo ratings yet

- Intro ReportDocument24 pagesIntro ReportShiela AdlawanNo ratings yet

- Full Text PropertyDocument32 pagesFull Text PropertyShiela AdlawanNo ratings yet

- Submitted To: Ms. Faria AkterDocument11 pagesSubmitted To: Ms. Faria Akterfarzana mahmudNo ratings yet

- WESTERN MINOLCO CORPORATION v. CIRDocument8 pagesWESTERN MINOLCO CORPORATION v. CIRKhate AlonzoNo ratings yet

- Inventories: Additional Valuation Issues Answers To QuestionsDocument60 pagesInventories: Additional Valuation Issues Answers To QuestionsMaldin JeremiaNo ratings yet

- Allowable Deductions SEC. 86. Computation of Net Estate. - For The Purpose of The Tax Imposed in ThisDocument5 pagesAllowable Deductions SEC. 86. Computation of Net Estate. - For The Purpose of The Tax Imposed in ThisJenny Rose Castro FernandezNo ratings yet

- Paper Industries Corporation of The PhilippinesDocument3 pagesPaper Industries Corporation of The PhilippinesCalagui Tejano Glenda JaygeeNo ratings yet

- Handout - 03 CorporationDocument10 pagesHandout - 03 CorporationKiyo KoNo ratings yet

- TAX QsDocument131 pagesTAX QsUser 010897020197No ratings yet

- PT Unitex LaptahunanDocument108 pagesPT Unitex LaptahunanbereniceNo ratings yet

- 10 Consolidated Mines, Inc. Vs Commissioner of Internal RevenueDocument21 pages10 Consolidated Mines, Inc. Vs Commissioner of Internal RevenueHey it's RayaNo ratings yet

- Financial Position of Nishat Mills LimitedDocument87 pagesFinancial Position of Nishat Mills Limitedzeshan khaliq80% (5)

- An Overall Financial Analysis of Tesla: Jingyuan FangDocument6 pagesAn Overall Financial Analysis of Tesla: Jingyuan FangShahmala PerabuNo ratings yet

- MCQs On Taxation LawDocument18 pagesMCQs On Taxation LawAli Asghar RindNo ratings yet

- FA - Quiz1 - Answers - All VersionDocument22 pagesFA - Quiz1 - Answers - All VersionAgANo ratings yet

- Slides On The Ethiopian Tax System2Document26 pagesSlides On The Ethiopian Tax System2yebegashetNo ratings yet

- RMC No 67-2012Document5 pagesRMC No 67-2012evilminionsattackNo ratings yet

- Western Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Document2 pagesWestern Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Marc William SorianoNo ratings yet

- Chapter 5 - Corporate Income Tax A. Corporations Subject To Income TaxDocument2 pagesChapter 5 - Corporate Income Tax A. Corporations Subject To Income TaxPJDNo ratings yet

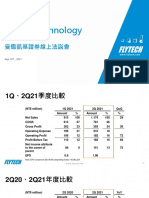

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Allowable DeductionsDocument4 pagesAllowable DeductionsdailydoseoflawNo ratings yet

- Income Tax Calculator 2013-14Document2 pagesIncome Tax Calculator 2013-14kirang gandhiNo ratings yet

- 3RD Year Diagnostic ExamDocument30 pages3RD Year Diagnostic ExamRoisu De KuriNo ratings yet

- Beleza NaturalDocument22 pagesBeleza NaturalTejas MahajanNo ratings yet

- Special CorporationsDocument12 pagesSpecial CorporationsDinah BaluyutNo ratings yet

- Long QuizDocument14 pagesLong QuizMaritesNo ratings yet