You might also like

- CFA FlashcardsDocument258 pagesCFA FlashcardsBrook Rene Johnson71% (7)

- Profit & Loss Statement: O' Lites GymDocument8 pagesProfit & Loss Statement: O' Lites GymNoorulain Adnan100% (5)

- Project Report On Boutique ShopDocument16 pagesProject Report On Boutique ShopKhandaker Sakib Farhad33% (3)

- Ford Motor Company's Value Enhancement PlanDocument20 pagesFord Motor Company's Value Enhancement PlanIvaylo VasilevNo ratings yet

- Statement of Comprehensive IncomeDocument11 pagesStatement of Comprehensive IncomeKhiezna PakamNo ratings yet

- Project Finance Modelling PDFDocument86 pagesProject Finance Modelling PDFspranga5100% (5)

- 07 JUNE AnswersDocument10 pages07 JUNE Answerskhengmai50% (2)

- Cost-Volume-Profit Relationships: Solutions To QuestionsDocument90 pagesCost-Volume-Profit Relationships: Solutions To QuestionsKathryn Teo100% (1)

- Cost Analysis Sheet DaburDocument11 pagesCost Analysis Sheet DaburrohitNo ratings yet

- KPMG Technical Terms Commercial Accounting and Tax LawDocument44 pagesKPMG Technical Terms Commercial Accounting and Tax LawIosias100% (3)

- R&D Productivity: How to Target It. How to Measure It. Why It Matters.From EverandR&D Productivity: How to Target It. How to Measure It. Why It Matters.No ratings yet

- Business Mathematics: Quarter 1, Week 6 - Module 9 Describing How Gross Margin Is Used in Sales - ABM - BM11BS-Ih-4Document14 pagesBusiness Mathematics: Quarter 1, Week 6 - Module 9 Describing How Gross Margin Is Used in Sales - ABM - BM11BS-Ih-4Dave Sulam100% (2)

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingMohtasim Bin HabibNo ratings yet

- TugasDocument1 pageTugasMiftachul NgazizNo ratings yet

- GSBA002 - Management Accounting - Realyn Austria - Case Study 3BDocument4 pagesGSBA002 - Management Accounting - Realyn Austria - Case Study 3BRealyn AustriaNo ratings yet

- 8463035Document2 pages8463035SasisomWilaiwanNo ratings yet

- Computation of Gross ProfitDocument15 pagesComputation of Gross ProfitAnnely Jane DarbeNo ratings yet

- A. Calculate The Break-Even Dollar Sales For The MonthDocument25 pagesA. Calculate The Break-Even Dollar Sales For The MonthPriyankaNo ratings yet

- Statement: Comprehensive IncomeDocument11 pagesStatement: Comprehensive IncomeAngela Cuevas DimaanoNo ratings yet

- Cfa3 1Document2 pagesCfa3 1Trinh NguyễnNo ratings yet

- AFD Practice QuestionsDocument3 pagesAFD Practice QuestionsChandanaNo ratings yet

- Kraft Heinz Case VF PDFDocument5 pagesKraft Heinz Case VF PDFNadine ElNo ratings yet

- Accounts Case StudyDocument9 pagesAccounts Case Studydhiraj agarwalNo ratings yet

- Ebook Build More Profitable BusinessDocument11 pagesEbook Build More Profitable BusinessMagnusNo ratings yet

- ACT2111 Fall 2019 Ch6 - Lecture 9&10 - StudentDocument62 pagesACT2111 Fall 2019 Ch6 - Lecture 9&10 - StudentKevinNo ratings yet

- CH 5 - AdjustmentsDocument24 pagesCH 5 - Adjustmentsmuhamad elmiNo ratings yet

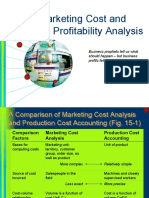

- Marketing Cost and Profitability AnalysisDocument10 pagesMarketing Cost and Profitability AnalysisBharathi RajuNo ratings yet

- Chapter 8 Case Study 8 6Document4 pagesChapter 8 Case Study 8 6mryanncarol.23No ratings yet

- Cost-Volume-Profit Relationships: Mcgraw-Hill /irwinDocument15 pagesCost-Volume-Profit Relationships: Mcgraw-Hill /irwinHibaaq AxmedNo ratings yet

- AA13nEvnnProfitnandnLoss 81614b548292ead Rap 69Document8 pagesAA13nEvnnProfitnandnLoss 81614b548292ead Rap 69jhon alexander bermudez malaverNo ratings yet

- CaseDocument7 pagesCaseAmer Wagdy GergesNo ratings yet

- Ummary of Study Objectives: 198 Financial StatementsDocument5 pagesUmmary of Study Objectives: 198 Financial StatementsYun ChandoraNo ratings yet

- Income Statement Ratios Analysis Ratios FormulaeDocument4 pagesIncome Statement Ratios Analysis Ratios FormulaeMousse1995No ratings yet

- Chapter 3 - Understanding The Income StatementDocument68 pagesChapter 3 - Understanding The Income StatementNguyễn Yến NhiNo ratings yet

- Session 5 Financial Statement Analysis Part 1-2Document17 pagesSession 5 Financial Statement Analysis Part 1-2Prakriti ChaturvediNo ratings yet

- ROE Disaggregation Exercise - P&GDocument3 pagesROE Disaggregation Exercise - P&GPepe GeoNo ratings yet

- Case CDocument100 pagesCase CAmer Wagdy GergesNo ratings yet

- Rap 69 Aa13 InglesDocument6 pagesRap 69 Aa13 InglesCristina GalvezNo ratings yet

- Case Descriptive Solve 2Document8 pagesCase Descriptive Solve 2rocken samiunNo ratings yet

- Accounting Slides Income StatmentDocument20 pagesAccounting Slides Income StatmentEdouard Rivet-BonjeanNo ratings yet

- Costing MethodsDocument79 pagesCosting MethodsemmaNo ratings yet

- Job Order CostingDocument5 pagesJob Order CostingNishanth PrabhakarNo ratings yet

- M/s. XYZ: About Your Valuation ReportDocument16 pagesM/s. XYZ: About Your Valuation ReportBhushan GowdaNo ratings yet

- LLH9e Chapter - 13Document30 pagesLLH9e Chapter - 13shakeDNo ratings yet

- Rights Reserved: Part III: Ancillary TopicsDocument13 pagesRights Reserved: Part III: Ancillary TopicsJane Michelle EmanNo ratings yet

- AA13nEvnnProfitnandnLoss 1062acee1603d0eDocument6 pagesAA13nEvnnProfitnandnLoss 1062acee1603d0eCristina GalvezNo ratings yet

- Profitability: 2008 2010 Operating Profit Margin (%)Document4 pagesProfitability: 2008 2010 Operating Profit Margin (%)prarak7283No ratings yet

- Akuntansi Sektor PublikDocument90 pagesAkuntansi Sektor PublikFicky ZulandoNo ratings yet

- What Is A Profit and Loss (P&L) Statement - InvestopediaDocument16 pagesWhat Is A Profit and Loss (P&L) Statement - InvestopediaFrancisco Del PuertoNo ratings yet

- CIEM5160 - Ch3 - IS & SREDocument30 pagesCIEM5160 - Ch3 - IS & SREMatthew LiNo ratings yet

- Enterp7a Financial MGMTDocument17 pagesEnterp7a Financial MGMTVanessa Tattao IsagaNo ratings yet

- Financial Management Toy World, Inc. Case Analysis Final ReportDocument9 pagesFinancial Management Toy World, Inc. Case Analysis Final ReportGagan Deep SinghNo ratings yet

- Taiho Plastics Industries Private LimitedDocument3 pagesTaiho Plastics Industries Private LimitedDonrost Ducusin Dulatre100% (1)

- IAS 8 - Net Profit or Loss For The Period, Fundamental Errors and Changes in Accounting PoliciesDocument11 pagesIAS 8 - Net Profit or Loss For The Period, Fundamental Errors and Changes in Accounting PoliciesPlatonicNo ratings yet

- Particulars Observation InferenceDocument2 pagesParticulars Observation InferenceChetan KejriwalNo ratings yet

- Hi Growth FixedDocument36 pagesHi Growth FixedVikram GulatiNo ratings yet

- Chapter 2. Financial Mangerial ReportingDocument9 pagesChapter 2. Financial Mangerial Reportingnaveen728No ratings yet

- EBIT Revenue COGS Operating Expenses or EBIT Net Income + Interest + Taxes Where: COGS Cost of Goods SoldDocument3 pagesEBIT Revenue COGS Operating Expenses or EBIT Net Income + Interest + Taxes Where: COGS Cost of Goods SoldLeahC.No ratings yet

- Objectives of Cost-Volume-Profit AnalysisDocument7 pagesObjectives of Cost-Volume-Profit AnalysisAnonNo ratings yet

- Revision - Income Stat and BS - V3Document4 pagesRevision - Income Stat and BS - V3betyibtihal03No ratings yet

- Principles of AccountingDocument19 pagesPrinciples of AccountingDarryl HungweNo ratings yet

- Are Depreciation and Amortization Included in Gross Profit - InvestopediaDocument5 pagesAre Depreciation and Amortization Included in Gross Profit - InvestopediaBob KaneNo ratings yet

- TutorialDocument3 pagesTutorialEliciaNo ratings yet

- Définition Du Mot EBITDocument32 pagesDéfinition Du Mot EBITpaterson djedoNo ratings yet

- 16 2 Prestige Telephone CompanyDocument3 pages16 2 Prestige Telephone CompanyAnunobi JaneNo ratings yet

- The Income StatementDocument13 pagesThe Income StatementPao VuochneaNo ratings yet

- 33 Assignment7Document6 pages33 Assignment7SasisomWilaiwanNo ratings yet

- Tijuana Bronze MachiningDocument6 pagesTijuana Bronze MachiningSasisomWilaiwanNo ratings yet

- Reichard Maschinen, GMBHDocument23 pagesReichard Maschinen, GMBHSasisomWilaiwanNo ratings yet

- 14 Assignment4Document5 pages14 Assignment4SasisomWilaiwanNo ratings yet

- Reichard Maschinen, GMBHDocument4 pagesReichard Maschinen, GMBHSasisomWilaiwanNo ratings yet

- 9 Assignment3Document15 pages9 Assignment3SasisomWilaiwanNo ratings yet

- Assignment1 2Document5 pagesAssignment1 2SasisomWilaiwanNo ratings yet

- Profit Percentage Excel Template: Visit: EmailDocument5 pagesProfit Percentage Excel Template: Visit: EmailMustafa Ricky Pramana SeNo ratings yet

- Ch3 - Batch - Exercises and SolutionDocument9 pagesCh3 - Batch - Exercises and Solution黃群睿No ratings yet

- Chapter 22 Share CapitalDocument25 pagesChapter 22 Share CapitalHammad AhmadNo ratings yet

- Activity 2 - 4B UpdatesDocument3 pagesActivity 2 - 4B UpdatesAngelo HilomaNo ratings yet

- Accounting For ManufacturingDocument12 pagesAccounting For ManufacturingAira Nhaire Cortez MecateNo ratings yet

- Cost of Manuf ScheduleDocument2 pagesCost of Manuf Scheduleebat11No ratings yet

- Solution:: January 1 0.16 May 1 0.18 July 1 0.20 October 1 0.21 December 31 0.22 Average For The Year 0.19Document19 pagesSolution:: January 1 0.16 May 1 0.18 July 1 0.20 October 1 0.21 December 31 0.22 Average For The Year 0.19Germayne GaluraNo ratings yet

- Partnership (Basic Concepts)Document33 pagesPartnership (Basic Concepts)MERRY DONNo ratings yet

- Coa C2017-004Document8 pagesCoa C2017-004Tom Louis HerreraNo ratings yet

- Income-Statement SampleDocument7 pagesIncome-Statement SampleShilpa NNo ratings yet

- Petron F (1) .S 3Document74 pagesPetron F (1) .S 3cieloville06100% (1)

- Rodell Accounts 20032004Document13 pagesRodell Accounts 20032004unlockdemocracyNo ratings yet

- Chapter 4 To 6 MillanDocument27 pagesChapter 4 To 6 MillanAlona MeladNo ratings yet

- Lahore School of Economics. Advance Corporate Finance. MBA II - Winter 2014. Dr. Sohail ZafarDocument6 pagesLahore School of Economics. Advance Corporate Finance. MBA II - Winter 2014. Dr. Sohail Zafarsarakhan0622No ratings yet

- Intermediate Examination Syllabus 2016 Paper 5: Financial Accounting (Fac)Document17 pagesIntermediate Examination Syllabus 2016 Paper 5: Financial Accounting (Fac)Bharat ThackerNo ratings yet

- Mabola TradingDocument2 pagesMabola TradingStye Sense PhNo ratings yet

- Final Account of Joint Stock CompanyDocument8 pagesFinal Account of Joint Stock CompanyanupsuchakNo ratings yet

- AFM SyllabusDocument3 pagesAFM SyllabusUtsav GhulatiNo ratings yet

- Fdocuments - in PPT On Nahar 1Document34 pagesFdocuments - in PPT On Nahar 1Rajni kalraNo ratings yet

- MGT101 GDB 1 SolutionDocument3 pagesMGT101 GDB 1 Solutionabid princeNo ratings yet

- NBP Unconsolidated Financial Statements 2015Document105 pagesNBP Unconsolidated Financial Statements 2015Asif RafiNo ratings yet

- Busininess Math Chapter 3 1 PDFDocument57 pagesBusininess Math Chapter 3 1 PDFAngela Miles DizonNo ratings yet