You might also like

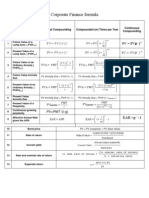

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Acute Ankle Sprain - An UpdateDocument7 pagesAcute Ankle Sprain - An UpdateFran Leiva CorreaNo ratings yet

- Calculus For EngineersDocument268 pagesCalculus For EngineersSr_Tabosa100% (1)

- Probability Cheatsheet 140718Document7 pagesProbability Cheatsheet 140718Mohit Agrawal100% (1)

- Exam FM QuestioonsDocument102 pagesExam FM Questioonsnkfran100% (1)

- Stats 101c Final ProjectDocument16 pagesStats 101c Final Projectapi-362845526100% (1)

- Characteristics of An Effective CounselorDocument5 pagesCharacteristics of An Effective CounselorAbbas KhanNo ratings yet

- VN Salary Guide 2020Document28 pagesVN Salary Guide 2020Raven NgoNo ratings yet

- Introduction To Econometrics With RDocument400 pagesIntroduction To Econometrics With RHervé DakpoNo ratings yet

- Multiple Regression Analysis: I 0 1 I1 K Ik IDocument30 pagesMultiple Regression Analysis: I 0 1 I1 K Ik Iajayikayode100% (1)

- Logistic RegressionDocument21 pagesLogistic RegressionDaneil RadcliffeNo ratings yet

- 1694600777-Unit2.2 Logistic Regression CU 2.0Document37 pages1694600777-Unit2.2 Logistic Regression CU 2.0prime9316586191100% (1)

- Environmental Sustainability Assessment of An Academic Institution in Calamba CityDocument29 pagesEnvironmental Sustainability Assessment of An Academic Institution in Calamba CityAmadeus Fernando M. PagenteNo ratings yet

- Historical CriticismDocument1 pageHistorical CriticismPatricia Ann Dulce Ambata67% (3)

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- CS229 Lecture on Supervised Learning and ClassificationDocument35 pagesCS229 Lecture on Supervised Learning and ClassificationAmr Abbas100% (1)

- Scikit-Learn Cheat Sheet For Preprocessing And Evaluating Machine Learning ModelsDocument1 pageScikit-Learn Cheat Sheet For Preprocessing And Evaluating Machine Learning ModelsLourdes Victoria Urrutia100% (1)

- Feedback - Logistic Regression HelpDocument5 pagesFeedback - Logistic Regression HelpChinmay Bhushan100% (1)

- EDA Lecture Module 2Document42 pagesEDA Lecture Module 2WINORLOSE100% (1)

- 1.1 Simple Linear Regression ModelDocument15 pages1.1 Simple Linear Regression Modelanshuman kandari100% (1)

- Logistic Regression: Gunjan Bharadwaj Assistant Professor Dept of CEADocument42 pagesLogistic Regression: Gunjan Bharadwaj Assistant Professor Dept of CEARahul Singh100% (1)

- Logistic RegressionDocument30 pagesLogistic RegressionBharath100% (1)

- Lecture 4 Linear RegressionDocument44 pagesLecture 4 Linear Regressioniamboss086100% (1)

- PytutorialDocument134 pagesPytutorialbernardinusheri100% (1)

- QuantEconlectures Python3 PDFDocument1,125 pagesQuantEconlectures Python3 PDFKaik Wulck Bassanelli100% (1)

- Linear Regression Model FundamentalsDocument20 pagesLinear Regression Model FundamentalsOmkar Todkar100% (1)

- Student Booklet For Sep 2015 v6Document50 pagesStudent Booklet For Sep 2015 v6radebp100% (1)

- Approaching ML ProblemsDocument300 pagesApproaching ML ProblemsIkram Laaroussi100% (1)

- MLR 3 BookDocument291 pagesMLR 3 BookPsic. Dra. Marina Moreno100% (1)

- TutorDocument309 pagesTutorravibtlit100% (1)

- Python For You and Me: Release 0.3.alpha1Document143 pagesPython For You and Me: Release 0.3.alpha1Zafar Ansari100% (1)

- Python 27Document162 pagesPython 27vaka82100% (1)

- Informatics Practices: Numpy - ArrayDocument28 pagesInformatics Practices: Numpy - ArrayAmit Kumar100% (1)

- Machine Learning (Analytics Vidhya) : What Is Logistic Regression?Document5 pagesMachine Learning (Analytics Vidhya) : What Is Logistic Regression?pradeep100% (1)

- LPTHWDocument220 pagesLPTHWBannuru Rafiq100% (1)

- 7. Heteroscedasticity: y = β + β x + · · · + β x + uDocument21 pages7. Heteroscedasticity: y = β + β x + · · · + β x + uajayikayode100% (1)

- Statistics Formulas CheatsheetDocument2 pagesStatistics Formulas Cheatsheetsonsuzakadarccc100% (1)

- 18.6501x Fundamentals of StatisticsDocument8 pages18.6501x Fundamentals of StatisticsAlexander CTO100% (1)

- Introduction To Basics of Machine Learning Algorithms: Pankaj OliDocument13 pagesIntroduction To Basics of Machine Learning Algorithms: Pankaj OliPankaj Oli100% (1)

- H-311 Linear Regression Analysis With RDocument71 pagesH-311 Linear Regression Analysis With RNat Boltu100% (1)

- Python Guide to Science and Machine LearningDocument108 pagesPython Guide to Science and Machine LearningOtto Nielsen100% (1)

- Scip y LecturesDocument329 pagesScip y Lecturesv100% (1)

- ML ProjectDocument57 pagesML ProjectPranav Viswanathan100% (1)

- Arrays in PythonDocument32 pagesArrays in Pythoneimaan afroz100% (1)

- Python Intro to Data AnalysisDocument34 pagesPython Intro to Data AnalysisGargi Jana100% (1)

- Decision Tree Classification ExplainedDocument11 pagesDecision Tree Classification Explainedvikas dhale100% (1)

- In All The Regression Models That We Have Considered SoDocument52 pagesIn All The Regression Models That We Have Considered SoMohammed Siyah100% (1)

- ML Microsoft Course Overview: Machine Learning in ContextDocument53 pagesML Microsoft Course Overview: Machine Learning in Contextnandex777100% (1)

- Import AsDocument27 pagesImport AsFozia Dawood100% (1)

- Sas Notes Module 4-Categorical Data Analysis Testing Association Between Categorical VariablesDocument16 pagesSas Notes Module 4-Categorical Data Analysis Testing Association Between Categorical VariablesNISHITA MALPANI100% (1)

- Numpy Basics CheatsheetDocument1 pageNumpy Basics CheatsheetAkshay Yawale100% (1)

- Linear Regression Chap01Document7 pagesLinear Regression Chap01israel14548100% (1)

- Linear RegressionDocument51 pagesLinear RegressionKunal Langer100% (1)

- Essential Python Cheat Sheet: SschaubDocument11 pagesEssential Python Cheat Sheet: SschaubOusmane Diamari100% (1)

- Data Transformation With Dplyr - CheatsheetDocument2 pagesData Transformation With Dplyr - CheatsheetGirish Chadha100% (1)

- CSE3506 Logistic Regression Predicts Red Wine QualityDocument10 pagesCSE3506 Logistic Regression Predicts Red Wine QualityShivam Batra100% (1)

- Linear Regression With LM Function, Diagnostic Plots, Interaction Term, Non-Linear Transformation of The Predictors, Qualitative PredictorsDocument15 pagesLinear Regression With LM Function, Diagnostic Plots, Interaction Term, Non-Linear Transformation of The Predictors, Qualitative Predictorskeexuepin100% (1)

- MLT Unit 3Document38 pagesMLT Unit 3iamutkarshdube100% (1)

- Classification with Decision Trees: Choosing the Best Splitting AttributeDocument62 pagesClassification with Decision Trees: Choosing the Best Splitting Attributemalik_genius100% (1)

- Correlation & Regression AnalysisDocument39 pagesCorrelation & Regression AnalysisAbhipreeth Mehra100% (1)

- Logistic RegressionDocument17 pagesLogistic RegressionLovedeep Chaudhary100% (1)

- Z Transforms: Raising A New Generation of LeadersDocument33 pagesZ Transforms: Raising A New Generation of Leadersmngueter100% (1)

- Probability and Statistics: Cheat SheetDocument10 pagesProbability and Statistics: Cheat Sheetmrbook79100% (1)

- Sajjad DSDocument97 pagesSajjad DSHey Buddy100% (1)

- Correlation & RegressionDocument53 pagesCorrelation & Regressionvhj jhhj100% (1)

- Stat1012 Cheatsheet Double-SidedDocument2 pagesStat1012 Cheatsheet Double-SidedNicholas So100% (1)

- CS 229, Public Course Problem Set #4 Solutions: Unsupervised Learn-Ing and Reinforcement LearningDocument12 pagesCS 229, Public Course Problem Set #4 Solutions: Unsupervised Learn-Ing and Reinforcement Learninglalm9931No ratings yet

- Statistics 580 Maximum Likelihood Estimation: 1 2 N 0 N 1 P 0 PDocument25 pagesStatistics 580 Maximum Likelihood Estimation: 1 2 N 0 N 1 P 0 PTawsif HasanNo ratings yet

- Tables of The Legendre Functions P—½+it(x): Mathematical Tables SeriesFrom EverandTables of The Legendre Functions P—½+it(x): Mathematical Tables SeriesNo ratings yet

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)From EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)No ratings yet

- MFE SampleQS1-76Document185 pagesMFE SampleQS1-76Jihyeon Kim100% (1)

- Stolyarov MFE Study Guide PDFDocument279 pagesStolyarov MFE Study Guide PDFSachin SomaniNo ratings yet

- 1 Exam FM QuestionsDocument36 pages1 Exam FM QuestionsMiguel Grau100% (1)

- GMAC 09LLCAgreementDocument100 pagesGMAC 09LLCAgreementHoaNo ratings yet

- SOA MFE 76 Practice Ques SolsDocument70 pagesSOA MFE 76 Practice Ques SolsGracia DongNo ratings yet

- Exam FM Sample SolutionsDocument56 pagesExam FM Sample SolutionsJessica NoviaNo ratings yet

- A Prlmal Algorithm For Interval Linear-Programming ProblemsDocument14 pagesA Prlmal Algorithm For Interval Linear-Programming ProblemsHông HoaNo ratings yet

- LTAM01 - Chap 2 - Assignment PDFDocument10 pagesLTAM01 - Chap 2 - Assignment PDFHông HoaNo ratings yet

- The Gauss-Markov Theorem in Anal Sis by L. Eaton of of Echnical 422Document36 pagesThe Gauss-Markov Theorem in Anal Sis by L. Eaton of of Echnical 422Hông HoaNo ratings yet

- Stat 5102 Lecture Slides: Deck 6 Gauss-Markov Theorem, Sufficiency, Generalized Linear Models, Likelihood Ratio Tests, Categorical Data AnalysisDocument86 pagesStat 5102 Lecture Slides: Deck 6 Gauss-Markov Theorem, Sufficiency, Generalized Linear Models, Likelihood Ratio Tests, Categorical Data AnalysisHông HoaNo ratings yet

- Fap Module ObjectivesDocument25 pagesFap Module ObjectivesHông HoaNo ratings yet

- Naval Shore Activities Manpower Forecasting ModelsDocument72 pagesNaval Shore Activities Manpower Forecasting ModelsHông HoaNo ratings yet

- Main PDFDocument7 pagesMain PDFMukminin BaharuddinNo ratings yet

- 2021 04 Exam FM SyllabiDocument10 pages2021 04 Exam FM SyllabiHông HoaNo ratings yet

- 2020 6 19 Exam Pa Project Statement PDFDocument6 pages2020 6 19 Exam Pa Project Statement PDFHông HoaNo ratings yet

- Edu 2020 02 FM Percents Ogu4ljDocument1 pageEdu 2020 02 FM Percents Ogu4ljHông HoaNo ratings yet

- Chapter 4. Gauss-Markov ModelDocument20 pagesChapter 4. Gauss-Markov ModelHông HoaNo ratings yet

- Prudential Supervision ENDocument9 pagesPrudential Supervision ENHông HoaNo ratings yet

- 2020 6 17 Exam Pa Project Statement PDFDocument6 pages2020 6 17 Exam Pa Project Statement PDFHông HoaNo ratings yet

- Exam Pa 06 17 Model Solution PDFDocument21 pagesExam Pa 06 17 Model Solution PDFHông HoaNo ratings yet

- Exam Pa 06 16 Model Solution PDFDocument18 pagesExam Pa 06 16 Model Solution PDFHông HoaNo ratings yet

- Exam Pa 06 19 Model SolutionDocument17 pagesExam Pa 06 19 Model SolutionHông HoaNo ratings yet

- 2020 6 19 Exam Pa Project Statement PDFDocument6 pages2020 6 19 Exam Pa Project Statement PDFHông HoaNo ratings yet

- With All Their Worldly Possessions - A Story Connecting The Rees, Deslandes, Jardine and Nelson Families and Their Emigration To Australia in The 1850s - Glendon O'ConnorDocument382 pagesWith All Their Worldly Possessions - A Story Connecting The Rees, Deslandes, Jardine and Nelson Families and Their Emigration To Australia in The 1850s - Glendon O'ConnorGlendon O'ConnorNo ratings yet

- PDF Microsite Achieve Global AG Survey of Sales EffectivenessDocument44 pagesPDF Microsite Achieve Global AG Survey of Sales Effectivenessingrid_walrabensteinNo ratings yet

- Consortium of National Law Universities: Provisional 5th List - CLAT 2021 - PGDocument3 pagesConsortium of National Law Universities: Provisional 5th List - CLAT 2021 - PGLNo ratings yet

- Marketing Management-MY KhanDocument102 pagesMarketing Management-MY KhansujeetleopardNo ratings yet

- MODULE 3 - Revisiting The ClassicsDocument22 pagesMODULE 3 - Revisiting The ClassicsSneha MichaelNo ratings yet

- Characterization of Liquid-Solid Reactions in Flow ChannelsDocument8 pagesCharacterization of Liquid-Solid Reactions in Flow ChannelsYuni_Arifwati_5495No ratings yet

- Beed III-lesson 1.1-The Curricula in School Sept 4 2021Document7 pagesBeed III-lesson 1.1-The Curricula in School Sept 4 2021catherine r. apusagaNo ratings yet

- Cover Letter and Thank You Letter ExamplesDocument7 pagesCover Letter and Thank You Letter Examplesf675ztsf100% (2)

- Primary Year 3 SJK SOWDocument150 pagesPrimary Year 3 SJK SOWJoshua100% (1)

- PBA Physics SSC-I FinalDocument7 pagesPBA Physics SSC-I Finalrayyanhashmi93No ratings yet

- Bahia Slave RevoltDocument73 pagesBahia Slave Revoltalexandercarberry1543No ratings yet

- 1st International Conference On Foreign Language Teaching and Applied Linguistics (Sarajevo, 5-7 May 2011)Document38 pages1st International Conference On Foreign Language Teaching and Applied Linguistics (Sarajevo, 5-7 May 2011)Jasmin Hodžić100% (2)

- Chapter 22 - Futures MarketsDocument9 pagesChapter 22 - Futures MarketsminibodNo ratings yet

- Understanding Adjuncts in GrammarDocument4 pagesUnderstanding Adjuncts in GrammarCarlos Lopez CifuentesNo ratings yet

- COR 014 Personal Development Day 2 Journaling (38Document24 pagesCOR 014 Personal Development Day 2 Journaling (38Camsy PandaNo ratings yet

- FORM B1 Photocopiables 3CDocument2 pagesFORM B1 Photocopiables 3CAnka SchoolNo ratings yet

- 11Document24 pages11anil.gelra5140100% (1)

- Patient ProfileDocument9 pagesPatient ProfileValarmathiNo ratings yet

- Status Signalling and Conspicuous Consumption: The Demand For Counterfeit Status GoodDocument5 pagesStatus Signalling and Conspicuous Consumption: The Demand For Counterfeit Status GoodMarliezel CaballeroNo ratings yet

- Medication Error ThesisDocument6 pagesMedication Error Thesisoaehviiig100% (2)

- Assessment 2 Stat20053 Descriptive Statistics - CompressDocument2 pagesAssessment 2 Stat20053 Descriptive Statistics - CompressDon RatbuNo ratings yet

- Religion ScriptDocument3 pagesReligion Scriptapi-461590822No ratings yet

- The Myth of Scientific Miracles in The KoranDocument13 pagesThe Myth of Scientific Miracles in The KoranDoctor Jones33% (3)

- Unit 5 Math-Parent Letter-4th GradeDocument4 pagesUnit 5 Math-Parent Letter-4th Gradeapi-346081420No ratings yet

- Hesi v2Document125 pagesHesi v2kandiezein88No ratings yet