You might also like

- Solution Manual For Managerial Accounting 7th Edition James Jiambalvo DownloadDocument25 pagesSolution Manual For Managerial Accounting 7th Edition James Jiambalvo DownloadGaryLeemtno100% (45)

- Final Exam - Ba 213Document6 pagesFinal Exam - Ba 213api-408647155100% (1)

- Charles AKMENDocument11 pagesCharles AKMENCharles GohNo ratings yet

- Sample D - Exam SolutionsDocument8 pagesSample D - Exam SolutionsJaden EuNo ratings yet

- Classic Pen Company Case: MBA 628: Managerial Accounting Instructor: Dr. Juan J. SegoviaDocument5 pagesClassic Pen Company Case: MBA 628: Managerial Accounting Instructor: Dr. Juan J. SegoviabharathtgNo ratings yet

- Question - Parallel Quiz - Final Term - Cost Accounting 22 - 23Document6 pagesQuestion - Parallel Quiz - Final Term - Cost Accounting 22 - 23Gistima Putra JavandaNo ratings yet

- HorngrenIMA14eSM ch13Document73 pagesHorngrenIMA14eSM ch13Piyal Hossain100% (1)

- Managerial Accounting - Classic Pen Company Case: GMITE7-Group 7Document21 pagesManagerial Accounting - Classic Pen Company Case: GMITE7-Group 7bharathtgNo ratings yet

- ABC MedTech ROIDocument27 pagesABC MedTech ROIWei ZhangNo ratings yet

- Week 8 (Unit 7) - Tutorial Solutions: Review QuestionDocument10 pagesWeek 8 (Unit 7) - Tutorial Solutions: Review QuestionSheenam SinghNo ratings yet

- Solution Manual For Accounting For Decision Making and Control 9th Edition Jerold ZimmermanDocument7 pagesSolution Manual For Accounting For Decision Making and Control 9th Edition Jerold Zimmermanfuze.riddle.ghik9100% (46)

- MSC Management & MSC Marketing & MSC International Business: Assessment 2-60%Document6 pagesMSC Management & MSC Marketing & MSC International Business: Assessment 2-60%Lu YangNo ratings yet

- F5 Asignment 1Document5 pagesF5 Asignment 1Minhaj AlbeezNo ratings yet

- Exercise 5-25 Activity Levels and Cost Drivers: RequiredDocument20 pagesExercise 5-25 Activity Levels and Cost Drivers: RequiredDilsa JainNo ratings yet

- Accounting & Control: Cost ManagementDocument22 pagesAccounting & Control: Cost ManagementdewyNo ratings yet

- Lecture 4 SolutionsDocument11 pagesLecture 4 SolutionsHiền NguyễnNo ratings yet

- Managerial Accounting 5th Edition Jiambalvo Solutions ManualDocument25 pagesManagerial Accounting 5th Edition Jiambalvo Solutions Manualnhattranel7k1100% (28)

- Course Exam ACCO 503 Managerial and Financial AccountingDocument20 pagesCourse Exam ACCO 503 Managerial and Financial Accountingmauricio ricardoNo ratings yet

- Solutions For CH 9 2-26-14Document15 pagesSolutions For CH 9 2-26-14Rafael Ricardo VilleroNo ratings yet

- Chapter 5Document9 pagesChapter 5Dishantely SamboNo ratings yet

- CH14 ABC systems 練習題Document3 pagesCH14 ABC systems 練習題sslbsNo ratings yet

- Exercise 8-26 Cost Classification: RequirementDocument153 pagesExercise 8-26 Cost Classification: RequirementIkram100% (1)

- Revision Module 5 PDFDocument5 pagesRevision Module 5 PDFavineshNo ratings yet

- Chapter 5 ABC - ABM PDFDocument31 pagesChapter 5 ABC - ABM PDFdiky supriadiNo ratings yet

- Final For PDFDocument8 pagesFinal For PDFWaizin KyawNo ratings yet

- Ch04Hansen6e ABCDocument21 pagesCh04Hansen6e ABCTini SholihaniNo ratings yet

- Soultions - Chapter 3Document8 pagesSoultions - Chapter 3Naudia L. TurnbullNo ratings yet

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Document22 pagesABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranNo ratings yet

- City Buildings Business PowerPoint TemplateDocument15 pagesCity Buildings Business PowerPoint TemplateSalman SajidNo ratings yet

- Ch.3Document23 pagesCh.3ahmedgalalabdalbaath2003No ratings yet

- Module 2 - ExercisesDocument6 pagesModule 2 - ExercisesaNo ratings yet

- Case Study: Study Processes and CostsDocument4 pagesCase Study: Study Processes and CostsCristiano Jr.No ratings yet

- Exam 2 ReviewDocument18 pagesExam 2 ReviewBrad MellerNo ratings yet

- University of Finance and MarketingDocument8 pagesUniversity of Finance and MarketingQuế Phương NguyễnNo ratings yet

- Cost Allocation and Activity-Based Costing: Financial and Managerial Accounting 8th Edition Warren Reeve FessDocument39 pagesCost Allocation and Activity-Based Costing: Financial and Managerial Accounting 8th Edition Warren Reeve FessRafif AjieNo ratings yet

- Color ScopeDocument12 pagesColor Scopeprincemech2004100% (1)

- ABC Exercise With SolutionDocument33 pagesABC Exercise With Solutionगौरव जैनNo ratings yet

- 7114afe WK5 (WS3) AnsDocument8 pages7114afe WK5 (WS3) AnsFrasat IqbalNo ratings yet

- Kerjakan 4-12 Dan 4 - 17: 1. "Plantwide"Document4 pagesKerjakan 4-12 Dan 4 - 17: 1. "Plantwide"natan. lieNo ratings yet

- FIDM 2019-20 - L3 CompleteDocument55 pagesFIDM 2019-20 - L3 CompleteAdam StożekNo ratings yet

- Kode QDocument11 pagesKode QatikaNo ratings yet

- Pma Test 1 2022Document6 pagesPma Test 1 2022Janielle LambertNo ratings yet

- Lecture 6 - ABC Costing RevisedDocument22 pagesLecture 6 - ABC Costing RevisedMJ jNo ratings yet

- Unit 6 Chapter 11Document5 pagesUnit 6 Chapter 11Kimberly A AlanizNo ratings yet

- Exercises Chapter07 PricingDocument11 pagesExercises Chapter07 PricingQuỳnh ChâuNo ratings yet

- ACCT3500 (Fall 20) Answers To Tutorial 3Document7 pagesACCT3500 (Fall 20) Answers To Tutorial 3Mohammad ShabirNo ratings yet

- AF201 REVISION PACKAGE s1, 2023 - StudentsDocument9 pagesAF201 REVISION PACKAGE s1, 2023 - StudentsMiss SlayerNo ratings yet

- Latihan Akt MGT Lanjutan - Ppak Untar Genap 21-22 HTDocument18 pagesLatihan Akt MGT Lanjutan - Ppak Untar Genap 21-22 HTCalvin HadikusumaNo ratings yet

- Management Accounting Information in The New Business EnvironmentDocument31 pagesManagement Accounting Information in The New Business EnvironmentGaluh Boga KuswaraNo ratings yet

- Managerial Accounting Homework 1.3Document5 pagesManagerial Accounting Homework 1.3OvidiaNo ratings yet

- ABC SystemDocument11 pagesABC SystemSyarifatuz Zuhriyah UmarNo ratings yet

- Bthma2e Ch04 SMDocument132 pagesBthma2e Ch04 SMAmanda BarkerNo ratings yet

- ManaktugasDocument7 pagesManaktugasNimas KartikaNo ratings yet

- Acct 260 CHAPTER 8Document25 pagesAcct 260 CHAPTER 8John Guy0% (1)

- Managerial Accounting 6th Edition Jiambalvo Solutions ManualDocument24 pagesManagerial Accounting 6th Edition Jiambalvo Solutions Manualgenevievetruong9ajpr100% (28)

- Clarito, Trisha Bacostmx - Hw7 - Part 2Document3 pagesClarito, Trisha Bacostmx - Hw7 - Part 2Clarito, Trisha Kareen F.No ratings yet

- ABC Costing Autumn 19Document15 pagesABC Costing Autumn 19Tory IslamNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Gen Banking LawDocument11 pagesGen Banking LawDaniel John Cañares LegaspiNo ratings yet

- Candidates For Internship Program For 1st Term AY 2015-2016Document1 pageCandidates For Internship Program For 1st Term AY 2015-2016Daniel John Cañares LegaspiNo ratings yet

- The Trans-Pacific Partnership (Trade of Goods)Document6 pagesThe Trans-Pacific Partnership (Trade of Goods)Daniel John Cañares LegaspiNo ratings yet

- Certificate of Recognition: Charrevie M. TingsonDocument2 pagesCertificate of Recognition: Charrevie M. TingsonDaniel John Cañares LegaspiNo ratings yet

- Scatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Document6 pagesScatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Daniel John Cañares LegaspiNo ratings yet

- Bank Secrecy LawDocument2 pagesBank Secrecy LawDaniel John Cañares LegaspiNo ratings yet

- BEHASCIDocument2 pagesBEHASCIDaniel John Cañares LegaspiNo ratings yet

- Chapter 5 Professional AudiDocument35 pagesChapter 5 Professional AudiDaniel John Cañares Legaspi100% (1)

- Chapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDocument12 pagesChapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDaniel John Cañares LegaspiNo ratings yet

- Monday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMDocument2 pagesMonday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMDaniel John Cañares LegaspiNo ratings yet

- SMCDocument12 pagesSMCDaniel John Cañares LegaspiNo ratings yet

- City University of PasayDocument2 pagesCity University of PasayDaniel John Cañares LegaspiNo ratings yet

- 23 Marcon, Louise Margarette 24 Millar, AllyssaDocument2 pages23 Marcon, Louise Margarette 24 Millar, AllyssaDaniel John Cañares LegaspiNo ratings yet

- Partnership ReviewerDocument21 pagesPartnership ReviewerDaniel John Cañares Legaspi100% (1)

- PhotoshootDocument1 pagePhotoshootDaniel John Cañares LegaspiNo ratings yet

- Federatio N Year: Prof. Osler T AquinoDocument2 pagesFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiNo ratings yet

- Del Mundo Q and ADocument2 pagesDel Mundo Q and ADaniel John Cañares LegaspiNo ratings yet

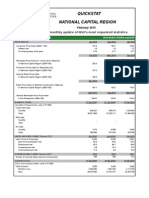

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 pagesQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiNo ratings yet

- Federatio N Year: Prof. Osler T AquinoDocument1 pageFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiNo ratings yet

- Sampoerna - Marketing Plan-Gc BonchonDocument13 pagesSampoerna - Marketing Plan-Gc BonchonDaniel John Cañares Legaspi50% (2)

- APS For Peer MentoringDocument2 pagesAPS For Peer MentoringDaniel John Cañares LegaspiNo ratings yet

- House Rules: 1. English Only PolicyDocument2 pagesHouse Rules: 1. English Only PolicyDaniel John Cañares LegaspiNo ratings yet

- Grand Academic Congress 2015 (Responses) - v7Document14 pagesGrand Academic Congress 2015 (Responses) - v7Daniel John Cañares LegaspiNo ratings yet

- Cost of Production Report First Department: Quantity ScheduleDocument4 pagesCost of Production Report First Department: Quantity ScheduleDaniel John Cañares LegaspiNo ratings yet