You might also like

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- Assignment 3 - Practice 3 CVP Analysis - Multi-ProductDocument2 pagesAssignment 3 - Practice 3 CVP Analysis - Multi-Productjoint accountNo ratings yet

- ABC-sample ProblemDocument5 pagesABC-sample ProblemLee Jap OyNo ratings yet

- Communication Plan September 27Document24 pagesCommunication Plan September 27Rosemarie T. BrionesNo ratings yet

- Activity Based CostingDocument50 pagesActivity Based CostingParamjit Sharma97% (65)

- Manacc Ans KeyDocument4 pagesManacc Ans KeyArchie Lazaro100% (1)

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Document22 pagesABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranNo ratings yet

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

- Activity Based CostingDocument13 pagesActivity Based CostingSudeep D'SouzaNo ratings yet

- Task-1 Market ResearchDocument2 pagesTask-1 Market ResearchDevyanshi HadaNo ratings yet

- Activity Based CostingDocument52 pagesActivity Based CostingraviktatiNo ratings yet

- Ch04 Activity Based CostingDocument52 pagesCh04 Activity Based CostingDaniel John Cañares LegaspiNo ratings yet

- Activity Based Costing - Case StudyDocument8 pagesActivity Based Costing - Case StudyViksit Choudhary100% (1)

- Optional: Service BulletinDocument8 pagesOptional: Service BulletinDaniil SerovNo ratings yet

- Supply Chain Management in Big BazaarDocument25 pagesSupply Chain Management in Big Bazaarabhijit05582% (11)

- Waterway Continuous Problem WCPDocument17 pagesWaterway Continuous Problem WCPAboi Boboi50% (4)

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- ABC Costing Autumn 19Document15 pagesABC Costing Autumn 19Tory IslamNo ratings yet

- Answers Homework # 15 Cost MGMT 4Document7 pagesAnswers Homework # 15 Cost MGMT 4Raman ANo ratings yet

- F5 Asignment 1Document5 pagesF5 Asignment 1Minhaj AlbeezNo ratings yet

- ABC COSTING PRESENTATIONDocument17 pagesABC COSTING PRESENTATIONSumit GargNo ratings yet

- Chapter 5. Activity Based CostingDocument28 pagesChapter 5. Activity Based CostingbellaNo ratings yet

- Chapter 2 Activity Based Costing: 1. ObjectivesDocument13 pagesChapter 2 Activity Based Costing: 1. ObjectivesNilda CorpuzNo ratings yet

- Lecture 6 - ABC Costing RevisedDocument22 pagesLecture 6 - ABC Costing RevisedMJ jNo ratings yet

- Quiz ABCDocument2 pagesQuiz ABCZoey Alvin EstarejaNo ratings yet

- Activity Based CostingDocument49 pagesActivity Based CostingEdson EdwardNo ratings yet

- Chapter 6 Cost Allocation and Activity-Based CostingDocument30 pagesChapter 6 Cost Allocation and Activity-Based CostingEjaz AhmadNo ratings yet

- 1.3 Activity Based Costing 1.3 Activity Based CostingDocument10 pages1.3 Activity Based Costing 1.3 Activity Based CostingSUHRIT BISWASNo ratings yet

- Chapter 10 Activity Based CostingDocument10 pagesChapter 10 Activity Based CostingRuby P. MadejaNo ratings yet

- Activity Based CostingDocument20 pagesActivity Based CostingArpit SahaiNo ratings yet

- AKUNTANSI MANAJEMEN ABC-ABMDocument54 pagesAKUNTANSI MANAJEMEN ABC-ABMAnonymous yMOMM9bsNo ratings yet

- Tahmina Ahmed Instructor Cost AccountingDocument19 pagesTahmina Ahmed Instructor Cost Accountingfaraazxbox1No ratings yet

- City Buildings Business PowerPoint TemplateDocument15 pagesCity Buildings Business PowerPoint TemplateSalman SajidNo ratings yet

- ABC & ABM: Activity-Based Costing and Management ExplainedDocument31 pagesABC & ABM: Activity-Based Costing and Management Explaineddiky supriadiNo ratings yet

- Group 6 PPT CaseDocument33 pagesGroup 6 PPT CaseRavNeet KaUr100% (1)

- Exercise 5-25 Activity Levels and Cost Drivers: RequiredDocument20 pagesExercise 5-25 Activity Levels and Cost Drivers: RequiredDilsa JainNo ratings yet

- Activity Based Costing: By: Kasahun N. (M.SC.)Document20 pagesActivity Based Costing: By: Kasahun N. (M.SC.)Mulugeta WoldeNo ratings yet

- Bco322 Budgeting and ControlDocument10 pagesBco322 Budgeting and ControlHà Biên Lê ĐặngNo ratings yet

- ABC SystemDocument11 pagesABC SystemSyarifatuz Zuhriyah UmarNo ratings yet

- Garrison 8 Ex 5-20, PR 5-25Document17 pagesGarrison 8 Ex 5-20, PR 5-25Shalini VeluNo ratings yet

- Activity-Based Costing: Mcgraw-Hill/IrwinDocument17 pagesActivity-Based Costing: Mcgraw-Hill/IrwinImran KhanNo ratings yet

- B01 AbcDocument21 pagesB01 AbcAcca BooksNo ratings yet

- Ch.2 - Job CostingDocument26 pagesCh.2 - Job Costingahmedgalalabdalbaath2003No ratings yet

- Absorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesDocument4 pagesAbsorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesAung Zaw HtweNo ratings yet

- Cost and Management Accounting 01 _ Class Notes (1)Document114 pagesCost and Management Accounting 01 _ Class Notes (1)saurabhNo ratings yet

- Revision New CostsingsDocument10 pagesRevision New CostsingsSammy Ben MenahemNo ratings yet

- ABC Method..Document20 pagesABC Method..Mutambu MwetaNo ratings yet

- MAHM6e Ch04.Ab - AzDocument49 pagesMAHM6e Ch04.Ab - Azlita2703No ratings yet

- ABC Costing Lecture1Document12 pagesABC Costing Lecture1Nusrat JahanNo ratings yet

- Activity Based Costing ER - NewDocument14 pagesActivity Based Costing ER - NewFadillah LubisNo ratings yet

- PPC Ch. 4Document20 pagesPPC Ch. 4Mulugeta WoldeNo ratings yet

- Measuring and Managing Process Performance: QuestionsDocument4 pagesMeasuring and Managing Process Performance: QuestionsAshik Uz ZamanNo ratings yet

- Measuring and Managing Process Performance: QuestionsDocument4 pagesMeasuring and Managing Process Performance: QuestionsAshik Uz ZamanNo ratings yet

- Lec4 ABCDocument31 pagesLec4 ABCnathan panNo ratings yet

- Answers Homework # 16 Cost MGMT 5Document7 pagesAnswers Homework # 16 Cost MGMT 5Raman ANo ratings yet

- ABC Costing Quiz ReviewDocument7 pagesABC Costing Quiz ReviewCody TarantinoNo ratings yet

- Managerial Accounting Final Exam SolutionsDocument10 pagesManagerial Accounting Final Exam SolutionsRanim HfaidhiaNo ratings yet

- 05 Handout 1Document6 pages05 Handout 1Reanne Mae BilogNo ratings yet

- Activity Based CostingDocument10 pagesActivity Based CostingEdi Kristanta PelawiNo ratings yet

- 602 Assignment 1Document8 pages602 Assignment 1Irina ShamaievaNo ratings yet

- ManaktugasDocument7 pagesManaktugasNimas KartikaNo ratings yet

- Lecture 2 Activity Based CostingDocument6 pagesLecture 2 Activity Based Costingmaharajabby81No ratings yet

- Activity Based CostingDocument3 pagesActivity Based Costingsumit kumarNo ratings yet

- ADA University, School of Business ACCT3500 Managerial Accounting, 2017 / 2018 Fall Semester Quiz 2 (10 Minutes)Document3 pagesADA University, School of Business ACCT3500 Managerial Accounting, 2017 / 2018 Fall Semester Quiz 2 (10 Minutes)Mohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 7 BudgetingDocument11 pagesACCT3500 (Fall 20) Lecture and Tutorial 7 BudgetingMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Answers To Tutorial 2Document6 pagesACCT3500 (Fall 20) Answers To Tutorial 2Mohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 1 Introductory LectureDocument3 pagesACCT3500 (Fall 20) Lecture and Tutorial 1 Introductory LectureMohammad ShabirNo ratings yet

- Managerial Accounting Tutorial AnswersDocument5 pagesManagerial Accounting Tutorial AnswersMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 7 BudgetingDocument11 pagesACCT3500 (Fall 20) Lecture and Tutorial 7 BudgetingMohammad ShabirNo ratings yet

- LaiACCT3500/Fall 20 (answers to tutorial 1Document2 pagesLaiACCT3500/Fall 20 (answers to tutorial 1Mohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 3 ABCDocument14 pagesACCT3500 (Fall 20) Lecture and Tutorial 3 ABCMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 4 CVPADocument13 pagesACCT3500 (Fall 20) Lecture and Tutorial 4 CVPAMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 5 Relevant CostsDocument9 pagesACCT3500 (Fall 20) Lecture and Tutorial 5 Relevant CostsMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 1 Introductory LectureDocument3 pagesACCT3500 (Fall 20) Lecture and Tutorial 1 Introductory LectureMohammad ShabirNo ratings yet

- ACCT3500 (Fall 20) Lecture and Tutorial 2 CostingDocument15 pagesACCT3500 (Fall 20) Lecture and Tutorial 2 CostingMohammad ShabirNo ratings yet

- Accounts PaperDocument2 pagesAccounts PaperRohan Ghadge-46No ratings yet

- Why The Rich Are Getting Richer by Robert T. Kiyosaki: Download HereDocument3 pagesWhy The Rich Are Getting Richer by Robert T. Kiyosaki: Download HereAndrew MichaelNo ratings yet

- Philips V NLRC PDFDocument7 pagesPhilips V NLRC PDFIoa WnnNo ratings yet

- Asset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutDocument10 pagesAsset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutcamirandamNo ratings yet

- Equity CrowdfundingDocument13 pagesEquity CrowdfundingantonyNo ratings yet

- MRB Approves Nonconforming PartsDocument3 pagesMRB Approves Nonconforming PartsMiguel RodriguezNo ratings yet

- Ir l04 U06 TestDocument5 pagesIr l04 U06 TestghostarixNo ratings yet

- Inside Flipkart A High-Pressure Workplace Thanks To IPO DreamsDocument1 pageInside Flipkart A High-Pressure Workplace Thanks To IPO DreamsRama Kant0% (1)

- Chapter 2. Historical and Current ThinkingDocument5 pagesChapter 2. Historical and Current Thinkingnguyetanhtata0207k495No ratings yet

- Jollisavers Meals TV Ad DeconstructedDocument4 pagesJollisavers Meals TV Ad DeconstructedMa. Rhona Faye MedesNo ratings yet

- K WaterDocument113 pagesK WaterAmri Rifki FauziNo ratings yet

- Education System Thesis StatementDocument6 pagesEducation System Thesis Statementanneryssanchezpaterson100% (2)

- TCPL Integrated Annual Report - FY2020-21Document288 pagesTCPL Integrated Annual Report - FY2020-21Mark LucasNo ratings yet

- Training in Human Resource ManagementDocument21 pagesTraining in Human Resource ManagementAlok kumarNo ratings yet

- Pelangi 2019 PDFDocument194 pagesPelangi 2019 PDFTharshanraaj RaajNo ratings yet

- List of Key Indian Office HoldersDocument15 pagesList of Key Indian Office HoldersRohit KumarNo ratings yet

- Jawad Internship ReportDocument28 pagesJawad Internship Reportjunaidyaseen442No ratings yet

- SAP NetWeaver WAS Administration TrainingDocument8 pagesSAP NetWeaver WAS Administration Trainingchaduvula1995No ratings yet

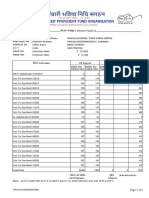

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Goodwill 23.3.23Document1 pageGoodwill 23.3.2308 Ajay Halder 11- CNo ratings yet

- SW One DXP Cost Sheet (4.5BHK+Utility) Phase 2Document1 pageSW One DXP Cost Sheet (4.5BHK+Utility) Phase 2assetcafe7No ratings yet

- Problem 9-21 (Pp. 420-421) : 1. Should The Owner Feel Frustrated With The Variance Reports? ExplainDocument3 pagesProblem 9-21 (Pp. 420-421) : 1. Should The Owner Feel Frustrated With The Variance Reports? ExplainCj SernaNo ratings yet

- RBI's Credit Monitoring Arrangement and Tandon Committee recommendationsDocument4 pagesRBI's Credit Monitoring Arrangement and Tandon Committee recommendationsAbhi_IMK100% (1)

- Visa Wizard - France-VisasDocument2 pagesVisa Wizard - France-VisasAbthal Tenore Al-fasnaNo ratings yet

- FSA Guide 20Document16 pagesFSA Guide 20David DangNo ratings yet