You might also like

- Revenue Regulations on Tax Compromise SettlementDocument11 pagesRevenue Regulations on Tax Compromise SettlementBobby Olavides SebastianNo ratings yet

- Taxation Review Income Taxation For Individual TaxpayersDocument8 pagesTaxation Review Income Taxation For Individual TaxpayersAsh AdoNo ratings yet

- TAX-1701 (Authority of The Commissioner of Internal Revenue)Document3 pagesTAX-1701 (Authority of The Commissioner of Internal Revenue)saligumba mikeNo ratings yet

- 2 Authority of The Commissioner of Internal Revenue 1Document13 pages2 Authority of The Commissioner of Internal Revenue 1Catherine AlzagaNo ratings yet

- 2 Authority of The Commissioner of Internal RevenueDocument12 pages2 Authority of The Commissioner of Internal RevenueAngel MarieNo ratings yet

- Tax Remedies and Assessment ProceduresDocument27 pagesTax Remedies and Assessment ProceduresNodlesde Awanab ZurcNo ratings yet

- Strategic Tax MNGT 2Document3 pagesStrategic Tax MNGT 2accpco.100No ratings yet

- REMEDIESDocument9 pagesREMEDIESkathlenejane.garciaNo ratings yet

- Tax-Remedies - Authority-of-CIR 2022Document4 pagesTax-Remedies - Authority-of-CIR 20229nh9xfrkqyNo ratings yet

- Taxation Law Reviewer Key ConceptsDocument13 pagesTaxation Law Reviewer Key ConceptsJericho PedragosaNo ratings yet

- Tax 2 Finals ReviewerDocument19 pagesTax 2 Finals Reviewerapi-3837022100% (2)

- Title VIII Tax Remedies NotesDocument7 pagesTitle VIII Tax Remedies NotesAnthony Yap100% (1)

- Rmo 22 01Document20 pagesRmo 22 01Maria Leonora Bornales100% (1)

- Uniform LayoutDocument7 pagesUniform LayoutJade CoritanaNo ratings yet

- CODAL - TAXATION - TITLE VIII RemediesDocument10 pagesCODAL - TAXATION - TITLE VIII RemediesTea AnnNo ratings yet

- Tax 1701 Cir PDFDocument22 pagesTax 1701 Cir PDFHeva AbsalonNo ratings yet

- Title Viii - RemediesDocument7 pagesTitle Viii - RemedieshrvyvyyyNo ratings yet

- Tax RemediesDocument10 pagesTax RemediesBryan CatungalNo ratings yet

- Revenue Regulations on Tax AssessmentDocument16 pagesRevenue Regulations on Tax AssessmentI.G. Mingo MulaNo ratings yet

- Income Taxation (Old Standard) RemediesDocument2 pagesIncome Taxation (Old Standard) RemediesKenneth CalzadoNo ratings yet

- RR 12-99Document16 pagesRR 12-99doraemoanNo ratings yet

- Revenue Memorandum Order No. 033-18Document9 pagesRevenue Memorandum Order No. 033-18TreshaNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document25 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Commissioner of Internal Revenue vs. Univation Motor Philippines, Inc. (Formerly Nissan Motor Philippines, Inc.), 901 SCRA 512, April 10, 2019Document18 pagesCommissioner of Internal Revenue vs. Univation Motor Philippines, Inc. (Formerly Nissan Motor Philippines, Inc.), 901 SCRA 512, April 10, 2019j0d3No ratings yet

- Taxation Law Reviewpower of Cir ReportDocument31 pagesTaxation Law Reviewpower of Cir ReportFiliusdeiNo ratings yet

- Concept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryDocument5 pagesConcept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryJD BarcellanoNo ratings yet

- Suspension of Running of Statute of Limitations. Sec. 223, NIRCDocument2 pagesSuspension of Running of Statute of Limitations. Sec. 223, NIRCshiejingNo ratings yet

- Tax - 4 - Module - 3 With AnswerDocument14 pagesTax - 4 - Module - 3 With AnswerDanielNo ratings yet

- BIR's powers and dutiesDocument19 pagesBIR's powers and dutiesjeff herradaNo ratings yet

- RR 12-99 Rules On Assessments PDFDocument19 pagesRR 12-99 Rules On Assessments PDFJeremeh PenarejoNo ratings yet

- RR No. 30-02Document1 pageRR No. 30-02Joanna MandapNo ratings yet

- A. Assessment B. Collection: Remedies of The GovernmentDocument10 pagesA. Assessment B. Collection: Remedies of The GovernmentGianna CantoriaNo ratings yet

- Tax Review Remedies of The GovernmentDocument120 pagesTax Review Remedies of The GovernmentJaline Aquino MozoNo ratings yet

- Tax Remedies of Government and Tax PayersDocument3 pagesTax Remedies of Government and Tax PayersHanah Grace DelfinNo ratings yet

- Tax Remedies and CompromiseDocument5 pagesTax Remedies and Compromiselegine ramaylaNo ratings yet

- Module 6 Tax Remedies ReviewerDocument11 pagesModule 6 Tax Remedies ReviewerburgerpattygirlNo ratings yet

- Tax2 Finals REMDocument16 pagesTax2 Finals REMAlexandra Castro-SamsonNo ratings yet

- Notes in Taxation IIDocument6 pagesNotes in Taxation IIJoe BuenoNo ratings yet

- Remedies Under NIRCDocument14 pagesRemedies Under NIRCcmv mendoza100% (3)

- Finals Personal Study Guide Tax2Document116 pagesFinals Personal Study Guide Tax2TeacherEliNo ratings yet

- TRAIN Law ProvisionsDocument5 pagesTRAIN Law ProvisionsCarmela WenceslaoNo ratings yet

- Remedies of The TaxpayerDocument4 pagesRemedies of The TaxpayerAngelyn Sanjorjo50% (2)

- RemediesDocument45 pagesRemediesCzarina100% (1)

- Bir RR 12-99Document21 pagesBir RR 12-99Isaac Joshua AganonNo ratings yet

- Title ViiiDocument8 pagesTitle ViiiErica Mae GuzmanNo ratings yet

- Rev. Regs. 12-99Document21 pagesRev. Regs. 12-99Phoebe SpaurekNo ratings yet

- Notes in Tax RemediesDocument104 pagesNotes in Tax RemediesJeremae Ann CeriacoNo ratings yet

- Tax REv NotesDocument23 pagesTax REv NotesCti Ahyeza DMNo ratings yet

- Ac 5288Document31 pagesAc 5288Choco KookieNo ratings yet

- Tax-Remedies (Govt-Remedies-Highlights)Document38 pagesTax-Remedies (Govt-Remedies-Highlights)Yves Nicollete LabadanNo ratings yet

- Taxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationDocument4 pagesTaxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationKristen StewartNo ratings yet

- Pale Cases 02232019Document3 pagesPale Cases 02232019DenardConwiBesaNo ratings yet

- Tax Collection Systems: Withholding Taxes Collected Under This SystemDocument9 pagesTax Collection Systems: Withholding Taxes Collected Under This Systememielyn lafortezaNo ratings yet

- RR 13-01Document5 pagesRR 13-01Peggy SalazarNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- RR No. 13-2018 CorrectedDocument20 pagesRR No. 13-2018 CorrectedRap BaguioNo ratings yet

- 53765-2003-Rule On Custody of Minors and Writ of HabeasDocument6 pages53765-2003-Rule On Custody of Minors and Writ of HabeasJennylyn Biltz AlbanoNo ratings yet

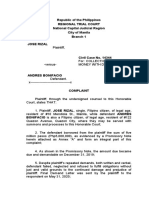

- Republic of The Philippines Regional Trial Court National Capital Judicial Region City of Manila Branch 1 Jose RizalDocument4 pagesRepublic of The Philippines Regional Trial Court National Capital Judicial Region City of Manila Branch 1 Jose RizalMilane Anne CunananNo ratings yet

- 3SCorpo CUNANAN Task1 RCCDocument22 pages3SCorpo CUNANAN Task1 RCCMilane Anne CunananNo ratings yet

- 213485-2018-Republic v. SerenoDocument261 pages213485-2018-Republic v. SerenoKristina B DiamanteNo ratings yet

- ARDC vs Ago Dispute Over Corporate Property ImprovementsDocument19 pagesARDC vs Ago Dispute Over Corporate Property ImprovementsMilane Anne CunananNo ratings yet

- Petitioner vs. vs. Respondent: Third DivisionDocument8 pagesPetitioner vs. vs. Respondent: Third DivisionMilane Anne CunananNo ratings yet

- Stonehill vs. Diokno - Right To Rss Is: (Ppop)Document11 pagesStonehill vs. Diokno - Right To Rss Is: (Ppop)Milane Anne CunananNo ratings yet

- Edu vs. GomezDocument3 pagesEdu vs. GomezShiela PilarNo ratings yet

- 203942-2016-Taina Manigque-Stone v. Cattleya Land Inc.Document13 pages203942-2016-Taina Manigque-Stone v. Cattleya Land Inc.ACNo ratings yet

- Court upholds validity of mortgage on disputed propertyDocument3 pagesCourt upholds validity of mortgage on disputed propertyShiela PilarNo ratings yet

- Petitioners vs. vs. Respondents: Second DivisionDocument14 pagesPetitioners vs. vs. Respondents: Second DivisionMilane Anne CunananNo ratings yet

- A Hidden and Unknown Deposit of Money Is Considered A HiddenDocument2 pagesA Hidden and Unknown Deposit of Money Is Considered A HiddenMilane Anne CunananNo ratings yet

- TAX 1 DIGESTS - LimitationsDocument12 pagesTAX 1 DIGESTS - LimitationsMilane Anne Cunanan100% (1)

- Petitioner vs. vs. Respondents Araneta, Mendoza & Papa Martin B. LaureaDocument6 pagesPetitioner vs. vs. Respondents Araneta, Mendoza & Papa Martin B. LaureaMilane Anne CunananNo ratings yet

- Case Doctrines SummaryDocument3 pagesCase Doctrines SummaryMilane Anne CunananNo ratings yet

- 132215-1989-Moles v. Intermediate Appellate CourtDocument9 pages132215-1989-Moles v. Intermediate Appellate CourtJ castNo ratings yet

- Plaintiffs-Appellants Vs Vs Defendants-Appellees Almacen & Almacen Diosdado GaringalaoDocument4 pagesPlaintiffs-Appellants Vs Vs Defendants-Appellees Almacen & Almacen Diosdado GaringalaoMilane Anne CunananNo ratings yet

- Rev. 2.11. 135056-1985-Escaler - v. - Court - of - Appeals PDFDocument6 pagesRev. 2.11. 135056-1985-Escaler - v. - Court - of - Appeals PDFMilane Anne CunananNo ratings yet

- Plaintiffs-Appellees vs. vs. Defendant-Appellant Villareal, Almacen, Navarra & Associates Sycip, Salazar, Luna, Manalo & FelicianoDocument6 pagesPlaintiffs-Appellees vs. vs. Defendant-Appellant Villareal, Almacen, Navarra & Associates Sycip, Salazar, Luna, Manalo & FelicianoMilane Anne CunananNo ratings yet

- Borbon v. Servicewide PDFDocument7 pagesBorbon v. Servicewide PDFAnonymous mxCPJJPVEfNo ratings yet

- Petitioner vs. vs. Respondents Pantaleon Z. Salcedo Leandro B. FernandezDocument7 pagesPetitioner vs. vs. Respondents Pantaleon Z. Salcedo Leandro B. FernandezJanna SalvacionNo ratings yet

- 6 Fedman - Development - Corp. - v. - Agcaoili20180911-5466-Yu715wDocument8 pages6 Fedman - Development - Corp. - v. - Agcaoili20180911-5466-Yu715wMark De JesusNo ratings yet

- Court upholds land sale despite unpaid balanceDocument9 pagesCourt upholds land sale despite unpaid balanceAisa CastilloNo ratings yet

- 1.-153136-1939-Levy Hermanos Inc. v. GervacioDocument3 pages1.-153136-1939-Levy Hermanos Inc. v. GervacioJanna SalvacionNo ratings yet

- Bachrach Motor Co. Inc. v. MillanDocument4 pagesBachrach Motor Co. Inc. v. MillanVia Rhidda ImperialNo ratings yet

- 117633-2000-Laforteza v. Machuca PDFDocument12 pages117633-2000-Laforteza v. Machuca PDFNichole Patricia PedriñaNo ratings yet

- 203942-2016-Taina Manigque-Stone v. Cattleya Land Inc.Document13 pages203942-2016-Taina Manigque-Stone v. Cattleya Land Inc.ACNo ratings yet

- r.1. 121287-2004-Arra - Realty - Corp. - v. - Guarantee - Development20180412-1159-Onax2u PDFDocument20 pagesr.1. 121287-2004-Arra - Realty - Corp. - v. - Guarantee - Development20180412-1159-Onax2u PDFMilane Anne CunananNo ratings yet

- Hbupm1741l Q1 2023-24Document2 pagesHbupm1741l Q1 2023-24ProlayNo ratings yet

- Tax Rates Card 2023 GC - 220819 - 230837Document5 pagesTax Rates Card 2023 GC - 220819 - 230837smnomanNo ratings yet

- Borrower ChecklistDocument2 pagesBorrower ChecklistquibroNo ratings yet

- Contractor's Ledger 1Document4 pagesContractor's Ledger 1Fareha RiazNo ratings yet

- 183553-2012-Diageo Philippines, Inc. v. Commissioner of Internal RevenueDocument7 pages183553-2012-Diageo Philippines, Inc. v. Commissioner of Internal RevenueButch MaatNo ratings yet

- Swiftcom Screen Report Deut BniDocument1 pageSwiftcom Screen Report Deut BniBagus AndriansyahNo ratings yet

- 3 6bitcoinDocument1 page3 6bitcoinjohn.whiteNo ratings yet

- Istilah Pajak Dalam Bahasa InggrisDocument2 pagesIstilah Pajak Dalam Bahasa Inggrisroida hasugianNo ratings yet

- TRAIN Law (PWC Philippines) PDFDocument16 pagesTRAIN Law (PWC Philippines) PDFYzar VelascoNo ratings yet

- Classification of Taxes: A. Domestic CorporationDocument5 pagesClassification of Taxes: A. Domestic CorporationWenjunNo ratings yet

- HSBC Amanah Malaysia Berhad ("HSBC Amanah") Universal Terms & ConditionsDocument41 pagesHSBC Amanah Malaysia Berhad ("HSBC Amanah") Universal Terms & ConditionsfaridajirNo ratings yet

- Standard Format SBLC Incoming (Final) - CorrectionDocument1 pageStandard Format SBLC Incoming (Final) - Correctionfugga50% (2)

- 5338 - September 2021 - P33MK3ZQEFJQM1AFODHYA3BR5477351240762656333113912Document1 page5338 - September 2021 - P33MK3ZQEFJQM1AFODHYA3BR5477351240762656333113912Shreyash SahayNo ratings yet

- Source Docuemnts For UploadingDocument26 pagesSource Docuemnts For UploadingCarlene Mae Ugay100% (1)

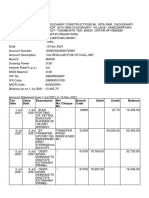

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument12 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancevijay choudharyNo ratings yet

- Tax InvoiceDocument2 pagesTax InvoiceNoman AnsariNo ratings yet

- Tax Audit Requirements for Intraday Equity and F&O Trading IncomeDocument5 pagesTax Audit Requirements for Intraday Equity and F&O Trading IncomebalakrishnaNo ratings yet

- Dav Public School,: Bseb Colony, PatnaDocument5 pagesDav Public School,: Bseb Colony, PatnaSaumya SaumyaNo ratings yet

- Rhombus Energy, Inc. vs. Commissioner of Internal Revenue DigestDocument2 pagesRhombus Energy, Inc. vs. Commissioner of Internal Revenue DigestEmir MendozaNo ratings yet

- Individual Taxpayer 1atax2Document21 pagesIndividual Taxpayer 1atax2Joneric RamosNo ratings yet

- Contract Guernsey Tax Summary To PDFDocument1 pageContract Guernsey Tax Summary To PDFMancus MariusNo ratings yet

- GST Amendments For June 22 Students by CA Vivek GabaDocument6 pagesGST Amendments For June 22 Students by CA Vivek GabayashNo ratings yet

- Prepaid CreditDocument8 pagesPrepaid CreditJavier RojasNo ratings yet

- Compute Income TaxDocument24 pagesCompute Income TaxMelody Fabreag76% (25)

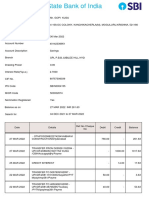

- Account Statement-Unlocked PDFDocument12 pagesAccount Statement-Unlocked PDFvamsiNo ratings yet

- Wmcustomer 17586699 E73 CustomerInvoice PDFDocument1 pageWmcustomer 17586699 E73 CustomerInvoice PDFmdazajalamNo ratings yet

- Managing Transaction Taxesfor BrazilDocument31 pagesManaging Transaction Taxesfor BrazilLuiz A M V BarraNo ratings yet

- Report IBPMECMCXXXX760BBP - SB 0169-1Document5 pagesReport IBPMECMCXXXX760BBP - SB 0169-1MuhammadAsimNo ratings yet

- 25 Dollar 1Up Account Signup and Payment StepsDocument12 pages25 Dollar 1Up Account Signup and Payment StepsDeepak YadavNo ratings yet

- SBI Simply Click Jan22-1Document1 pageSBI Simply Click Jan22-1Broke BondNo ratings yet