You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Month Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Document209 pagesMonth Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Ivan ChiuNo ratings yet

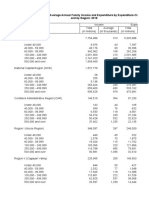

- Table 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Document16 pagesTable 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Ivan ChiuNo ratings yet

- ABA - Annual Report 2019Document169 pagesABA - Annual Report 2019Ivan ChiuNo ratings yet

- ABA - Annual Report 2017Document128 pagesABA - Annual Report 2017Ivan ChiuNo ratings yet

- ABA - Annual Report 2018Document146 pagesABA - Annual Report 2018Ivan ChiuNo ratings yet

- Table 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Document8 pagesTable 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Glenn GalvezNo ratings yet

- Table 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Document8 pagesTable 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Ivan ChiuNo ratings yet

- 7 - BibliographyDocument4 pages7 - BibliographyIvan ChiuNo ratings yet

- Table 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Document2 pagesTable 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Ivan ChiuNo ratings yet

- Table 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Document10 pagesTable 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Ivan ChiuNo ratings yet

- 6 - Summary, Conclusion and RecommendationDocument3 pages6 - Summary, Conclusion and RecommendationIvan ChiuNo ratings yet

- 3 - Conceptual FrameworkDocument3 pages3 - Conceptual FrameworkIvan ChiuNo ratings yet

- 4 - MethodologyDocument6 pages4 - MethodologyIvan ChiuNo ratings yet

- Bscs Se v2011 PDFDocument3 pagesBscs Se v2011 PDFBobNo ratings yet

- Bachelor of Science in Computer ScienceDocument3 pagesBachelor of Science in Computer ScienceIvan ChiuNo ratings yet

- CIMA ScenarioDocument10 pagesCIMA ScenarioPerfectionism FollowerNo ratings yet

- Accounting For Branches and Combined FSDocument112 pagesAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuNo ratings yet

- The Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentDocument9 pagesThe Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentIvan ChiuNo ratings yet

- Auditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaDocument1 pageAuditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaRJ Diana0% (1)

- Briefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power andDocument4 pagesBriefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power andIvan ChiuNo ratings yet

- CSC 121Document8 pagesCSC 121Ivan ChiuNo ratings yet

- Salosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestDocument1 pageSalosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestIvan ChiuNo ratings yet

- 47.taxability of Productivity Incentive Bonuses.07.10.08.GACDocument2 pages47.taxability of Productivity Incentive Bonuses.07.10.08.GACEumell Alexis PaleNo ratings yet

- Audit Internal ExternalDocument1 pageAudit Internal ExternalIvan ChiuNo ratings yet

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuNo ratings yet

- Power of The MassesDocument1 pagePower of The MassesIvan ChiuNo ratings yet

- Critique of Comtemporary Philippine FilmsDocument1 pageCritique of Comtemporary Philippine FilmsIvan ChiuNo ratings yet

- It's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanDocument1 pageIt's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanIvan ChiuNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Divine Mercy ShrineDocument3 pagesDivine Mercy ShrineGwynne WabeNo ratings yet

- Yoo In-Soo - AsianWikiDocument1 pageYoo In-Soo - AsianWikiLerkheJhane ToribioNo ratings yet

- Baru PDFDocument4 pagesBaru PDFshribarathiNo ratings yet

- Zoom G2.1u English ManualDocument25 pagesZoom G2.1u English ManualKevin KerberNo ratings yet

- Bus Comm AssignDocument9 pagesBus Comm AssignKarenNo ratings yet

- ASTM D1816 - 12 (2019) Standard Test Method For Dielectric Breakdown Voltage of Insulating Liquids Using VDE ElectrodesDocument5 pagesASTM D1816 - 12 (2019) Standard Test Method For Dielectric Breakdown Voltage of Insulating Liquids Using VDE ElectrodesAlonso Lioneth100% (2)

- PubCorp BookExcerpts 01Document6 pagesPubCorp BookExcerpts 01Roms RoldanNo ratings yet

- Latch Lock and Mutex Contention TroubleshootingDocument20 pagesLatch Lock and Mutex Contention Troubleshootingvippy_love100% (1)

- Sample Final PDFDocument3 pagesSample Final PDFshallypallyNo ratings yet

- The Imamis Between Rationalism and TraditionalismDocument12 pagesThe Imamis Between Rationalism and Traditionalismmontazerm100% (1)

- Dekada 70 and The Patriot: A Film Analysis ofDocument3 pagesDekada 70 and The Patriot: A Film Analysis ofCHARLIES CutiesNo ratings yet

- Science Year 3/grade 8: Middle Years ProgrammeDocument4 pagesScience Year 3/grade 8: Middle Years Programmeakshyta gantanNo ratings yet

- Our Cover Is Definitely The Reason Why We Would Choose This Book in A BookstoreDocument1 pageOur Cover Is Definitely The Reason Why We Would Choose This Book in A BookstoreSlobaKuzmanovicNo ratings yet

- What Is The Use of Accord Powder?Document3 pagesWhat Is The Use of Accord Powder?ivy l.sta.mariaNo ratings yet

- Emerging Treatment Options For Prostate CancerDocument8 pagesEmerging Treatment Options For Prostate CancerMax Carrasco SanchezNo ratings yet

- Chapter 43 The Immune SystemDocument13 pagesChapter 43 The Immune System蔡旻珊No ratings yet

- Discipline of Counseling: Full Name: Grade 12 - HumssDocument7 pagesDiscipline of Counseling: Full Name: Grade 12 - HumssJhen DE ChavezNo ratings yet

- Semantics-Ms. Minh TamDocument15 pagesSemantics-Ms. Minh TamMy Tran100% (2)

- 哈佛大学开放课程 幸福课 (积极心理学) 视频英文字幕下载 (1-12集) (网易公开课提供) PDFDocument352 pages哈佛大学开放课程 幸福课 (积极心理学) 视频英文字幕下载 (1-12集) (网易公开课提供) PDFZiwei MiaoNo ratings yet

- Analysis and Interpretation of Assessment ResultsDocument84 pagesAnalysis and Interpretation of Assessment ResultsAlyanna Clarisse Padilla CamposNo ratings yet

- People v. Panlilio, G.R. Nos. 113519-20 Case Digest (Criminal Procedure)Document4 pagesPeople v. Panlilio, G.R. Nos. 113519-20 Case Digest (Criminal Procedure)AizaFerrerEbina50% (2)

- BS EN 12596 - Dynamic Viscosity by Vacuum CapillaryDocument22 pagesBS EN 12596 - Dynamic Viscosity by Vacuum CapillaryCraig LongNo ratings yet

- (1787) Crochet Succulent Crochet Tutorial Video For Beginners#handmade #Diy #Crochet #Crochettutorial - YouTubeDocument1 page(1787) Crochet Succulent Crochet Tutorial Video For Beginners#handmade #Diy #Crochet #Crochettutorial - YouTubevix.jumawanNo ratings yet

- What Muslim Invaders Really Did To IndiaDocument4 pagesWhat Muslim Invaders Really Did To IndiaTarek Fatah75% (16)

- Para MidtermsDocument126 pagesPara Midtermshezekiah hezNo ratings yet

- Demystifying Graph Data Science Graph Algorithms, Analytics Methods, Platforms, Databases, and Use Cases (Pethuru Raj, Abhishek Kumar Etc.) (Z-Library)Document415 pagesDemystifying Graph Data Science Graph Algorithms, Analytics Methods, Platforms, Databases, and Use Cases (Pethuru Raj, Abhishek Kumar Etc.) (Z-Library)edm kdNo ratings yet

- Design and Development of Alternative Delivery SystemDocument3 pagesDesign and Development of Alternative Delivery Systemfredie unggayNo ratings yet

- Dhruv ExplanationDocument3 pagesDhruv ExplanationDharmavir SinghNo ratings yet

- Comparative Study of CNC Controllers Used in CNC Milling MachineDocument9 pagesComparative Study of CNC Controllers Used in CNC Milling MachineAJER JOURNALNo ratings yet

- Quiz 1 - Semana 1 - PDFDocument6 pagesQuiz 1 - Semana 1 - PDFLeonardo AlzateNo ratings yet