You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Commercial Invoice: Reset FormDocument3 pagesCommercial Invoice: Reset FormBen AliNo ratings yet

- Module 1 8operations ManagementDocument84 pagesModule 1 8operations ManagementBryan Lord BatonNo ratings yet

- Objectives and Phases of Operational AuditsDocument12 pagesObjectives and Phases of Operational AuditsJacqueline Ortega100% (2)

- (The Oily Press Lipid Library) Frank Gunstone - Lipids For Functional Foods and Nutraceuticals-Woodhead Publishing (2003) PDFDocument341 pages(The Oily Press Lipid Library) Frank Gunstone - Lipids For Functional Foods and Nutraceuticals-Woodhead Publishing (2003) PDFCamilo Andrés CastroNo ratings yet

- 1 s2.0 S1473309921007039 MainDocument6 pages1 s2.0 S1473309921007039 MainCamilo Andrés CastroNo ratings yet

- Biomedicine & Pharmacotherapy: SciencedirectDocument10 pagesBiomedicine & Pharmacotherapy: SciencedirectCamilo Andrés CastroNo ratings yet

- Similar COVID-19 Incidence To The General Population in People With Opioid Use Disorder Receiving Integrated Outpatient Clinical CareDocument21 pagesSimilar COVID-19 Incidence To The General Population in People With Opioid Use Disorder Receiving Integrated Outpatient Clinical CareCamilo Andrés CastroNo ratings yet

- Value ChainDocument2 pagesValue ChainAbhishek Agarwal0% (1)

- Position Title: Enumerator (Only For Kunduz Residents)Document4 pagesPosition Title: Enumerator (Only For Kunduz Residents)Laiq BahirNo ratings yet

- Frasier Case Study: Search Over 500,000 Essays..Document9 pagesFrasier Case Study: Search Over 500,000 Essays..aishwarya sahaiNo ratings yet

- CMA Past Paper 2022Document17 pagesCMA Past Paper 2022Iqramunir IqramunirNo ratings yet

- Global Supply Chain Management: The Fresh Connection Simulation ReportDocument5 pagesGlobal Supply Chain Management: The Fresh Connection Simulation ReportnishantNo ratings yet

- WCA Certificate of Insurance and List of Employees 21-11-2022Document4 pagesWCA Certificate of Insurance and List of Employees 21-11-2022ArslanSaeedNo ratings yet

- Strategic Management : Gregory G. Dess and G. T. LumpkinDocument16 pagesStrategic Management : Gregory G. Dess and G. T. LumpkinJose driguezNo ratings yet

- Operations Management Managing Global Supply Chains 1st Edition Venkataraman Test BankDocument36 pagesOperations Management Managing Global Supply Chains 1st Edition Venkataraman Test BankmariowoodtncfjqbrowNo ratings yet

- Silabus AI 1Document7 pagesSilabus AI 1Aisyah Nadiatul HikmahNo ratings yet

- List of Reports Required YEAR 2020: Annex "A"Document12 pagesList of Reports Required YEAR 2020: Annex "A"Earl PatrickNo ratings yet

- Sindhiya Plastic IndustriesDocument12 pagesSindhiya Plastic IndustriesRaj KumarNo ratings yet

- Assurance ICAEW CFAB Question Bank 2021Document178 pagesAssurance ICAEW CFAB Question Bank 2021Huyền TrangNo ratings yet

- Activity Guide and Evaluation Rubric - Stage 2 - Intellectual PropertyDocument12 pagesActivity Guide and Evaluation Rubric - Stage 2 - Intellectual Propertyjc lozanoNo ratings yet

- MARICO Ltd. - Financial ModelDocument12 pagesMARICO Ltd. - Financial Modelmundadaharsh1No ratings yet

- A Premise of Union BankDocument18 pagesA Premise of Union BankMeheady HasanNo ratings yet

- Session 03 - 04 Entr6122Document30 pagesSession 03 - 04 Entr6122Jessy IskandarNo ratings yet

- Related Titles: Search DocumentDocument90 pagesRelated Titles: Search DocumentNikhil SinghNo ratings yet

- PINg Doce - ANASER Alimentação Fast FoodDocument13 pagesPINg Doce - ANASER Alimentação Fast Foodcaetano nunesNo ratings yet

- Nestle Pure LifeDocument44 pagesNestle Pure LifeJawad Aziz Farhad100% (1)

- A New Multi Objective Stochastic Model For A Forward Reve - 2013 - Applied Mathe PDFDocument17 pagesA New Multi Objective Stochastic Model For A Forward Reve - 2013 - Applied Mathe PDFRamakrushna MishraNo ratings yet

- Tulsiram PatelDocument130 pagesTulsiram PatelAnimesh RajoriyaNo ratings yet

- Kursus Kesedaran Keselamatan: Jabatan Pembangunan Kemahiran SarawakDocument51 pagesKursus Kesedaran Keselamatan: Jabatan Pembangunan Kemahiran SarawakLydia Mohammad SarkawiNo ratings yet

- Week 2 AIS 306 Activity Prelim GONZALESDocument5 pagesWeek 2 AIS 306 Activity Prelim GONZALEShelen rose cepedaNo ratings yet

- Week 11 Business Model MetrixDocument21 pagesWeek 11 Business Model Metrix20190101137 HafizNo ratings yet

- BTMS 2043 - Lecture 8Document20 pagesBTMS 2043 - Lecture 8Soh HerryNo ratings yet

- Abstract - World Class Maintenance (WCM) Concept IsDocument5 pagesAbstract - World Class Maintenance (WCM) Concept IsEduardo MonteiroNo ratings yet

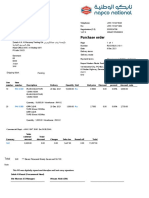

- Purchase Order: Napco Modern Plastic Products Co. - Sack DivisionDocument1 pagePurchase Order: Napco Modern Plastic Products Co. - Sack Divisionمحمد اصدNo ratings yet