You might also like

- CFD Forex Broker Report - 7th EditionDocument75 pagesCFD Forex Broker Report - 7th EditiongghghgfhfghNo ratings yet

- Mou Maggie ProspectusDocument17 pagesMou Maggie ProspectusMaggie MouNo ratings yet

- FX Trading: A Guide to Trading Foreign ExchangeFrom EverandFX Trading: A Guide to Trading Foreign ExchangeRating: 5 out of 5 stars5/5 (1)

- MPS - Budget TemplateDocument4 pagesMPS - Budget TemplateADETUNJI ADENIYI SAMUELNo ratings yet

- Chapter 6Document3 pagesChapter 6DanaosNo ratings yet

- International Financial Management PPT Chap 1Document26 pagesInternational Financial Management PPT Chap 1serge folegweNo ratings yet

- Running Head: International Trade 1Document6 pagesRunning Head: International Trade 1Bruce OderaNo ratings yet

- Solnik Chapter 3 Solutions To Questions & Problems (6th Edition)Document6 pagesSolnik Chapter 3 Solutions To Questions & Problems (6th Edition)gilli1trNo ratings yet

- International Trade Is Exchange ofDocument4 pagesInternational Trade Is Exchange ofshaequeazamNo ratings yet

- SPCFLCF36B29BDocument5 pagesSPCFLCF36B29BRao TvaraNo ratings yet

- Unintended Consequences: by John MauldinDocument11 pagesUnintended Consequences: by John Mauldinrichardck61No ratings yet

- Macro Economics Assignment 1Document13 pagesMacro Economics Assignment 1Naveen KumarNo ratings yet

- IFMDocument11 pagesIFMAqib RazaNo ratings yet

- Wpiea2020126 Print PDFDocument38 pagesWpiea2020126 Print PDFPrabudh MishraNo ratings yet

- High Inflation Rate: Inflation Begins With Money Losing ValueDocument4 pagesHigh Inflation Rate: Inflation Begins With Money Losing ValueWilliam ZenNo ratings yet

- The Foreign Exchange MarketDocument51 pagesThe Foreign Exchange Markethussien_economyNo ratings yet

- 2 Australia: Peter MccrayDocument27 pages2 Australia: Peter MccrayowltbigNo ratings yet

- Mohamad Hafiz Bin Ahmad RadziDocument9 pagesMohamad Hafiz Bin Ahmad RadziMohd HafizNo ratings yet

- Global Economy ModuleDocument6 pagesGlobal Economy ModuleMavianne T. TerrenalNo ratings yet

- Ôn tập lý thuyếtDocument4 pagesÔn tập lý thuyếtLinh NguyễnNo ratings yet

- IE Lecture 1Document58 pagesIE Lecture 1EnjoyNo ratings yet

- Work860 PDFDocument61 pagesWork860 PDFGeetika KhandelwalNo ratings yet

- Chapter 7: Government Intervention in International BusinessDocument6 pagesChapter 7: Government Intervention in International BusinessHans DizonNo ratings yet

- Introduction To Foreign ExchangeDocument80 pagesIntroduction To Foreign ExchangeGlobalStrategyNo ratings yet

- WK 11 SupplementDocument10 pagesWK 11 SupplementShou Yee WongNo ratings yet

- Int Business GlobalizationDocument27 pagesInt Business GlobalizationZohaib Jamil WahajNo ratings yet

- Term Project in Eb IIIDocument21 pagesTerm Project in Eb IIIdivvyankguptaNo ratings yet

- Yogesh SharmaDocument8 pagesYogesh SharmaAbhishek Gaming YTNo ratings yet

- Intro To International TradeDocument46 pagesIntro To International TradeKatherine SauerNo ratings yet

- International Trade and Natural ResourcesDocument35 pagesInternational Trade and Natural ResourcesTimur LukinNo ratings yet

- Current FTSE GM Issue Section1Document132 pagesCurrent FTSE GM Issue Section1pleumNo ratings yet

- International Trade 2 - Week 3Document15 pagesInternational Trade 2 - Week 3Ahmad Dwi Syaiful AmriIB102No ratings yet

- International Economics: Lecture 1. Introduction. World Trade: An OverviewDocument35 pagesInternational Economics: Lecture 1. Introduction. World Trade: An Overviewnishi_gautam_1No ratings yet

- UNIT 5 READING - Docx KO KEYDocument5 pagesUNIT 5 READING - Docx KO KEYthuyyhangg1003No ratings yet

- Full Download International Economics 15th Edition Pugel Solutions ManualDocument35 pagesFull Download International Economics 15th Edition Pugel Solutions Manualyakarzhehaot100% (36)

- Dwnload Full International Economics 15th Edition Pugel Solutions Manual PDFDocument35 pagesDwnload Full International Economics 15th Edition Pugel Solutions Manual PDFtenjeichabac9100% (9)

- International Economics 15th Edition Pugel Solutions ManualDocument8 pagesInternational Economics 15th Edition Pugel Solutions Manualrebeccapetersonrefkwxgbij100% (16)

- European Business Assignment 1Document5 pagesEuropean Business Assignment 1Serwaa AkotoNo ratings yet

- Assignment 3 ECON 401Document4 pagesAssignment 3 ECON 401aleena asifNo ratings yet

- World Trade OrganizationDocument7 pagesWorld Trade OrganizationWillyanto LeeNo ratings yet

- Case StudyDocument3 pagesCase StudyKogi JeyaNo ratings yet

- Thesis Topic Exchange RateDocument4 pagesThesis Topic Exchange RateAaron Anyaakuu100% (2)

- International Trade 1Document18 pagesInternational Trade 1kittysingla40988No ratings yet

- China Exchange Rate - NewDocument34 pagesChina Exchange Rate - NewPhu MiNo ratings yet

- Global Imbalances and Global Governance: Philip R. LaneDocument34 pagesGlobal Imbalances and Global Governance: Philip R. LanepalestallarNo ratings yet

- Run Lola Run The Good The Bad and The Ugly of FX Market Fragmentation Speech by Andrew HauserDocument14 pagesRun Lola Run The Good The Bad and The Ugly of FX Market Fragmentation Speech by Andrew HauserHao WangNo ratings yet

- Globalization and Its Effects To The WorldDocument9 pagesGlobalization and Its Effects To The WorldDumindu KatuwalaNo ratings yet

- The Balance of PaymentsDocument39 pagesThe Balance of PaymentsKiran AishaNo ratings yet

- Ge 3 Module 3Document7 pagesGe 3 Module 3eugene taleNo ratings yet

- Ireland in The Global Economy MCQsDocument13 pagesIreland in The Global Economy MCQsVicki LanganNo ratings yet

- Full Download International Economics 11th Edition Salvatore Solutions ManualDocument35 pagesFull Download International Economics 11th Edition Salvatore Solutions Manualyakarzhehaot100% (29)

- Dwnload Full Introduction To International Economics 3rd Edition Salvatore Solutions Manual PDFDocument35 pagesDwnload Full Introduction To International Economics 3rd Edition Salvatore Solutions Manual PDFstrewmerils1ej3n100% (12)

- FIM AssignmentDocument5 pagesFIM AssignmentNoor AliNo ratings yet

- The Structures of GlobalizationDocument4 pagesThe Structures of GlobalizationGerald Jaboyanon MondragonNo ratings yet

- Cross-Border M&a Activity and Financial DeepeningDocument23 pagesCross-Border M&a Activity and Financial Deepeninganimesh karnNo ratings yet

- Literature Review On International Trade and Economic GrowthDocument7 pagesLiterature Review On International Trade and Economic GrowthafmzsbnbobbgkeNo ratings yet

- Three Challenges For The New EU Trade CommissionerDocument5 pagesThree Challenges For The New EU Trade CommissionerWilliam WulffNo ratings yet

- Term Paper Import Export (International Trade) Procedure Still An Impediment To The Growth of Foreign TradeDocument27 pagesTerm Paper Import Export (International Trade) Procedure Still An Impediment To The Growth of Foreign TradeAsad Gour100% (1)

- C1 - Consequences of EMUDocument5 pagesC1 - Consequences of EMUTrái Chanh Ngọt Lịm Thích Ăn ChuaNo ratings yet

- The Reform of Europe: A Political Guide to the FutureFrom EverandThe Reform of Europe: A Political Guide to the FutureRating: 2 out of 5 stars2/5 (1)

- EIB Investment Report 2017/2018: From recovery to sustainable growthFrom EverandEIB Investment Report 2017/2018: From recovery to sustainable growthNo ratings yet

- Qe As An Economic Policy Tool What Does It Do and How Should We Use It Speech by Dave RamsdenDocument17 pagesQe As An Economic Policy Tool What Does It Do and How Should We Use It Speech by Dave RamsdenHao WangNo ratings yet

- Inflation A Tiger by The Tail Speech by Andy HaldaneDocument24 pagesInflation A Tiger by The Tail Speech by Andy HaldaneHao WangNo ratings yet

- Remarks On Challenges To The Economic Outlook Speech by Jonathan HaskelDocument12 pagesRemarks On Challenges To The Economic Outlook Speech by Jonathan HaskelHao WangNo ratings yet

- Jonathan Haskel Remarks On Challenges To The Economic Outlook SlidesDocument6 pagesJonathan Haskel Remarks On Challenges To The Economic Outlook SlidesHao WangNo ratings yet

- Dave Ramsden Institute of Chartered Accountants in England WalesDocument9 pagesDave Ramsden Institute of Chartered Accountants in England WalesHao WangNo ratings yet

- Andrew Haldane SpeechDocument32 pagesAndrew Haldane SpeechhansNo ratings yet

- Whats Going On Speech by Dave RamsdenDocument18 pagesWhats Going On Speech by Dave RamsdenHao WangNo ratings yet

- Transforming Our Payments Infrastructure Speech by Victoria ClelandDocument7 pagesTransforming Our Payments Infrastructure Speech by Victoria ClelandHao WangNo ratings yet

- Stock Take of Global Cyber Security Regulatory Initiatives Speech by Lyndon NelsonDocument12 pagesStock Take of Global Cyber Security Regulatory Initiatives Speech by Lyndon NelsonHao WangNo ratings yet

- Resilience and Continuity in An Interconnected and Changing World Speech by Lyndon NelsonDocument8 pagesResilience and Continuity in An Interconnected and Changing World Speech by Lyndon NelsonHao WangNo ratings yet

- From Construction To Maintenance Patrolling The Ring Fence Speech by James ProudmanDocument8 pagesFrom Construction To Maintenance Patrolling The Ring Fence Speech by James ProudmanHao WangNo ratings yet

- Why The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserDocument9 pagesWhy The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserHao WangNo ratings yet

- Some Effects of Demographic Change On The UK EconomyDocument22 pagesSome Effects of Demographic Change On The UK EconomyHao WangNo ratings yet

- From Construction To Maintenance Patrolling The Ring Fence Speech by James ProudmanDocument8 pagesFrom Construction To Maintenance Patrolling The Ring Fence Speech by James ProudmanHao WangNo ratings yet

- Why The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserDocument9 pagesWhy The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserHao WangNo ratings yet

- Positive Externalities Speech by Martin TaylorDocument9 pagesPositive Externalities Speech by Martin TaylorHao WangNo ratings yet

- Stock Take of Global Cyber Security Regulatory Initiatives Speech by Lyndon NelsonDocument12 pagesStock Take of Global Cyber Security Regulatory Initiatives Speech by Lyndon NelsonHao WangNo ratings yet

- The Economic Outlook Speech by Gertjan VliegheDocument20 pagesThe Economic Outlook Speech by Gertjan VliegheHao WangNo ratings yet

- Transforming Our Payments Infrastructure Speech by Victoria ClelandDocument7 pagesTransforming Our Payments Infrastructure Speech by Victoria ClelandHao WangNo ratings yet

- The Global Outlook Speech by Mark CarneyDocument20 pagesThe Global Outlook Speech by Mark CarneyHao WangNo ratings yet

- Setting Standards: Remarks Given by Dave Ramsden, Deputy Governor For Markets and BankingDocument6 pagesSetting Standards: Remarks Given by Dave Ramsden, Deputy Governor For Markets and BankingHao WangNo ratings yet

- The Creative Economy: Speech Given byDocument22 pagesThe Creative Economy: Speech Given byHao WangNo ratings yet

- Central Bank Independence As A Prerequisite For Financial Stability Speech by Richard SharpDocument11 pagesCentral Bank Independence As A Prerequisite For Financial Stability Speech by Richard SharpHao WangNo ratings yet

- Debt Dynamics: Speech Given by Ben BroadbentDocument20 pagesDebt Dynamics: Speech Given by Ben BroadbentHao WangNo ratings yet

- The Elusive Supply Potential: Monetary Policy in Times of UncertaintyDocument21 pagesThe Elusive Supply Potential: Monetary Policy in Times of UncertaintyHao WangNo ratings yet

- Will Uk Investment Bounce Back Speech by Jonathan HaskelDocument22 pagesWill Uk Investment Bounce Back Speech by Jonathan HaskelHao WangNo ratings yet

- A Platform For Innovation: Speech Given by Mark Carney, Governor Bank of EnglandDocument7 pagesA Platform For Innovation: Speech Given by Mark Carney, Governor Bank of EnglandHao WangNo ratings yet

- Investing in Ethnicity and Race Speech by Mark CarneyDocument7 pagesInvesting in Ethnicity and Race Speech by Mark CarneyHao WangNo ratings yet

- A New Horizon Speech by Mark CarneyDocument12 pagesA New Horizon Speech by Mark Carneyokovacs11okovacsNo ratings yet

- My Reflections On The Fpcs Strategy Speech by Anil KashyapDocument15 pagesMy Reflections On The Fpcs Strategy Speech by Anil KashyapHao WangNo ratings yet

- Chapter 02Document11 pagesChapter 02Saad mubeenNo ratings yet

- Accounting Quizbowl QuestionsDocument7 pagesAccounting Quizbowl QuestionsChabby ChabbyNo ratings yet

- Lembar Jawaban 2-BUKU BESARDocument13 pagesLembar Jawaban 2-BUKU BESAREnrico Jovian S SNo ratings yet

- Learning Objectives: Assets Liabilities + EquityDocument13 pagesLearning Objectives: Assets Liabilities + EquityAira AbigailNo ratings yet

- Engineering EconomyDocument19 pagesEngineering EconomyGreg Calibo LidasanNo ratings yet

- Ratio Analysis at Amararaja Batteries Limited (Arbl) A Project ReportDocument79 pagesRatio Analysis at Amararaja Batteries Limited (Arbl) A Project Reportfahim zamanNo ratings yet

- Exchange Control in IndiaDocument3 pagesExchange Control in Indianeemz1990100% (5)

- Brealey - Principles of Corporate Finance - 13e - Chap09 - SMDocument10 pagesBrealey - Principles of Corporate Finance - 13e - Chap09 - SMShivamNo ratings yet

- Mis 442Document9 pagesMis 442mirfaiyazkabir2000No ratings yet

- Pending Home SalesDocument2 pagesPending Home SalesAmber TaufenNo ratings yet

- Manufacturing Account Worked Example Question 8Document7 pagesManufacturing Account Worked Example Question 8Roshan RamkhalawonNo ratings yet

- AmazonFile 0Document2 pagesAmazonFile 0chawllarohitNo ratings yet

- Errata Group Statements Vol 2 17th Ed Reprint 2021Document10 pagesErrata Group Statements Vol 2 17th Ed Reprint 2021THABO CLARENCE MohleleNo ratings yet

- Starting A Silk Screen Printing Business PDFDocument2 pagesStarting A Silk Screen Printing Business PDFMarietta Fragata RamiterreNo ratings yet

- Chapter 11 - Part 1 - Accounting FranchisesDocument13 pagesChapter 11 - Part 1 - Accounting FranchisesJane Dizon100% (1)

- Negen Angel Fund FAQsDocument8 pagesNegen Angel Fund FAQsAnil Kumar Reddy ChinthaNo ratings yet

- 21127, Ahmad, Assignment 5, IFDocument5 pages21127, Ahmad, Assignment 5, IFmuhammad ahmadNo ratings yet

- Sawsan Hassan Al SaffarDocument3 pagesSawsan Hassan Al SaffarwaminoNo ratings yet

- Prop Firm Drawdown Limitations - Forex Prop ReviewsDocument9 pagesProp Firm Drawdown Limitations - Forex Prop ReviewsMye RakNo ratings yet

- Foreign Exchange Rate Sheet: Bulletin November 29, 2021Document1 pageForeign Exchange Rate Sheet: Bulletin November 29, 2021Zeeshan AtharNo ratings yet

- Partnership Dissolution: National College of Business and ArtsDocument5 pagesPartnership Dissolution: National College of Business and ArtsKate Jezel SantoniaNo ratings yet

- SP PaperDocument11 pagesSP Paper9137373282abcdNo ratings yet

- Ministry of Revenues: Tax Audit ManualDocument304 pagesMinistry of Revenues: Tax Audit ManualYoNo ratings yet

- I2BE-Morning Evening PDFDocument10 pagesI2BE-Morning Evening PDFusama sajawalNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruTed Mosby100% (1)

- Assignment On International TradeDocument3 pagesAssignment On International TradeMark James GarzonNo ratings yet

- Pioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesDocument4 pagesPioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesPrajwal PaiNo ratings yet

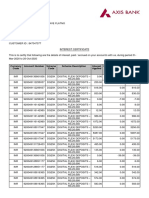

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet