You might also like

- Model Answer: E-Commerce store launch by Unilever in Sri LankaFrom EverandModel Answer: E-Commerce store launch by Unilever in Sri LankaNo ratings yet

- 10 SectorsDocument28 pages10 SectorsanshikaNo ratings yet

- The BCG Growth-Share Matrix: Theory and Applications: The key to portfolio managementFrom EverandThe BCG Growth-Share Matrix: Theory and Applications: The key to portfolio managementRating: 2 out of 5 stars2/5 (1)

- PC - HLL Co Visit - Dec 2014 FINAL 20141224150219 PDFDocument9 pagesPC - HLL Co Visit - Dec 2014 FINAL 20141224150219 PDFAniket DhanukaNo ratings yet

- Hindustan Unilever: CMP: INR1,604Document10 pagesHindustan Unilever: CMP: INR1,604Vishakha RathodNo ratings yet

- 10 Sectors 8 AugustDocument28 pages10 Sectors 8 AugustanshikaNo ratings yet

- Final Report - FM Project - HUL 2020Document4 pagesFinal Report - FM Project - HUL 2020Barathy ArvindNo ratings yet

- IDBI Capital FMCG Sector UpdateDocument177 pagesIDBI Capital FMCG Sector UpdateHimani SinghalNo ratings yet

- Annapurna Ayush Axe Breeze Bru Brooke Bond Clinic Dove Fair & LovelyDocument4 pagesAnnapurna Ayush Axe Breeze Bru Brooke Bond Clinic Dove Fair & LovelyAnu IlakiyaNo ratings yet

- Fom Assignment MaDocument14 pagesFom Assignment MaadarshNo ratings yet

- JOCIL LTD - Initiating Coverage - Sept 10 - 16 Sep 2010Document13 pagesJOCIL LTD - Initiating Coverage - Sept 10 - 16 Sep 2010Amber GuptaNo ratings yet

- Hindustan Unilever: CMP: INR858 Aborted Kraft-Heinz Attempt For UnileverDocument8 pagesHindustan Unilever: CMP: INR858 Aborted Kraft-Heinz Attempt For UnileverChinmayJoshiNo ratings yet

- Hindustan Unilever LimitedDocument8 pagesHindustan Unilever LimitedsonalimanchandaNo ratings yet

- Comparison Itc and HulDocument1 pageComparison Itc and HulAshish SinglaNo ratings yet

- HUL's Net Sales Rise by 7% in First Quarter - The Economic TimesDocument1 pageHUL's Net Sales Rise by 7% in First Quarter - The Economic TimesTanisha AgarwalNo ratings yet

- Resilient Q1 Performance Amid Challenges: Hindustan Unilever LTDDocument8 pagesResilient Q1 Performance Amid Challenges: Hindustan Unilever LTDUTSAVNo ratings yet

- Ratio Analysis of Top FMGC Companies in India and Their ComparisionDocument26 pagesRatio Analysis of Top FMGC Companies in India and Their ComparisionSUMIT KUMAR SINGHNo ratings yet

- FM J Component Review 1Document20 pagesFM J Component Review 1J S SupreethaNo ratings yet

- Marketing PlanDocument59 pagesMarketing PlanSharath Shyamasunder75% (4)

- Financial Analysis of Hul and GodrejDocument53 pagesFinancial Analysis of Hul and GodrejJiwan Jot SinghNo ratings yet

- 05 - Amrita AroraDocument9 pages05 - Amrita AroraAmrita AroraNo ratings yet

- MM Project C7Document4 pagesMM Project C7Mayukh MukhopadhyayNo ratings yet

- Accounts ProjectDocument38 pagesAccounts ProjectLaksh SinghalNo ratings yet

- Entrepreneurship Final Presentation OutlineDocument13 pagesEntrepreneurship Final Presentation Outlineapi-525820170No ratings yet

- Competitive Strategy ..HulDocument7 pagesCompetitive Strategy ..HulPallavi Vaid50% (2)

- DGM14 - D42010019 - Hitesh ParasharDocument10 pagesDGM14 - D42010019 - Hitesh ParasharHitesh ParasharNo ratings yet

- Thomson Reuters Stock Report - Hindustan Unilever LTD PDFDocument11 pagesThomson Reuters Stock Report - Hindustan Unilever LTD PDFShriyaDarganNo ratings yet

- Motilal Oswal Thematic View On Consumer Time To Restock!Document72 pagesMotilal Oswal Thematic View On Consumer Time To Restock!Rahul GargNo ratings yet

- Pidilite Industries: Robust Recovery Margin Pressure AheadDocument15 pagesPidilite Industries: Robust Recovery Margin Pressure AheadIS group 7No ratings yet

- Competitive Strategies Followed by FMCG Sector in IndiaDocument4 pagesCompetitive Strategies Followed by FMCG Sector in IndiaPrashant Gurjar100% (1)

- Portfolio Analysis - Personal Care - Group 2 - Section C PDFDocument25 pagesPortfolio Analysis - Personal Care - Group 2 - Section C PDFroguemba100% (1)

- Competitive Strategies Followed by FMCG Sector in India: Free Trial: Project MGMT Accenture CareersDocument9 pagesCompetitive Strategies Followed by FMCG Sector in India: Free Trial: Project MGMT Accenture Careersabhik_123No ratings yet

- EADRDocument42 pagesEADRvivekbade2013No ratings yet

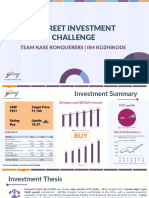

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- Piramal Enterprises: Building Scalable Differentiated Pharma BusinessDocument14 pagesPiramal Enterprises: Building Scalable Differentiated Pharma BusinessEcho WackoNo ratings yet

- Swedish Installation Artist, Michael Johansson, Created The Godrej Heart Art Wall by Juxtaposing Different Products From Across Our BusinessesDocument68 pagesSwedish Installation Artist, Michael Johansson, Created The Godrej Heart Art Wall by Juxtaposing Different Products From Across Our BusinessesSubrat RathNo ratings yet

- Annual Report 2015-16 JK FennerDocument68 pagesAnnual Report 2015-16 JK FennerMohan RajNo ratings yet

- Corporate Finance - Risk and ValuationDocument6 pagesCorporate Finance - Risk and ValuationATUL KUMARNo ratings yet

- FMCG, Rating Methodology, Feb 2022Document17 pagesFMCG, Rating Methodology, Feb 2022jayNo ratings yet

- Hul Vs Itc StrategyDocument15 pagesHul Vs Itc StrategySharanya Srinivasa100% (2)

- Hindustan Unilever Limited: A Project Report OnDocument32 pagesHindustan Unilever Limited: A Project Report OnNupur VarmaNo ratings yet

- Merger of Hul and GSK CH India Hul Presentation Tcm1255 529065 1 enDocument18 pagesMerger of Hul and GSK CH India Hul Presentation Tcm1255 529065 1 ensheetal0% (1)

- Hul Dove ReportDocument23 pagesHul Dove ReportYasavNo ratings yet

- Financial Statement Analysis Report On Hindustan Unilever Limited, Dabur and MaricoDocument50 pagesFinancial Statement Analysis Report On Hindustan Unilever Limited, Dabur and MaricoJKIONo ratings yet

- Hindustan Unilever: Better Performance in An Uncertain EnvironmentDocument7 pagesHindustan Unilever: Better Performance in An Uncertain EnvironmentUTSAVNo ratings yet

- Rural MarketingDocument17 pagesRural Marketing2123 Sushmita PalNo ratings yet

- Student Name: Sharath Shyamasunder Course: M.B.A. Uob Number: 09034024 Batch Number: MBBD 51010A Subject: Marketing Word Count: Less Than 3500 WordsDocument60 pagesStudent Name: Sharath Shyamasunder Course: M.B.A. Uob Number: 09034024 Batch Number: MBBD 51010A Subject: Marketing Word Count: Less Than 3500 WordsHeena ParveenNo ratings yet

- Financial Statement Analysis ReportDocument49 pagesFinancial Statement Analysis ReportSandeep King Swain100% (1)

- Mini ProjectDocument23 pagesMini ProjectSumit BeraNo ratings yet

- LSM Investigation Report Sample 1Document36 pagesLSM Investigation Report Sample 1Ranjana BandaraNo ratings yet

- Aarti Industries LTD August-10: Industry: Chemicals Recommendation: BUYDocument6 pagesAarti Industries LTD August-10: Industry: Chemicals Recommendation: BUYMishra Anand PrakashNo ratings yet

- IBM AssignmentDocument6 pagesIBM AssignmenttarunNo ratings yet

- HUL Equity Research ReportDocument20 pagesHUL Equity Research Reportrohitatwork357No ratings yet

- ( (Group 6 - (Sie1011) )Document29 pages( (Group 6 - (Sie1011) )Rohit KarmakerNo ratings yet

- Capital StructureDocument65 pagesCapital Structureselvamsettus0% (1)

- Case 1 Managing Hindustan Unilever StrategicallyDocument7 pagesCase 1 Managing Hindustan Unilever StrategicallyYash Agarwal100% (3)

- Final ProjectDocument24 pagesFinal ProjectShreya targeNo ratings yet

- ComparisonsDocument4 pagesComparisonsnupurbagrilNo ratings yet

- Hul ProDocument23 pagesHul ProNitika GuptaNo ratings yet

- Final ITC Vs HULDocument15 pagesFinal ITC Vs HULAnindya MukherjeeNo ratings yet

- Fund Managers HandbookDocument72 pagesFund Managers HandbookAlp DhingraNo ratings yet

- Fund Managers HandbookDocument72 pagesFund Managers HandbookAlp DhingraNo ratings yet

- ICICI Bank Annual Report FY2015Document236 pagesICICI Bank Annual Report FY2015gauravNo ratings yet

- Understanding Stock Index FuturesDocument21 pagesUnderstanding Stock Index FuturesAlp DhingraNo ratings yet

- Collaborating For GrowthDocument98 pagesCollaborating For GrowthAkhilesh JainNo ratings yet

- RF Summary Practical Guide Risk ManagementDocument9 pagesRF Summary Practical Guide Risk ManagementAlp DhingraNo ratings yet

- Market Profile-Futures TradingDocument6 pagesMarket Profile-Futures TradingAlp Dhingra100% (2)

- Chapter 2 - Insurance RiskDocument22 pagesChapter 2 - Insurance RiskY XyNo ratings yet

- BadhravathiDocument82 pagesBadhravathitvasanthoshNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument10 pagesUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNo ratings yet

- Acca F7Document73 pagesAcca F7taoyuan521100% (2)

- Astor Lodge & Suites, Inc CASEDocument16 pagesAstor Lodge & Suites, Inc CASETatianna GroveNo ratings yet

- D6Document11 pagesD6neo14No ratings yet

- US Internal Revenue Service: p1525Document603 pagesUS Internal Revenue Service: p1525IRSNo ratings yet

- Project Report at KelDocument76 pagesProject Report at KelAsif HashimNo ratings yet

- Service Tax Refund - RansaDocument1 pageService Tax Refund - RansaservervcnewNo ratings yet

- The Effect of Financial Secrecy and IFRS Adoption On Earnings Quality: A Comparative Study Between Indonesia, Malaysia and SingaporeDocument24 pagesThe Effect of Financial Secrecy and IFRS Adoption On Earnings Quality: A Comparative Study Between Indonesia, Malaysia and SingaporeMarwiyahNo ratings yet

- 2030 Roadmap: Australian Agriculture's Plan For A $100 Billion IndustryDocument48 pages2030 Roadmap: Australian Agriculture's Plan For A $100 Billion IndustryToby VueNo ratings yet

- Pa Bab 13 DividendsDocument3 pagesPa Bab 13 DividendsRahmi RestuNo ratings yet

- Advanced Financial Accounting 10th Edition Christensen Solutions ManualDocument25 pagesAdvanced Financial Accounting 10th Edition Christensen Solutions ManualHerbertRangelqrtc100% (56)

- Chapter 12Document15 pagesChapter 12Cooper89No ratings yet

- Case Study Creating Monster in The OfficeDocument2 pagesCase Study Creating Monster in The OfficechienNo ratings yet

- Acctg7 Prob4Document3 pagesAcctg7 Prob4Nyster Ann RebenitoNo ratings yet

- Acct 122 Outline (New)Document8 pagesAcct 122 Outline (New)Onika BlandinNo ratings yet

- 2013 Pan European Private Equity Performance Benchmarks Study Evca Thomson Reuters Final VersionDocument28 pages2013 Pan European Private Equity Performance Benchmarks Study Evca Thomson Reuters Final VersionAbdullah HassanNo ratings yet

- Fundamentals of Corporate Finance, 2nd Edition, Selt Test Ch03Document7 pagesFundamentals of Corporate Finance, 2nd Edition, Selt Test Ch03macseuNo ratings yet

- Britannia Industries Ltd. (India) : SourceDocument6 pagesBritannia Industries Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Management Accounting: A Business Partner: Lecture # 1Document15 pagesManagement Accounting: A Business Partner: Lecture # 1Amna NasserNo ratings yet

- Project On Chocolate Industry in Lotte India Corporation Ltd1Document51 pagesProject On Chocolate Industry in Lotte India Corporation Ltd1Keleti Santhosh100% (1)

- Intermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesDocument7 pagesIntermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesdeeznutsNo ratings yet

- Pas 12: Accounting For Income TaxDocument2 pagesPas 12: Accounting For Income TaxKiana FernandezNo ratings yet

- 0807 - Ec 1Document23 pages0807 - Ec 1haryhunter50% (2)

- 2050spring15 SyllabusDocument7 pages2050spring15 SyllabusJimNo ratings yet

- Job Order CostingDocument32 pagesJob Order CostingSetia NurulNo ratings yet

- Sensus Healthcare, Inc. (SRTS) Q1 2023 Earnings Call Transcript - Seeking AlphaDocument28 pagesSensus Healthcare, Inc. (SRTS) Q1 2023 Earnings Call Transcript - Seeking Alpha123456789No ratings yet

- Ldce - Fasp - 08 PDFDocument9 pagesLdce - Fasp - 08 PDFDinesh Talele86% (7)

- I 1040Document161 pagesI 1040ricola1982No ratings yet

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaFrom EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaRating: 4.5 out of 5 stars4.5/5 (266)

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessFrom EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessRating: 5 out of 5 stars5/5 (456)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesFrom EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesRating: 5 out of 5 stars5/5 (1635)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessFrom EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNo ratings yet

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsFrom EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsRating: 4.5 out of 5 stars4.5/5 (383)

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindFrom EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindRating: 4.5 out of 5 stars4.5/5 (57)

- Summary of 12 Rules for Life: An Antidote to ChaosFrom EverandSummary of 12 Rules for Life: An Antidote to ChaosRating: 4.5 out of 5 stars4.5/5 (294)

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsFrom EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsRating: 4.5 out of 5 stars4.5/5 (709)

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesFrom EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesRating: 4.5 out of 5 stars4.5/5 (273)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryFrom EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryRating: 5 out of 5 stars5/5 (556)

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessFrom EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessRating: 4.5 out of 5 stars4.5/5 (328)

- Summary of Atomic Habits by James ClearFrom EverandSummary of Atomic Habits by James ClearRating: 5 out of 5 stars5/5 (169)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsFrom EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsNo ratings yet

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningFrom EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningRating: 4.5 out of 5 stars4.5/5 (55)

- Summary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityFrom EverandSummary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityNo ratings yet

- Tiny Habits by BJ Fogg - Book Summary: The Small Changes That Change EverythingFrom EverandTiny Habits by BJ Fogg - Book Summary: The Small Changes That Change EverythingRating: 4.5 out of 5 stars4.5/5 (111)

- How Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseFrom EverandHow Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseRating: 4.5 out of 5 stars4.5/5 (83)

- Designing Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeFrom EverandDesigning Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeRating: 4.5 out of 5 stars4.5/5 (62)

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeFrom EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeRating: 4.5 out of 5 stars4.5/5 (128)

- Summary, Analysis, and Review of Daniel Kahneman's Thinking, Fast and SlowFrom EverandSummary, Analysis, and Review of Daniel Kahneman's Thinking, Fast and SlowRating: 3.5 out of 5 stars3.5/5 (2)

- Summary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutFrom EverandSummary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutRating: 1 out of 5 stars1/5 (1)

- We Were the Lucky Ones: by Georgia Hunter | Conversation StartersFrom EverandWe Were the Lucky Ones: by Georgia Hunter | Conversation StartersNo ratings yet

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageFrom EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageRating: 4.5 out of 5 stars4.5/5 (329)

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessFrom EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessRating: 4.5 out of 5 stars4.5/5 (187)

- SUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)From EverandSUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)Rating: 4.5 out of 5 stars4.5/5 (14)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingFrom EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingRating: 4.5 out of 5 stars4.5/5 (114)

- Book Summary of The Subtle Art of Not Giving a F*ck by Mark MansonFrom EverandBook Summary of The Subtle Art of Not Giving a F*ck by Mark MansonRating: 4.5 out of 5 stars4.5/5 (577)

- Psycho-Cybernetics by Maxwell Maltz - Book SummaryFrom EverandPsycho-Cybernetics by Maxwell Maltz - Book SummaryRating: 4.5 out of 5 stars4.5/5 (91)