You might also like

- Industry Analysis of Telecom Sector1Document34 pagesIndustry Analysis of Telecom Sector1Animesh100% (1)

- Portars Diamond Model On TelecomeDocument10 pagesPortars Diamond Model On Telecomeshaikhmohib93No ratings yet

- Indian Tele ContextDocument31 pagesIndian Tele ContextSadhna MishraNo ratings yet

- Abhishek Raj Beck - Capstone 3Document36 pagesAbhishek Raj Beck - Capstone 3Abhishek raj beck (PGDM 17-19)No ratings yet

- Impact of External Environment On Telecom IndustryDocument25 pagesImpact of External Environment On Telecom Industrykanabaramit100% (9)

- India's Growing IT Industry Powers Economic GrowthDocument3 pagesIndia's Growing IT Industry Powers Economic GrowthhaNo ratings yet

- Indian Telecom IndustryDocument6 pagesIndian Telecom IndustryananndNo ratings yet

- Cellular Technologies for Emerging Markets: 2G, 3G and BeyondFrom EverandCellular Technologies for Emerging Markets: 2G, 3G and BeyondNo ratings yet

- Abstract (2).DocxDocument36 pagesAbstract (2).Docxarked kediaNo ratings yet

- Sales Promotion Study of Seabirds GroupDocument59 pagesSales Promotion Study of Seabirds GrouprammalsamNo ratings yet

- RHRS Main ProfileDocument43 pagesRHRS Main ProfileLingesh Sai KumarNo ratings yet

- Panaroma - ICT - 2014Document4 pagesPanaroma - ICT - 2014Shubham AroraNo ratings yet

- The Changing Indian Telecommunication IndustryDocument11 pagesThe Changing Indian Telecommunication Industryashish9dubey-16No ratings yet

- Information Technology in IndiaDocument10 pagesInformation Technology in IndiaNAVEEL ISLAMNo ratings yet

- Telecom: Industry Awareness ReportDocument23 pagesTelecom: Industry Awareness ReportBhagya ShreeNo ratings yet

- Ey Speeding Ahead On The Telecom and Digital Economy Highway 2Document116 pagesEy Speeding Ahead On The Telecom and Digital Economy Highway 2avijeetboparaiNo ratings yet

- 008-Niral Dalal-India Telecom SectorDocument91 pages008-Niral Dalal-India Telecom SectorDipesh JainNo ratings yet

- 07 - Chapter 1Document21 pages07 - Chapter 1Ankita PrabhulkarNo ratings yet

- India Telecom SectorDocument92 pagesIndia Telecom SectorKaif ShaikhNo ratings yet

- Micro - Economics (I-Mba Sem-Iv) Module - IvDocument4 pagesMicro - Economics (I-Mba Sem-Iv) Module - IvSabhaya ChiragNo ratings yet

- LPG drives globalization of Indian businessDocument5 pagesLPG drives globalization of Indian businessNikita Patwardhan100% (1)

- Introduction - EvolutionDocument9 pagesIntroduction - EvolutionSuresh KumarNo ratings yet

- The Changing Indian Telecommunication IndustryDocument11 pagesThe Changing Indian Telecommunication IndustryHarsh MehtaNo ratings yet

- Managerial Economics Assignment 2Document10 pagesManagerial Economics Assignment 2GEETHU MANOJNo ratings yet

- Emerging Telecom Industry ReportDocument40 pagesEmerging Telecom Industry Reportasif ansariNo ratings yet

- Indian Telecom Sector Growth in 2010Document4 pagesIndian Telecom Sector Growth in 2010ash21_foryouNo ratings yet

- Executive Summary: Indian Tele-CommunicationsDocument50 pagesExecutive Summary: Indian Tele-CommunicationsAsim OlakfNo ratings yet

- Final DraftDocument49 pagesFinal Draftmridulthebest882No ratings yet

- Dokumen - Tips - Training Report On BSNLDocument41 pagesDokumen - Tips - Training Report On BSNLAashish sharmaNo ratings yet

- Project ReportDocument12 pagesProject ReportRohit SharmaNo ratings yet

- Information Technology in India: The Shift in Paradigm: Shiri AhujaDocument12 pagesInformation Technology in India: The Shift in Paradigm: Shiri AhujaKishore ReddyNo ratings yet

- Employee TurnoverDocument52 pagesEmployee TurnovershivaniNo ratings yet

- Damodaram Sanjivayya National Law University, Ap, India: SubjectDocument16 pagesDamodaram Sanjivayya National Law University, Ap, India: SubjectPradeep reddy JonnalaNo ratings yet

- Unit IvDocument9 pagesUnit Ivkomalkatre11No ratings yet

- Research ReportDocument81 pagesResearch ReportMirali MonparaNo ratings yet

- National Telecom Policy - 2012Document20 pagesNational Telecom Policy - 2012Sushubh MittalNo ratings yet

- ITI Palakkad-IT ReportDocument28 pagesITI Palakkad-IT ReportMuhammed MasinNo ratings yet

- Assignment OF Business EnvironmentDocument18 pagesAssignment OF Business Environmenthimanshu_choudhary_2No ratings yet

- Evolution of Telecom Industry The 19 CenturyDocument6 pagesEvolution of Telecom Industry The 19 CenturyJoseph KuncheriaNo ratings yet

- Evolution of India's Telecom IndustryDocument6 pagesEvolution of India's Telecom IndustryJoseph KuncheriaNo ratings yet

- Brand Management ProjectDocument37 pagesBrand Management Projectanindya_kundu67% (6)

- Resarch and Innovation CenterDocument21 pagesResarch and Innovation CenterHarsh LadNo ratings yet

- INTRO TO INDIAN TELECOMDocument21 pagesINTRO TO INDIAN TELECOMvineet tiwariNo ratings yet

- Chapter - 1: (Type Text)Document21 pagesChapter - 1: (Type Text)vineet tiwariNo ratings yet

- 11AprRecommondation 12apr11Document244 pages11AprRecommondation 12apr11RUCHITA TRIPATHINo ratings yet

- Growth in IT SectorDocument15 pagesGrowth in IT Sectorjeet_singh_deepNo ratings yet

- Project Report On Financial Comparison of Various Telecom Companies in IndiaDocument105 pagesProject Report On Financial Comparison of Various Telecom Companies in Indiasumithanda1988100% (5)

- Index: Chapter 1Document71 pagesIndex: Chapter 1NarayanNo ratings yet

- Contemporary Issues in ManagementDocument25 pagesContemporary Issues in ManagementShreyansh ShahNo ratings yet

- Indian Institute of Management Lucknow: International Business Environment Assignment # 2Document15 pagesIndian Institute of Management Lucknow: International Business Environment Assignment # 2Rachit GauravNo ratings yet

- Customer Satisfaction On JioDocument75 pagesCustomer Satisfaction On JioPrince Kumar0% (1)

- A Study of Telecommunication Service Provider in Indian MarketDocument28 pagesA Study of Telecommunication Service Provider in Indian MarketMehreen Munaf ShaikhNo ratings yet

- AirtelDocument75 pagesAirtelVishal JogiNo ratings yet

- Airtel Project PDFDocument50 pagesAirtel Project PDFhika50% (2)

- DRAFT Copy of National Broadband Policy For Uganda - 17th Sept. 2018Document43 pagesDRAFT Copy of National Broadband Policy For Uganda - 17th Sept. 2018The Independent MagazineNo ratings yet

- IT Industry in IndiaDocument22 pagesIT Industry in IndiakrisNo ratings yet

- CIT418ASSIGNMENTDocument9 pagesCIT418ASSIGNMENTsammyNo ratings yet

- Strategic Development of Technology in China: Breakthroughs and TrendsFrom EverandStrategic Development of Technology in China: Breakthroughs and TrendsNo ratings yet

- Ion of Time in Certain Other CasesxxxxxDocument2 pagesIon of Time in Certain Other CasesxxxxxKapil KaroliyaNo ratings yet

- Liquidation of Damages Not A Bar To Specific PerformanceyyyyyyyyDocument3 pagesLiquidation of Damages Not A Bar To Specific PerformanceyyyyyyyyKapil KaroliyaNo ratings yet

- Contract To Sell or Let Property by One Who Has No TitlezzzzzzzzzzDocument3 pagesContract To Sell or Let Property by One Who Has No TitlezzzzzzzzzzKapil KaroliyaNo ratings yet

- E Specific Relief ActxxxDocument2 pagesE Specific Relief ActxxxKapil KaroliyaNo ratings yet

- Cases in Which Specific Performance of Contracts Connected With Trusts EnforceablexxxxxxxxxxDocument3 pagesCases in Which Specific Performance of Contracts Connected With Trusts EnforceablexxxxxxxxxxKapil KaroliyaNo ratings yet

- ZZZZZZZZZDocument2 pagesZZZZZZZZZKapil KaroliyaNo ratings yet

- Effect of Payment On Account of Debt or of Interest On LegacyxxxxxDocument3 pagesEffect of Payment On Account of Debt or of Interest On LegacyxxxxxKapil KaroliyaNo ratings yet

- Specific Relief Act, 1963 overviewDocument2 pagesSpecific Relief Act, 1963 overviewKapil KaroliyaNo ratings yet

- Tinguishment of Right To PropertyzzzzzzzzzDocument2 pagesTinguishment of Right To PropertyzzzzzzzzzKapil KaroliyaNo ratings yet

- Loan Agreement: 1. Parties of The AgreementDocument3 pagesLoan Agreement: 1. Parties of The AgreementKapil KaroliyaNo ratings yet

- Limitation Act 1963 SummaryDocument4 pagesLimitation Act 1963 SummaryKapil KaroliyaNo ratings yet

- Religions: Compassion For Living Creatures in Indian Law CourtsDocument21 pagesReligions: Compassion For Living Creatures in Indian Law CourtsShivam ShreshthaNo ratings yet

- Earnest Money ContractDocument3 pagesEarnest Money ContractKapil KaroliyaNo ratings yet

- Agreement For Purchase & Sale of Real Estate (Subject To Transaction)Document1 pageAgreement For Purchase & Sale of Real Estate (Subject To Transaction)Kapil Karoliya100% (1)

- Agreement For Purchase & Sale of Real Estate (Subject To Transaction)Document1 pageAgreement For Purchase & Sale of Real Estate (Subject To Transaction)Kapil Karoliya100% (1)

- Purchase AgreementDocument5 pagesPurchase AgreementRoldan LualhatiNo ratings yet

- Real Estate Agreement FormDocument3 pagesReal Estate Agreement FormKapil KaroliyaNo ratings yet

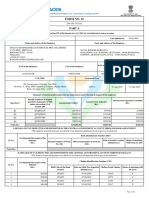

- Personal Loan Agreement Breakdown for The South Indian BankDocument13 pagesPersonal Loan Agreement Breakdown for The South Indian BankKapil KaroliyaNo ratings yet

- Sample Real Estate Purchase AgreementDocument3 pagesSample Real Estate Purchase AgreementObodai MannyNo ratings yet

- Agreement Purchase MBRS ProjectDocument4 pagesAgreement Purchase MBRS ProjectSahil FarazNo ratings yet

- Agreement Purchase MBRS ProjectDocument4 pagesAgreement Purchase MBRS ProjectSahil FarazNo ratings yet

- Purchase Sale ContractDocument7 pagesPurchase Sale ContractKapil Karoliya100% (2)

- Loan Agreement FormDocument34 pagesLoan Agreement FormKapil KaroliyaNo ratings yet

- Agreement Purchase MBRS ProjectDocument4 pagesAgreement Purchase MBRS ProjectSahil FarazNo ratings yet

- Lender Borrower PDFDocument7 pagesLender Borrower PDFPranav PalNo ratings yet

- Kapil Karolia Jurischeck1Document14 pagesKapil Karolia Jurischeck1Kapil KaroliyaNo ratings yet

- Loan Agreement: 1. Parties of The AgreementDocument3 pagesLoan Agreement: 1. Parties of The AgreementKapil KaroliyaNo ratings yet

- Naval Kishore Karolia - BYVPK8532M - 2020-21Document7 pagesNaval Kishore Karolia - BYVPK8532M - 2020-21Kapil KaroliyaNo ratings yet

- HHLGWR00377647 RPS - Naval Home Loan DeatailsDocument10 pagesHHLGWR00377647 RPS - Naval Home Loan DeatailsKapil KaroliyaNo ratings yet

- Jurisprudence Draft PDFDocument12 pagesJurisprudence Draft PDFsunilisraelNo ratings yet

- Pak Plas For Web PDFDocument160 pagesPak Plas For Web PDFHusnain ArifNo ratings yet

- Corporate Finance Assignment Ultratech EIC AnalysisDocument19 pagesCorporate Finance Assignment Ultratech EIC AnalysisAditya Bikram SinghNo ratings yet

- BEN Digital Nepal Framework V7.2March2019Document359 pagesBEN Digital Nepal Framework V7.2March2019TekNo ratings yet

- The Impact of Digital Infrastructure On The Sustainable Development Goals A Study For Selected Latin American and Caribbean Countries en enDocument109 pagesThe Impact of Digital Infrastructure On The Sustainable Development Goals A Study For Selected Latin American and Caribbean Countries en enShokhrukh AvazovNo ratings yet

- FSR June 2021 FinalDocument58 pagesFSR June 2021 FinalSaint CutesyNo ratings yet

- Support For Growth Oriented Women Entrepreneurs GOWE Ethiopia - Timothy MaheaDocument79 pagesSupport For Growth Oriented Women Entrepreneurs GOWE Ethiopia - Timothy MaheaMaheaNo ratings yet

- Circular Flow InfographicDocument1 pageCircular Flow InfographicMaria ConstanciaNo ratings yet

- An Analysis of The Effect of Fiscal Decentralisation On Eonomic Growth in NigeriaDocument9 pagesAn Analysis of The Effect of Fiscal Decentralisation On Eonomic Growth in NigeriaRoni JatmikoNo ratings yet

- Economic Survey 2019 2020 NammaKPSC PDFDocument966 pagesEconomic Survey 2019 2020 NammaKPSC PDFRavindra PujarNo ratings yet

- Economic SurveyDocument11 pagesEconomic SurveycfzbscjdghNo ratings yet

- Colombia Pharmaceuticals and Healthcare Report Q1 2019Document69 pagesColombia Pharmaceuticals and Healthcare Report Q1 2019Anonymous jzlDMsI9cNo ratings yet

- Edexcel Coursework Mark SchemeDocument8 pagesEdexcel Coursework Mark Schemegpwefhvcf100% (2)

- Gapminder Dataset OverviewDocument24 pagesGapminder Dataset OverviewaustronesianNo ratings yet

- SPP Capital Market Update July 2023Document10 pagesSPP Capital Market Update July 2023Jake RoseNo ratings yet

- Quantitative Recession PredictionDocument10 pagesQuantitative Recession PredictionRd PatelNo ratings yet

- Market Strategy Americas The Ins and Outs of The Labor MarketDocument47 pagesMarket Strategy Americas The Ins and Outs of The Labor MarketEduardo Gil Fernandez SanmamedNo ratings yet

- UntitledDocument311 pagesUntitledNickNo ratings yet

- AquinoDocument4 pagesAquinoJanessa EngengNo ratings yet

- Sweet Delight Co.,Ltd.Document159 pagesSweet Delight Co.,Ltd.Alice Kwon100% (1)

- The Sustainable Development Goals SDGS, Targets, and IndicatorsDocument21 pagesThe Sustainable Development Goals SDGS, Targets, and IndicatorsJan Dash100% (1)

- Nepal Market Study PDFDocument149 pagesNepal Market Study PDFBodhiNo ratings yet

- India's Economy and Foreign Trade Since PlanningDocument44 pagesIndia's Economy and Foreign Trade Since PlanningPooja Singh SolankiNo ratings yet

- Rakesh Jhunjhunwala Latest PresentationDocument52 pagesRakesh Jhunjhunwala Latest PresentationMark Fidelman94% (18)

- Industrial Growth, R Nagraj - Entry in Basu and Maertens Edited CompanionDocument4 pagesIndustrial Growth, R Nagraj - Entry in Basu and Maertens Edited CompanionRohit KumarNo ratings yet

- Mirae Asset Multicap Fund NFO PPT - 28 July 2023 To 11 Aug 2023Document37 pagesMirae Asset Multicap Fund NFO PPT - 28 July 2023 To 11 Aug 2023Sajid NavyNo ratings yet

- International Business: Part Two Comparative Environmental FrameworksDocument10 pagesInternational Business: Part Two Comparative Environmental FrameworksMassiel Prz OliveroNo ratings yet

- Indian FMCG MarketDocument42 pagesIndian FMCG MarketSud Sri100% (1)

- Role of International Marketing in Economic DevelopmentDocument12 pagesRole of International Marketing in Economic DevelopmentAdnan ChaudhryNo ratings yet

- Bba Thesis TopicsDocument5 pagesBba Thesis Topicshwxmyoief100% (2)

- 8 - Income and SpendingDocument6 pages8 - Income and SpendingmalingapereraNo ratings yet