You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chevron Vs CIRDocument2 pagesChevron Vs CIRKim Lorenzo CalatravaNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruNANDAN SALESNo ratings yet

- Tax 1 Summative 1 Multiple ChoiceDocument3 pagesTax 1 Summative 1 Multiple ChoiceVon Andrei MedinaNo ratings yet

- Taxation (United Kingdom) : March/June 2016 - Sample QuestionsDocument15 pagesTaxation (United Kingdom) : March/June 2016 - Sample QuestionsAmbreen KureemunNo ratings yet

- Jun 2015 Q PDFDocument14 pagesJun 2015 Q PDFAmbreen KureemunNo ratings yet

- Jun 2014 Q PDFDocument14 pagesJun 2014 Q PDFAmbreen KureemunNo ratings yet

- Dec 2013 A PDFDocument10 pagesDec 2013 A PDFAmbreen KureemunNo ratings yet

- Financial Reporting (F7) : Conceptual FrameworkDocument3 pagesFinancial Reporting (F7) : Conceptual FrameworkAmbreen KureemunNo ratings yet

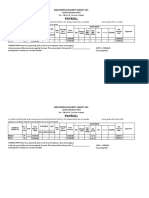

- Payroll: High Profile Security Agency IncDocument20 pagesPayroll: High Profile Security Agency IncRobert Mequila IINo ratings yet

- Serv Let ControllerDocument1 pageServ Let ControllerParas PareekNo ratings yet

- Principles of Taxation For Business and Investment Planning 16th Edition Jones Solutions ManualDocument20 pagesPrinciples of Taxation For Business and Investment Planning 16th Edition Jones Solutions Manualkevahanhksf100% (33)

- Downloadfile 2Document17 pagesDownloadfile 2Jung Hwan SoNo ratings yet

- ProTools Subscription Invoice - March 2020Document1 pageProTools Subscription Invoice - March 2020thathy78No ratings yet

- Rajapushpa Eterna 4bhk Price ListDocument1 pageRajapushpa Eterna 4bhk Price ListrajeshNo ratings yet

- Tax2 Seatworks-03.30.2020Document4 pagesTax2 Seatworks-03.30.2020Allen Fey De JesusNo ratings yet

- Latihan Uts Ganjil - Kelompok 1Document3 pagesLatihan Uts Ganjil - Kelompok 1Aiko KharendhaNo ratings yet

- Ay2021-22 12baDocument2 pagesAy2021-22 12bazaffsanNo ratings yet

- Public Finance 5 Ability To Pay Benefit Principlesacrifice and Lafer CurveDocument24 pagesPublic Finance 5 Ability To Pay Benefit Principlesacrifice and Lafer CurveRameez RajaNo ratings yet

- Analisa Penerapan Perhitungan Rekonsoliasi Fiskal Terhadap Laporan Keungan KomersialDocument17 pagesAnalisa Penerapan Perhitungan Rekonsoliasi Fiskal Terhadap Laporan Keungan KomersialNur Afiah MilleniaNo ratings yet

- A To Z of Payroll Guide 2021Document43 pagesA To Z of Payroll Guide 2021melanieNo ratings yet

- UTG Training Flyer Dampha FannehDocument1 pageUTG Training Flyer Dampha FannehMr DamphaNo ratings yet

- ACCT 553 Week 7 HW SolutionDocument3 pagesACCT 553 Week 7 HW SolutionMohammad Islam100% (1)

- Document PDFDocument2 pagesDocument PDFsherrimcateeNo ratings yet

- ITR DocumentDocument6 pagesITR DocumentRamesh BabuNo ratings yet

- SS2 Economics Scheme of Work For 3RD Term 2021-2022Document4 pagesSS2 Economics Scheme of Work For 3RD Term 2021-2022lenee letambari100% (1)

- Employee's Withholding Exemption and County Status CertificateDocument2 pagesEmployee's Withholding Exemption and County Status CertificateAparajeeta GuhaNo ratings yet

- Melanie S. Samsona Business Tax Chapter 7 ExercisesDocument3 pagesMelanie S. Samsona Business Tax Chapter 7 ExercisesMelanie SamsonaNo ratings yet

- Pas 12 Income - TaxesDocument1 pagePas 12 Income - TaxeshsjhsNo ratings yet

- Quotation - Mrs RikaDocument1 pageQuotation - Mrs RikaDANESTHA AVENo ratings yet

- Residential Status Scope of Total IncomeDocument4 pagesResidential Status Scope of Total IncomedeepakadhanaNo ratings yet

- Taxation of Foreign Source Income by Philippine TaxpayersDocument1 pageTaxation of Foreign Source Income by Philippine TaxpayersMarlon Ty ManaloNo ratings yet

- (A Unit of Maa Vaishno Group of Hotel & Services) : Ghazipur - 233001 209, Chawani Line, Vikash Bhawan Road DuplicateDocument1 page(A Unit of Maa Vaishno Group of Hotel & Services) : Ghazipur - 233001 209, Chawani Line, Vikash Bhawan Road DuplicateVedansh SrivastavaNo ratings yet

- Definitions - No Definition in The Code For: G. Capital Gains & LossesDocument5 pagesDefinitions - No Definition in The Code For: G. Capital Gains & LossesJen MoloNo ratings yet

- Individual Taxation ExercisesDocument3 pagesIndividual Taxation ExercisesMargaux CornetaNo ratings yet

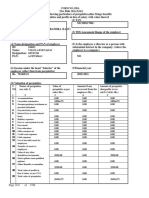

- 22 (Exercise 6: Assignment On Payroll Using Excel)Document1 page22 (Exercise 6: Assignment On Payroll Using Excel)dag mawiNo ratings yet