You might also like

- Zealcon Engineering Pvt. LTD: Item # Direct Cost Civil Mech E & I Total Amount (PKR)Document14 pagesZealcon Engineering Pvt. LTD: Item # Direct Cost Civil Mech E & I Total Amount (PKR)saud idreesNo ratings yet

- Paystub 202109Document1 pagePaystub 202109Ankush BarheNo ratings yet

- CIR vs Pawnshop Tax ProtestDocument4 pagesCIR vs Pawnshop Tax ProtestMac Duguiang Jr.No ratings yet

- Dashboard - SAI - PreviewReports - 2011Document73 pagesDashboard - SAI - PreviewReports - 2011Oh Oh OhNo ratings yet

- Taxation of Fringe Benefits: (Art 212, Labor Code)Document7 pagesTaxation of Fringe Benefits: (Art 212, Labor Code)Lyca VNo ratings yet

- Smart Notes Acca f6 2015 (35 Pages)Document38 pagesSmart Notes Acca f6 2015 (35 Pages)SrabonBarua100% (2)

- Jawaban Sesi 3 Ujikom Pt. BoombasstikDocument12 pagesJawaban Sesi 3 Ujikom Pt. BoombasstikNada Nadya100% (1)

- S20 TX ZAF Sample AnswersDocument8 pagesS20 TX ZAF Sample AnswersKAH MENG KAMNo ratings yet

- Answers To Questions For Chapter 9 Measuring Relevant Costs and Revenues For Decision-MakingDocument7 pagesAnswers To Questions For Chapter 9 Measuring Relevant Costs and Revenues For Decision-MakingElizabeth Del RosarioNo ratings yet

- UuuuyDocument12 pagesUuuuymacashNo ratings yet

- TXUK 2019 MarJun ADocument11 pagesTXUK 2019 MarJun AmdNo ratings yet

- Fundamentals Level – Skills Module, Paper F6 (UK) December 2014 Answers Taxation (United Kingdom) - Concise SummaryDocument9 pagesFundamentals Level – Skills Module, Paper F6 (UK) December 2014 Answers Taxation (United Kingdom) - Concise SummaryLatoya JohnsonNo ratings yet

- Taxation (Malaysia) Answers and Marking SchemeDocument8 pagesTaxation (Malaysia) Answers and Marking SchemeHar San LeeNo ratings yet

- F6uk 2013 Jun ADocument10 pagesF6uk 2013 Jun ADaniel B Boy NkrumahNo ratings yet

- F6ZWEDocument8 pagesF6ZWEkevior2No ratings yet

- Bishop Group (IAS-21 + Cashflow) : Cfap 1: A A F RDocument1 pageBishop Group (IAS-21 + Cashflow) : Cfap 1: A A F R.No ratings yet

- f6MYS 2019 Sep ADocument9 pagesf6MYS 2019 Sep AChoo LeeNo ratings yet

- The Roundtable On Sustainable Palm Oil: Financial Statements For The Financial Year Ended 30 June 2019Document50 pagesThe Roundtable On Sustainable Palm Oil: Financial Statements For The Financial Year Ended 30 June 2019sakul lukaskusNo ratings yet

- Lian's financial statements for year ended 31 March 2013Document2 pagesLian's financial statements for year ended 31 March 2013StpmTutorialClassNo ratings yet

- TX-CYP Dec 21 AnswersDocument8 pagesTX-CYP Dec 21 AnswersKAM JIA LINGNo ratings yet

- Accounting IAS Model Answers Series 3 2006 Old SyllabusDocument20 pagesAccounting IAS Model Answers Series 3 2006 Old SyllabusAung Zaw HtweNo ratings yet

- F6rom 2009 Jun ADocument13 pagesF6rom 2009 Jun AInga ȚîgaiNo ratings yet

- October 2019 PF ChallanDocument1 pageOctober 2019 PF ChallanTeam ServicesNo ratings yet

- AnswersDocument12 pagesAnswerschimbanguraNo ratings yet

- MFA Test 1 SolutionDocument4 pagesMFA Test 1 SolutionMuhammad ImranNo ratings yet

- Form Nl-4-Premium ScheduleDocument2 pagesForm Nl-4-Premium SchedulerohitNo ratings yet

- Suggested Answers Certified Finance and Accounting Professional Examination - Summer 2019Document9 pagesSuggested Answers Certified Finance and Accounting Professional Examination - Summer 2019Suman UroojNo ratings yet

- AAGB Quarter1 Ended 31.03.2021Document26 pagesAAGB Quarter1 Ended 31.03.2021NUR RAHIMIE FAHMI B.NOOR ADZMAN NUR RAHIMIE FAHMI B.NOOR ADZMANNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- Arunachala Logistics Internal Audit Report SummaryDocument172 pagesArunachala Logistics Internal Audit Report SummaryganeshNo ratings yet

- F6mys 2008 Dec ADocument7 pagesF6mys 2008 Dec ARuma RashydNo ratings yet

- National Rural Access Program CBADocument4 pagesNational Rural Access Program CBAMaiwand KhanNo ratings yet

- V3 Appe SWFT2020 001-098Document98 pagesV3 Appe SWFT2020 001-098Hao CuiNo ratings yet

- Tax implications of share listing for investment holding companyDocument15 pagesTax implications of share listing for investment holding companyFakhrul Azman NawiNo ratings yet

- The Financial Plan: Business Expenses As Two Categories Start-Up Expenses and Operating ExpensesDocument2 pagesThe Financial Plan: Business Expenses As Two Categories Start-Up Expenses and Operating ExpensesShamanth MNo ratings yet

- APT Tax AssignmentDocument11 pagesAPT Tax AssignmentMalik JavidNo ratings yet

- Rasgas Company LTD Offshore Expansion Project: Train 4 (WH No.5)Document1 pageRasgas Company LTD Offshore Expansion Project: Train 4 (WH No.5)MarkyNo ratings yet

- Test 3 2019 MemoDocument5 pagesTest 3 2019 MemoKoti KatishiNo ratings yet

- HDFC ERGO General Insurance Company Limited: Policy No. 2311 2007 3732 9204 000Document2 pagesHDFC ERGO General Insurance Company Limited: Policy No. 2311 2007 3732 9204 000Padmaja SNo ratings yet

- TXUK 2019 SepDec - ADocument10 pagesTXUK 2019 SepDec - AmdNo ratings yet

- TAX2601 2023 S1 Assessment 5 SolutionDocument4 pagesTAX2601 2023 S1 Assessment 5 SolutionNomthandazo SikhosanaNo ratings yet

- F6 (UK) Taxation (United Kingdom) exam answers and explanationDocument11 pagesF6 (UK) Taxation (United Kingdom) exam answers and explanationInsia AhmedNo ratings yet

- 2-3mwi 2004 Dec ADocument13 pages2-3mwi 2004 Dec Aanga100% (1)

- Rl1Chfilzri (Indlll) LTDDocument4 pagesRl1Chfilzri (Indlll) LTDJigneshNo ratings yet

- CT Engineering Polymers PVT LTD PDFDocument2 pagesCT Engineering Polymers PVT LTD PDFSangeetaNo ratings yet

- CS 2022Document1 pageCS 2022dk1100861No ratings yet

- Proforma 1Document1 pageProforma 1Haftom TekluNo ratings yet

- CS2022 (15)Document2 pagesCS2022 (15)gst65206No ratings yet

- Partnership Income Computation YA 2008Document4 pagesPartnership Income Computation YA 2008NUR DARWISYAH KAMARUDINNo ratings yet

- 高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementDocument13 pages高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementIskandar BudionoNo ratings yet

- 06chap 6 NP Fringe Benefits Solutions 2020Document2 pages06chap 6 NP Fringe Benefits Solutions 202044v8ct8cdyNo ratings yet

- ANNEXURE 4 - Q4 FY08-09 Consolidated ResultsDocument1 pageANNEXURE 4 - Q4 FY08-09 Consolidated ResultsPGurusNo ratings yet

- National Rural Support Programme Overall Reconciliation With GL/Trail 2018-19Document37 pagesNational Rural Support Programme Overall Reconciliation With GL/Trail 2018-19Naseem BalochNo ratings yet

- Swinburne University ACC10007 Discussion QuestionsDocument5 pagesSwinburne University ACC10007 Discussion QuestionsRenee WongNo ratings yet

- General Journal - Adjusting Entries December, 31 2017 (In RP.)Document12 pagesGeneral Journal - Adjusting Entries December, 31 2017 (In RP.)Zahra Nur FajriyahNo ratings yet

- Deleum Q2 2019Document43 pagesDeleum Q2 2019DiLungBanNo ratings yet

- Annual Report 2019 Financial Statements and Notes PDFDocument124 pagesAnnual Report 2019 Financial Statements and Notes PDFArti AtkaleNo ratings yet

- FAC3761 - Exam Prep - Mock Question Paper - Suggested SolutionDocument9 pagesFAC3761 - Exam Prep - Mock Question Paper - Suggested SolutionRene EngelbrechtNo ratings yet

- 6012 MAXIS QR 2020-12-31 MaxisBerhadQ42020 - 512429564Document37 pages6012 MAXIS QR 2020-12-31 MaxisBerhadQ42020 - 512429564Sarah AriffNo ratings yet

- F6zwe 2018 Jun ADocument6 pagesF6zwe 2018 Jun AcypriancourageNo ratings yet

- Project/Estimate Detail Report (GST)Document9 pagesProject/Estimate Detail Report (GST)Subhash DhakarNo ratings yet

- Seminar on Accounting Theory and PracticeDocument13 pagesSeminar on Accounting Theory and PracticeDEEPALI ANANDNo ratings yet

- Engineering: Reliance Naval and Limited (Formerly Limited)Document5 pagesEngineering: Reliance Naval and Limited (Formerly Limited)gowtham raju buttiNo ratings yet

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Jun 2015 A PDFDocument10 pagesJun 2015 A PDFAmbreen KureemunNo ratings yet

- Taxation (United Kingdom) : March/June 2016 - Sample QuestionsDocument15 pagesTaxation (United Kingdom) : March/June 2016 - Sample QuestionsAmbreen KureemunNo ratings yet

- Jun 2015 Q PDFDocument14 pagesJun 2015 Q PDFAmbreen KureemunNo ratings yet

- Jun 2016 A PDFDocument7 pagesJun 2016 A PDFAmbreen KureemunNo ratings yet

- Jun 2014 Q PDFDocument14 pagesJun 2014 Q PDFAmbreen KureemunNo ratings yet

- F6uk 2013 Jun Q PDFDocument12 pagesF6uk 2013 Jun Q PDFInsia AhmedNo ratings yet

- Dec 2014 Q PDFDocument14 pagesDec 2014 Q PDFAmbreen KureemunNo ratings yet

- F6UK 2014 Jun ADocument10 pagesF6UK 2014 Jun ASajidZiaNo ratings yet

- F6uk 2013 Jun ADocument10 pagesF6uk 2013 Jun ADaniel B Boy NkrumahNo ratings yet

- F6uk 2012 Dec QDocument13 pagesF6uk 2012 Dec QSaad HassanNo ratings yet

- Revision Kid F6 2015Document9 pagesRevision Kid F6 2015Rabin JoshiNo ratings yet

- Financial Reporting (F7) : Conceptual FrameworkDocument3 pagesFinancial Reporting (F7) : Conceptual FrameworkAmbreen KureemunNo ratings yet

- Dec 2013 Q PDFDocument14 pagesDec 2013 Q PDFAmbreen KureemunNo ratings yet

- F6UK 2012 Dec AnsDocument9 pagesF6UK 2012 Dec AnsamirahimiNo ratings yet

- F6 AnsDocument9 pagesF6 AnsRaza AliNo ratings yet

- Bay Impex Pte. LTD.: InvoiceDocument1 pageBay Impex Pte. LTD.: InvoiceKhalid Z.No ratings yet

- Tax Planning For Shut Down or ContinueDocument4 pagesTax Planning For Shut Down or ContinueDr Linda Mary Simon75% (4)

- PauslipDocument2 pagesPauslipAmanNo ratings yet

- LW-204 Professional Ethics Bar Bench Relation and Accountancy For Lawyers.Document2 pagesLW-204 Professional Ethics Bar Bench Relation and Accountancy For Lawyers.Rubab ShaikhNo ratings yet

- GST and Financial ServicesDocument25 pagesGST and Financial ServicesIrfanRKNo ratings yet

- Tutorial 3 QDocument3 pagesTutorial 3 Q謝中豪No ratings yet

- Quote and Order FormsDocument2 pagesQuote and Order FormsMoni FraileNo ratings yet

- Depreciation Analysis by CA Vijay SardaDocument1 pageDepreciation Analysis by CA Vijay SardaAnish JainNo ratings yet

- HSRP Online Appointment ReceiptDocument1 pageHSRP Online Appointment Receiptfayada bazaarNo ratings yet

- Pi 000087Document1 pagePi 000087maviyom.documentsNo ratings yet

- Bangladesh Customs, National Board of Revenue (NBR) 5Document2 pagesBangladesh Customs, National Board of Revenue (NBR) 5Mohsin Ul Amin KhanNo ratings yet

- Registration Guide: MAY 2020 SemesterDocument11 pagesRegistration Guide: MAY 2020 SemesterLi Shin LeeNo ratings yet

- InvoiceDocument1 pageInvoiceertop736No ratings yet

- Ias 12 TaxationDocument15 pagesIas 12 TaxationHải AnhNo ratings yet

- Lecture-3 Income Classsification and Residential StatusDocument25 pagesLecture-3 Income Classsification and Residential Statusimdadul haqueNo ratings yet

- Amit Cotton Industries vs. Principal Commissioner of Customs Gujarat High CourtDocument49 pagesAmit Cotton Industries vs. Principal Commissioner of Customs Gujarat High CourtMaragani MuraligangadhararaoNo ratings yet

- Scenario 1Document24 pagesScenario 1girirajNo ratings yet

- In Re Atty Bernardo ZialcitaDocument3 pagesIn Re Atty Bernardo ZialcitaMCNo ratings yet

- Sodexo Meal Pass FAQsDocument5 pagesSodexo Meal Pass FAQsJyothsna KotteNo ratings yet

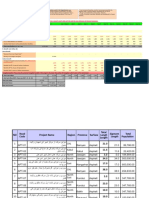

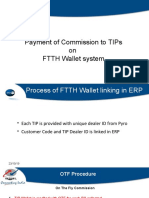

- FTTH Commission Payment ProcessDocument12 pagesFTTH Commission Payment ProcessVikrant PathakNo ratings yet

- Harvard Financial Aid Verification Non-FilerDocument1 pageHarvard Financial Aid Verification Non-Filerparth shuklaNo ratings yet

- One Piece Film Red Sat 01 Oct 1300 TicketsDocument1 pageOne Piece Film Red Sat 01 Oct 1300 TicketsKaren BautistaNo ratings yet

- FINANCE BUDDY PAYSLIPSDocument3 pagesFINANCE BUDDY PAYSLIPSshubham DeshmukhNo ratings yet

- CP PLUS Certified IP Training Programme (CSE Level-I) : Participant Registration Form (CSE - 011/CHENNAI)Document1 pageCP PLUS Certified IP Training Programme (CSE Level-I) : Participant Registration Form (CSE - 011/CHENNAI)giri xdaNo ratings yet

- Individual Return IT-Gha (2023) 1Document2 pagesIndividual Return IT-Gha (2023) 1monir7898No ratings yet

- Payslip 2190724 CIN Mar 2023Document1 pagePayslip 2190724 CIN Mar 2023sekhar nadimintiNo ratings yet

- 1574 Ir I 20208182020 - 63721 - PM PDFDocument2 pages1574 Ir I 20208182020 - 63721 - PM PDFSaleem SoomroNo ratings yet