You might also like

- Standard Operating Procedure Concentrated AcidsDocument6 pagesStandard Operating Procedure Concentrated AcidsDibyendu GhoshNo ratings yet

- Use The Following Information For The Next Two QuestionsDocument59 pagesUse The Following Information For The Next Two QuestionsAllecks Juel LuchanaNo ratings yet

- Use The Following Information For The Next Three Questions:: Activity 3.2Document11 pagesUse The Following Information For The Next Three Questions:: Activity 3.2Jade jade jadeNo ratings yet

- Accounting For Business CombinationsDocument29 pagesAccounting For Business CombinationsAmie Jane MirandaNo ratings yet

- Chapter 5 - Teacher's Manual - Afar Part 1Document15 pagesChapter 5 - Teacher's Manual - Afar Part 1Mayeth BotinNo ratings yet

- Consolidated FS - QUIZ PART 3Document4 pagesConsolidated FS - QUIZ PART 3Christine Jane Ramos100% (1)

- Bright Co. Dull Co. AssetsDocument5 pagesBright Co. Dull Co. AssetsJJ JaumNo ratings yet

- Home Office and Branch AccountingDocument5 pagesHome Office and Branch AccountingMaryjoy Sarzadilla JuanataNo ratings yet

- Chapter 1 Business Combinations - Part 1Document24 pagesChapter 1 Business Combinations - Part 1Kathlyn Tajada0% (1)

- Consolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)Document3 pagesConsolidated Financial Statements: XYZ, Inc. Carrying Amounts Fair Values Fair Value Adjustments (FVA)mhar lon100% (2)

- Chapter 4 Accounting For Business Combinations SolmanDocument16 pagesChapter 4 Accounting For Business Combinations SolmanCharlene Bolandres100% (1)

- Acc 113 2nd Periodical Examination PDF FreeDocument17 pagesAcc 113 2nd Periodical Examination PDF FreeStefanie FerminNo ratings yet

- Accountancy Student: Froilan Arlando BandulaDocument5 pagesAccountancy Student: Froilan Arlando BandulaGlennizze GalvezNo ratings yet

- Chapter 25 - Acctg For Derivatives and Hedging Part 4Document9 pagesChapter 25 - Acctg For Derivatives and Hedging Part 4PutmehudgJasdNo ratings yet

- Sol. Man. - Chapter 5 - Corporate Liquidation Reorganization - 2020 EditionDocument22 pagesSol. Man. - Chapter 5 - Corporate Liquidation Reorganization - 2020 Editiondianel villarico100% (1)

- Solution To Assign - Prob 3 Home Office, Branch and Agency AccountingDocument4 pagesSolution To Assign - Prob 3 Home Office, Branch and Agency Accountingmhikeedelantar100% (1)

- Chapter 24 - Acctg For Derivatives and Hedging Part 3Document36 pagesChapter 24 - Acctg For Derivatives and Hedging Part 3PutmehudgJasdNo ratings yet

- Picture CatDocument2 pagesPicture Catapi-361274406No ratings yet

- Chapter 4 Teachers Manual Afar Part 1Document13 pagesChapter 4 Teachers Manual Afar Part 1cezyyyyyyNo ratings yet

- Answers To Quiz 1 Period 3Document4 pagesAnswers To Quiz 1 Period 3trishaNo ratings yet

- Sol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aDocument21 pagesSol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aJamie Rose Aragones100% (1)

- Consolidated Financial Statement Classroom Discussion Part 2Document6 pagesConsolidated Financial Statement Classroom Discussion Part 2Sunshine KhuletzNo ratings yet

- Abc Chapter 7 Accounting For Business Combinations by Millan 2020Document21 pagesAbc Chapter 7 Accounting For Business Combinations by Millan 2020Charlene Bolandres100% (2)

- Chapter 10 Effects of Changes in Forex RatesDocument16 pagesChapter 10 Effects of Changes in Forex RatesJeeramel TorresNo ratings yet

- Home Office, Branch and Agency Accounting: Problem 11-1: True or FalseDocument13 pagesHome Office, Branch and Agency Accounting: Problem 11-1: True or FalseVenz Lacre100% (1)

- 14 Consolidated FS Pt1 PDFDocument2 pages14 Consolidated FS Pt1 PDFRiselle Ann Sanchez53% (15)

- Sol Man Chapter 8 Separate Fs Acctg For Bus CombinationsDocument2 pagesSol Man Chapter 8 Separate Fs Acctg For Bus Combinationsitsmenatoy100% (2)

- Solutions To Assign. - Prob 4 Construction ContractsDocument8 pagesSolutions To Assign. - Prob 4 Construction ContractsmhikeedelantarNo ratings yet

- Linagliptin - DRUG STUDYDocument1 pageLinagliptin - DRUG STUDYAcads useNo ratings yet

- Direct Quotation Indirect Quotation: Foreign Exchange Rate Theory & ComputationalDocument14 pagesDirect Quotation Indirect Quotation: Foreign Exchange Rate Theory & ComputationalGwen Sula Lacanilao67% (3)

- ACCBCOMB - Oct 10Document13 pagesACCBCOMB - Oct 10kimkim100% (1)

- Use The Following Information For The Next Seven Questions:: Total LiabilitiesDocument7 pagesUse The Following Information For The Next Seven Questions:: Total LiabilitiesRoss John JimenezNo ratings yet

- University of Perpetual Help System DALTA: Las Piñas CampusDocument65 pagesUniversity of Perpetual Help System DALTA: Las Piñas CampusGlennizze Galvez100% (1)

- Consolidated Financial Statements (Part 2) : Problem 1: Multiple Choice - TheoryDocument24 pagesConsolidated Financial Statements (Part 2) : Problem 1: Multiple Choice - TheoryKeith Alison ArellanoNo ratings yet

- Consolidated Financial Statements 1 SolDocument18 pagesConsolidated Financial Statements 1 SolChristine Dela Rosa Carolino100% (1)

- Chapter 9 Financial Reporting in Hyperinflationary EconomiesDocument10 pagesChapter 9 Financial Reporting in Hyperinflationary EconomiesKathrina RoxasNo ratings yet

- Sol. Man. Chapter 12 Acctg For Derivatives Hedging Transactions Part 2 Acctg For Bus. CombinationsDocument11 pagesSol. Man. Chapter 12 Acctg For Derivatives Hedging Transactions Part 2 Acctg For Bus. CombinationsJulyca C. LastimosoNo ratings yet

- Abc Chapter 6 Accounting For Business Combinations by Millan 2020Document14 pagesAbc Chapter 6 Accounting For Business Combinations by Millan 2020Nayoung LeeNo ratings yet

- Chapter 16 - Bus Com Part 3 - Afar Part 2-1Document5 pagesChapter 16 - Bus Com Part 3 - Afar Part 2-1Glennizze GalvezNo ratings yet

- ABC Chapter 5 Accounting For Business Combinations by Millan 2020Document25 pagesABC Chapter 5 Accounting For Business Combinations by Millan 2020Nayoung LeeNo ratings yet

- Profe03 Activity Chapter 7Document5 pagesProfe03 Activity Chapter 7eloisa celisNo ratings yet

- Chapter 6 ADVAC (Excel +Document43 pagesChapter 6 ADVAC (Excel +Christine Jane RamosNo ratings yet

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- Buss. Combi PrelimDocument8 pagesBuss. Combi PrelimPhia TeoNo ratings yet

- Quiz - Chapter 13 - Basic DerivativesDocument5 pagesQuiz - Chapter 13 - Basic DerivativesJaymee Andomang Os-ag27% (11)

- Owl Co. and Owlet Co. - NCI in Net AssetsDocument11 pagesOwl Co. and Owlet Co. - NCI in Net AssetsKristine Esplana ToraldeNo ratings yet

- Arlyn Pineda vs. Julie Arcalas - Case DigestDocument1 pageArlyn Pineda vs. Julie Arcalas - Case DigestJillian AsdalaNo ratings yet

- Sol. Man. Chapter 10 The Effects of Changes in Foreign Exchange Rates Acctg For Bus. CombinationsDocument19 pagesSol. Man. Chapter 10 The Effects of Changes in Foreign Exchange Rates Acctg For Bus. CombinationsJulyca C. LastimosoNo ratings yet

- Millan ConsignmentDocument5 pagesMillan Consignmenttonyalmon0% (1)

- Illustration Financial Reptg. in HyperinflationaryDocument4 pagesIllustration Financial Reptg. in HyperinflationaryKian GaboroNo ratings yet

- Chapter 21 - The Effects of Changes in Forex RatesDocument52 pagesChapter 21 - The Effects of Changes in Forex RatesPutmehudgJasd100% (1)

- Chapter 24 - Teachers Manual - Aa Part 2 PDFDocument13 pagesChapter 24 - Teachers Manual - Aa Part 2 PDFSheed ChiuNo ratings yet

- Chapter 10 - Teacher's Manual - Afar Part 1Document20 pagesChapter 10 - Teacher's Manual - Afar Part 1Angelic67% (3)

- Sol. Man. - Chapter 15 EpsDocument12 pagesSol. Man. - Chapter 15 Epsfinn mertensNo ratings yet

- Sol. Man. Chapter 8 Acctg For Franchise Operations Franchisor 2021 EditionDocument11 pagesSol. Man. Chapter 8 Acctg For Franchise Operations Franchisor 2021 EditionkoyNo ratings yet

- Chapter 8 - Teacher's Manual - Afar Part 1Document7 pagesChapter 8 - Teacher's Manual - Afar Part 1Angelic100% (3)

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Practice Problems AcctgDocument10 pagesPractice Problems AcctgRichard ColeNo ratings yet

- Special Trans Activity 2Document15 pagesSpecial Trans Activity 2Rachelle JoseNo ratings yet

- Chapter 15 - Bus. Combination Part 3Document8 pagesChapter 15 - Bus. Combination Part 3PutmehudgJasdNo ratings yet

- Chapter 25 Acctg FOR Derivatives & Hedging Transactions Part 2 Afar Part 2 Chapter 25 Acctg FOR Derivatives & Hedging Transactions Part 2 Afar Part 2Document11 pagesChapter 25 Acctg FOR Derivatives & Hedging Transactions Part 2 Afar Part 2 Chapter 25 Acctg FOR Derivatives & Hedging Transactions Part 2 Afar Part 2Jan OleteNo ratings yet

- Chapter 13 Intermediate AccountingDocument18 pagesChapter 13 Intermediate AccountingDanica Mae GenaviaNo ratings yet

- LM - Chapter 13Document18 pagesLM - Chapter 13PASCUA RENALYN M.No ratings yet

- Topic 3: Assesment ACTIVITY 1: Answer Problems 2 and 3 of The Chapter 13 of Your Book Intermediate Accounting 1 A. Problem 2Document6 pagesTopic 3: Assesment ACTIVITY 1: Answer Problems 2 and 3 of The Chapter 13 of Your Book Intermediate Accounting 1 A. Problem 2Rey HandumonNo ratings yet

- Chapter 26 Acctg For Derivatives Hedging Transactions Part 3 Afar Part 2Document13 pagesChapter 26 Acctg For Derivatives Hedging Transactions Part 3 Afar Part 2Kathrina Roxas100% (1)

- 04 Homework - Answer KeyDocument3 pages04 Homework - Answer KeyVeralou UrbinoNo ratings yet

- Problem XDocument30 pagesProblem XLove FreddyNo ratings yet

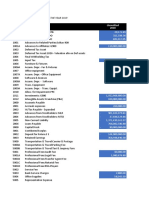

- Unaudited Trial Balance For The Year 2019: Sultan 900 Capital, IncDocument18 pagesUnaudited Trial Balance For The Year 2019: Sultan 900 Capital, IncGlennizze GalvezNo ratings yet

- Entrep 4 Week: What I KnowDocument9 pagesEntrep 4 Week: What I KnowGlennizze GalvezNo ratings yet

- Assets: Balance Sheet As of September 31, 2020Document91 pagesAssets: Balance Sheet As of September 31, 2020Glennizze GalvezNo ratings yet

- SynthesisDocument2 pagesSynthesisGlennizze GalvezNo ratings yet

- January 2019: Sun Mon Tue Wed Thu Fri SatDocument12 pagesJanuary 2019: Sun Mon Tue Wed Thu Fri SatGlennizze GalvezNo ratings yet

- Chapter 14 - Bus Com Part 1 - Afar Part 2-1Document4 pagesChapter 14 - Bus Com Part 1 - Afar Part 2-1Glennizze GalvezNo ratings yet

- Accountancy Student: Froilan Arlando BandulaDocument5 pagesAccountancy Student: Froilan Arlando BandulaGlennizze GalvezNo ratings yet

- Accountants National Capital Region (NFJPIA-NCR) Is A Duly: Ngarap Tungo SA Kilang LaDocument4 pagesAccountants National Capital Region (NFJPIA-NCR) Is A Duly: Ngarap Tungo SA Kilang LaGlennizze GalvezNo ratings yet

- Body Composition: BenefitsDocument8 pagesBody Composition: BenefitsGlennizze GalvezNo ratings yet

- Maxims of CommunicationDocument1 pageMaxims of CommunicationGlennizze GalvezNo ratings yet

- PurposiveDocument1 pagePurposiveGlennizze GalvezNo ratings yet

- 3.2.9 Process FlowchartDocument4 pages3.2.9 Process FlowchartGlennizze GalvezNo ratings yet

- Fun BoothDocument2 pagesFun BoothGlennizze GalvezNo ratings yet

- Bio Plants SurveyDocument1 pageBio Plants SurveyGlennizze GalvezNo ratings yet

- Systems Analysis and Design: Course DescriptionDocument3 pagesSystems Analysis and Design: Course DescriptionGlennizze GalvezNo ratings yet

- CV For Internship PDFDocument5 pagesCV For Internship PDFGlennizze GalvezNo ratings yet

- Accountancy Student: Froilan Arlando BandulaDocument5 pagesAccountancy Student: Froilan Arlando BandulaGlennizze GalvezNo ratings yet

- Critical Questions: 1. What Is More Potent Strategy To Use? Customer Driven or Customer Driving Market?Document2 pagesCritical Questions: 1. What Is More Potent Strategy To Use? Customer Driven or Customer Driving Market?Glennizze GalvezNo ratings yet

- As A Temporary Investment of Excess Cash As Part of A Long-Term Risk-Adjusted Portfolio As A Strategic InvestmentDocument41 pagesAs A Temporary Investment of Excess Cash As Part of A Long-Term Risk-Adjusted Portfolio As A Strategic InvestmentGlennizze GalvezNo ratings yet

- Wikispecies, Free Species DirectoryDocument5 pagesWikispecies, Free Species DirectoryjpescuderoNo ratings yet

- Astm D 36-2020Document5 pagesAstm D 36-2020Mohammed AliNo ratings yet

- Monroe Catalogue 2019 20 PDFDocument320 pagesMonroe Catalogue 2019 20 PDFTata JayaNo ratings yet

- Homework Chapter 13 Case From Text BookDocument23 pagesHomework Chapter 13 Case From Text Bookjhanzab0% (1)

- Human Area NetworkDocument9 pagesHuman Area NetworkLakshman ReddyNo ratings yet

- 2.2 - Isakkson - Biomass Gasification For Lime Kiln ApplicationsDocument15 pages2.2 - Isakkson - Biomass Gasification For Lime Kiln ApplicationsHuy NguyenNo ratings yet

- InTouch 2014 - Part 1 - Wonderware WestDocument6 pagesInTouch 2014 - Part 1 - Wonderware WestmanisegarNo ratings yet

- MASDocument7 pagesMASHelen IlaganNo ratings yet

- Attributes of Front Office Personnel:: Guests)Document8 pagesAttributes of Front Office Personnel:: Guests)Sumit PratapNo ratings yet

- Nec 4106 Module 1Document28 pagesNec 4106 Module 1Jessie Rey MembreveNo ratings yet

- Sumagka v. Sumagka - RODRIGUEZDocument1 pageSumagka v. Sumagka - RODRIGUEZGrafted KoalaNo ratings yet

- ZooscanDocument19 pagesZooscankpmanikandaanNo ratings yet

- Procédure de Test FABIAN EVO-TS-AA-03e - TI - 7250 - Rev04-2017 PDFDocument22 pagesProcédure de Test FABIAN EVO-TS-AA-03e - TI - 7250 - Rev04-2017 PDFDorian BuissonNo ratings yet

- PUB E: 5/31/2021 Top Builders Developers in Mumbai in 2020-2021 - Top and Best in 2021Document7 pagesPUB E: 5/31/2021 Top Builders Developers in Mumbai in 2020-2021 - Top and Best in 2021MINAKSHI SINGHNo ratings yet

- BEC ReportDocument20 pagesBEC ReportSuyash KerkarNo ratings yet

- Jawaban Soal Sales Forecast TM 5Document3 pagesJawaban Soal Sales Forecast TM 5Dhea Alfa NurezaNo ratings yet

- Lecture2 MonopolyDocument58 pagesLecture2 MonopolyGaurav JainNo ratings yet

- Japanese Candlestick ChartingDocument15 pagesJapanese Candlestick ChartingAlex WongNo ratings yet

- International Training: Arpana F. Gawade Dhanashri SDocument8 pagesInternational Training: Arpana F. Gawade Dhanashri SAny KadamNo ratings yet

- Ball Valves: 3-Way SeriesDocument8 pagesBall Valves: 3-Way SerieslorenzoNo ratings yet

- Daikin PA Catalogue Revised Low ResDocument32 pagesDaikin PA Catalogue Revised Low ResKartik PrabhakarNo ratings yet

- Lab ManualDocument65 pagesLab Manualamit bhagureNo ratings yet

- Module 12Document17 pagesModule 12Ritesah MadhunalaNo ratings yet

- FSP Check TX Wrist Oil VolumeDocument4 pagesFSP Check TX Wrist Oil VolumeJulio LiranzoNo ratings yet

- Internal Analysis of FedEx VDocument3 pagesInternal Analysis of FedEx Vjasmine8099100% (1)

- Ownership Structure, Corporate Governance and Firm Performance (#352663) - 363593Document10 pagesOwnership Structure, Corporate Governance and Firm Performance (#352663) - 363593mrzia996No ratings yet