You might also like

- Case 10 - Timing Is EverythingDocument6 pagesCase 10 - Timing Is EverythingMariaAngelicaMargenApe100% (1)

- Trump University Asset Protection 101 Trump University PDFDocument4 pagesTrump University Asset Protection 101 Trump University PDFThumper Kates0% (2)

- Marketing Strategies of AdidasDocument58 pagesMarketing Strategies of Adidasjassi7nishadNo ratings yet

- Ebook PDF CJ 2019 1st Edition by James A Fagin PDFDocument51 pagesEbook PDF CJ 2019 1st Edition by James A Fagin PDFphilip.pelote179100% (32)

- Case Analysis Casa DisenoDocument7 pagesCase Analysis Casa DisenoLexNo ratings yet

- 2011 Aug Tutorial 10 Working Capital ManagementDocument10 pages2011 Aug Tutorial 10 Working Capital ManagementHarmony TeeNo ratings yet

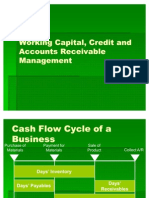

- Working Capital, Credit and Accounts Receivable Management: Reference: ETM Chapter 6 & 7 STFM Chapter 5 & 6Document31 pagesWorking Capital, Credit and Accounts Receivable Management: Reference: ETM Chapter 6 & 7 STFM Chapter 5 & 6sandeep949No ratings yet

- 1) Cash Conversion CycleDocument2 pages1) Cash Conversion CyclesaramumtazNo ratings yet

- Working Capital Management - 131218Document39 pagesWorking Capital Management - 131218bhumika manwaniNo ratings yet

- Unit 7 Working Capital ManagementDocument36 pagesUnit 7 Working Capital ManagementNabin JoshiNo ratings yet

- Working Capital ManagementDocument6 pagesWorking Capital ManagementSameer Ranjan MohapatraNo ratings yet

- 05 - Working Capital ManagementDocument111 pages05 - Working Capital Managementrow rowNo ratings yet

- Corporate Finance Sem3Document7 pagesCorporate Finance Sem3saurabhnanda14No ratings yet

- Operating and Cash Conversion CyclesDocument4 pagesOperating and Cash Conversion CyclesChristoper SalvinoNo ratings yet

- CorporateDocument10 pagesCorporateSumegha JainNo ratings yet

- Mc080405647 Fin621 AssignmentDocument2 pagesMc080405647 Fin621 AssignmentazhersandhuNo ratings yet

- Working Capital ManagementDocument52 pagesWorking Capital ManagementSuraj KumarNo ratings yet

- Chapter 10Document30 pagesChapter 10Nowshad AyubNo ratings yet

- Course: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit CollectionDocument27 pagesCourse: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit Collectionsalsabilla rpNo ratings yet

- Week 10 11 AssignmentDocument4 pagesWeek 10 11 AssignmentAsdfghjkl LkjhgfdsaNo ratings yet

- 1S5 Tarea Set B FinzsDocument8 pages1S5 Tarea Set B Finzsnelson gymNo ratings yet

- CH 18 Part 1Document18 pagesCH 18 Part 1mohab abdelhamedNo ratings yet

- What Is The Formula For Creditor DaysDocument9 pagesWhat Is The Formula For Creditor DaysKathir HaiNo ratings yet

- Assigment - CH.10 Credit AnalysisDocument6 pagesAssigment - CH.10 Credit AnalysisSausan SaniaNo ratings yet

- Working Capital ManagementDocument64 pagesWorking Capital ManagementPrerna SinhaNo ratings yet

- FIN701 Final Exam Cash Conversion CycleDocument24 pagesFIN701 Final Exam Cash Conversion Cycleankita chauhanNo ratings yet

- 05 - Working Capital Management (Notes)Document8 pages05 - Working Capital Management (Notes)Cheezuu DyNo ratings yet

- Charles Ega 3203017162 Case Study Working Capital Management Assessing Roche Publishing Companys Cash Management EfficiencyDocument4 pagesCharles Ega 3203017162 Case Study Working Capital Management Assessing Roche Publishing Companys Cash Management EfficiencyCharles 10No ratings yet

- Working Capital ManagementDocument62 pagesWorking Capital ManagementANISH KUMARNo ratings yet

- Strategic Capital Group Workshop #6: DCF ModelingDocument56 pagesStrategic Capital Group Workshop #6: DCF ModelingUniversity Securities Investment TeamNo ratings yet

- WORKING CAPITAL MANAGEMENET BPFA BCD Bsc PM DIPMDocument90 pagesWORKING CAPITAL MANAGEMENET BPFA BCD Bsc PM DIPMOreratile KeorapetseNo ratings yet

- PAN African E-Network Project: Working Capital ManagementDocument101 pagesPAN African E-Network Project: Working Capital ManagementEng Abdulkadir MahamedNo ratings yet

- Session 6 FINANCIAL PLANNING Working Capital ManagementDocument44 pagesSession 6 FINANCIAL PLANNING Working Capital ManagementXia AlliaNo ratings yet

- PAN African E-Network Project: Working Capital ManagementDocument89 pagesPAN African E-Network Project: Working Capital ManagementEng Abdulkadir MahamedNo ratings yet

- Corporate FinanceDocument7 pagesCorporate Financeaditya prakashNo ratings yet

- Working Capital, Credit and Accounts Receivable ManagementDocument28 pagesWorking Capital, Credit and Accounts Receivable ManagementVinodh Kumar LNo ratings yet

- Corporate FinanceDocument6 pagesCorporate Financejayesh jhaNo ratings yet

- Research TopicDocument2 pagesResearch TopicAsif SaeedNo ratings yet

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNo ratings yet

- Working Capital MGTDocument16 pagesWorking Capital MGTNouman SheikhNo ratings yet

- Cash Cycle CalculatorDocument1 pageCash Cycle CalculatorReza HaryohatmodjoNo ratings yet

- 2,,working Capital ManagementDocument19 pages2,,working Capital ManagementKelvin mwaiNo ratings yet

- CHAPTER 5 - Ratio AnalysisDocument66 pagesCHAPTER 5 - Ratio Analysisela cagsNo ratings yet

- Manage Working Capital & Cash FlowDocument10 pagesManage Working Capital & Cash Flowvalentine mutungaNo ratings yet

- 4working Capital ManagementDocument54 pages4working Capital ManagementErrol LuceroNo ratings yet

- Unit Two: Managing Cash and Marketable SecuritiesDocument31 pagesUnit Two: Managing Cash and Marketable SecuritiesmeseleNo ratings yet

- Need of Working Capital & Concept of Operating Cyycle: Presented By:-G.Venket Ramana Ujjayani PatraDocument11 pagesNeed of Working Capital & Concept of Operating Cyycle: Presented By:-G.Venket Ramana Ujjayani PatraVenket RamanaNo ratings yet

- Project Appraisal Ratio Analysis - 2023 - Students - SlidesDocument36 pagesProject Appraisal Ratio Analysis - 2023 - Students - SlidesThaboNo ratings yet

- CH 09 Valuing Early-Stage VenturesDocument20 pagesCH 09 Valuing Early-Stage VenturesshakeelsajjadNo ratings yet

- OC and CCC - AsynchronousDocument29 pagesOC and CCC - AsynchronousChristoper SalvinoNo ratings yet

- Chapter 17 - AnswerDocument6 pagesChapter 17 - Answerwynellamae67% (3)

- Working Capital Tools and TechniquesDocument60 pagesWorking Capital Tools and TechniquesMaria Bernadita RiveraNo ratings yet

- Chapter 3 - Financial Statement AnalysisDocument22 pagesChapter 3 - Financial Statement AnalysisReyes JonahNo ratings yet

- Business Finance Week 4: Financial Ratios Analysis and Interpretation Background Information For LearnersDocument8 pagesBusiness Finance Week 4: Financial Ratios Analysis and Interpretation Background Information For LearnersCarl Daniel DoromalNo ratings yet

- Revison CF 13.07.2023 (All)Document116 pagesRevison CF 13.07.2023 (All)seyon sithamparanathanNo ratings yet

- Seminar 10 WCMDocument8 pagesSeminar 10 WCMHeng CzNo ratings yet

- Cash Operating CycleDocument2 pagesCash Operating CycleAyman RamyNo ratings yet

- Cash Conversion Cycle of Rafhan Maize ProductsDocument5 pagesCash Conversion Cycle of Rafhan Maize Productsmuhammad farhanNo ratings yet

- Businessfinance12 q3 Mod4 FINAL PDFDocument13 pagesBusinessfinance12 q3 Mod4 FINAL PDFJoyce Anne ManzanilloNo ratings yet

- 2A Unit 6 Working Capital SlidesDocument104 pages2A Unit 6 Working Capital SlidesZiphozonkeNo ratings yet

- FinMan-11 25Document92 pagesFinMan-11 25Jessa GalbadorNo ratings yet

- 9523strategic Financial Management K-4-BDocument18 pages9523strategic Financial Management K-4-BPratham KochharNo ratings yet

- 06 Sales Forecasting IDocument32 pages06 Sales Forecasting IMiguel Gonzalez LondoñoNo ratings yet

- User Manual For YASAIwDocument17 pagesUser Manual For YASAIwggNo ratings yet

- 05 Developing Business Strategies Using SimulationDocument18 pages05 Developing Business Strategies Using SimulationMiguel Gonzalez LondoñoNo ratings yet

- 02 Venture Financing The Basics PDFDocument12 pages02 Venture Financing The Basics PDFMiguel Gonzalez LondoñoNo ratings yet

- 03 The Business Plan PDFDocument28 pages03 The Business Plan PDFMiguel Gonzalez LondoñoNo ratings yet

- 03 The Business Plan PDFDocument28 pages03 The Business Plan PDFMiguel Gonzalez LondoñoNo ratings yet

- Financial Performance Measures by Venture Life Cycle StageDocument31 pagesFinancial Performance Measures by Venture Life Cycle StageMiguel Gonzalez LondoñoNo ratings yet

- 02 Venture Financing The Basics PDFDocument12 pages02 Venture Financing The Basics PDFMiguel Gonzalez LondoñoNo ratings yet

- Financiacion Innovacion I PDFDocument71 pagesFinanciacion Innovacion I PDFMiguel Gonzalez LondoñoNo ratings yet

- MUET@UiTM2020 - Food Poisoning - Analysis & SynthesisDocument15 pagesMUET@UiTM2020 - Food Poisoning - Analysis & SynthesisNURUL FARRAH LIEYANA BT SHAMSUL BAHARINo ratings yet

- Bharat MalaDocument29 pagesBharat MalaNavin GoyalNo ratings yet

- Family Nursing Care Plan: NAME: CASTILLO, Nina Beleen F. CHN Section: 2nu03Document3 pagesFamily Nursing Care Plan: NAME: CASTILLO, Nina Beleen F. CHN Section: 2nu03NinaNo ratings yet

- Great Mosque of Djenné - WikipediaDocument15 pagesGreat Mosque of Djenné - WikipediaRabiya AnwarNo ratings yet

- Skadden:Lexis NexisDocument7 pagesSkadden:Lexis Nexismklimo13No ratings yet

- Structure of Indian GovernmentDocument10 pagesStructure of Indian GovernmentNilesh Mistry (Nilesh Sharma)No ratings yet

- Letter Sa Mga Panel Inag FinalsDocument7 pagesLetter Sa Mga Panel Inag FinalsCHENNY BETAIZARNo ratings yet

- Form b1Document7 pagesForm b1Ahmad ZuwairisyazwanNo ratings yet

- WHO Report On COVID-19 - April 22, 2020Document14 pagesWHO Report On COVID-19 - April 22, 2020CityNewsTorontoNo ratings yet

- Desperate HousewivesDocument15 pagesDesperate HousewivesIvanka ShtyfanenkoNo ratings yet

- Microeconomics 20th Edition Mcconnell Test BankDocument25 pagesMicroeconomics 20th Edition Mcconnell Test BankMeganAguilarkpjrz100% (56)

- Similarities Between Public Finance and Private FinanceDocument18 pagesSimilarities Between Public Finance and Private FinanceMelkamu100% (2)

- Crim Pro CasesDocument71 pagesCrim Pro CasesMassabielleNo ratings yet

- Salem Steel PlantDocument69 pagesSalem Steel PlantKavuthu Mathi100% (2)

- Sri Aurobindo's Guidance on Sadhana and the MindDocument8 pagesSri Aurobindo's Guidance on Sadhana and the MindShiyama SwaminathanNo ratings yet

- Material For Upper Advanced and TOEFLDocument132 pagesMaterial For Upper Advanced and TOEFLNadia ChavezNo ratings yet

- Amended Proposition Clarifications For 1st UILS Intra Department Trial Advocacy Competition PDFDocument42 pagesAmended Proposition Clarifications For 1st UILS Intra Department Trial Advocacy Competition PDFBrijeshNo ratings yet

- Pro-Choice Violence in OntarioDocument16 pagesPro-Choice Violence in OntarioHuman Life InternationalNo ratings yet

- Understanding Students' BackgroundsDocument4 pagesUnderstanding Students' BackgroundsBright Appiagyei-BoakyeNo ratings yet

- USA2Document2 pagesUSA2Helena TrầnNo ratings yet

- E-Commerce and Consumer Goods A Strategy For Omnichannel SuccessDocument16 pagesE-Commerce and Consumer Goods A Strategy For Omnichannel SuccessAnthony Le Jr.100% (1)

- FINAL DOCUMENT (SIP) ReportDocument16 pagesFINAL DOCUMENT (SIP) ReportSairaj MudhirajNo ratings yet

- Fallacies EssayDocument1 pageFallacies EssayrahimNo ratings yet

- House of Mango Street - Han Jade NgoDocument2 pagesHouse of Mango Street - Han Jade Ngoapi-330328331No ratings yet

- 2009-05-28Document40 pages2009-05-28Southern Maryland OnlineNo ratings yet

- KLTG23: Dec - Mac 2015Document113 pagesKLTG23: Dec - Mac 2015Abdul Rahim Mohd AkirNo ratings yet

- ALL Night Long: THE Architectural Jazz OF THE Texas RangersDocument8 pagesALL Night Long: THE Architectural Jazz OF THE Texas RangersBegüm EserNo ratings yet