You might also like

- Supreme Court: Polistico Law Office For PetitionerDocument8 pagesSupreme Court: Polistico Law Office For PetitionerBryle QuimNo ratings yet

- Supreme Court Rules on Liability for Invalid Infrastructure ContractDocument12 pagesSupreme Court Rules on Liability for Invalid Infrastructure ContractYgh E SargeNo ratings yet

- Melchor Vs COADocument6 pagesMelchor Vs COAJohney Doe100% (1)

- Melchor v. COA, G.R No. 95398, August 16, 1991Document2 pagesMelchor v. COA, G.R No. 95398, August 16, 1991Carie LawyerrNo ratings yet

- COA Cannot Nullify Contract Due to Missing Witness SignatureDocument1 pageCOA Cannot Nullify Contract Due to Missing Witness SignatureSarah LeeNo ratings yet

- Melchor vs. Coa 200 Scra 704 1991Document1 pageMelchor vs. Coa 200 Scra 704 1991Syed Almendras IINo ratings yet

- Roblett Vs CA Full TextDocument4 pagesRoblett Vs CA Full TextFai MeileNo ratings yet

- G.R. No. 98355 March 2, 1994 HON. TOMAS R, OSMEÑA, Petitioner, Commission On Audit and Honorable Eufemio C. Domingo, RespondentsDocument4 pagesG.R. No. 98355 March 2, 1994 HON. TOMAS R, OSMEÑA, Petitioner, Commission On Audit and Honorable Eufemio C. Domingo, RespondentsAnonymous 91VpMbgxNo ratings yet

- En Banc G.R. No. 223762, November 07, 2017 TOMAS N. JOSON III, Petitioner, v. COMMISSION ON AUDIT, Respondent. Decision Tijam, J.Document8 pagesEn Banc G.R. No. 223762, November 07, 2017 TOMAS N. JOSON III, Petitioner, v. COMMISSION ON AUDIT, Respondent. Decision Tijam, J.Paul Angelo 黃種 武No ratings yet

- Dingcong Vs GuingonaDocument4 pagesDingcong Vs GuingonaAbigael DemdamNo ratings yet

- Joson Case RA 9184Document22 pagesJoson Case RA 9184Myra BarandaNo ratings yet

- Case 236 Osmeña V COADocument5 pagesCase 236 Osmeña V COADyna CarlosNo ratings yet

- Public Corp CasesDocument149 pagesPublic Corp CasestjstiflerNo ratings yet

- PPA General Manager Lacks Authority to Bind AgencyDocument13 pagesPPA General Manager Lacks Authority to Bind AgencyDan Andrei Salmo SadorraNo ratings yet

- COA Grave Abuse Disallowing Gov LiabilityDocument3 pagesCOA Grave Abuse Disallowing Gov LiabilitySai PastranaNo ratings yet

- Roblett Vs CADocument2 pagesRoblett Vs CAJolo Coronel100% (1)

- AiriDocument9 pagesAiriMichaella LauritoNo ratings yet

- Maritime Company of The Philippines Vs Reparations CommissionDocument15 pagesMaritime Company of The Philippines Vs Reparations Commissiononryouyuki0% (1)

- M-5 Estimation and Costing - Rakesh RDocument10 pagesM-5 Estimation and Costing - Rakesh RNidhi MehtaNo ratings yet

- Cases TaxationDocument6 pagesCases TaxationEdel VillanuevaNo ratings yet

- Gutierrez Hermanos Vs Oria HermanosDocument4 pagesGutierrez Hermanos Vs Oria HermanosleawisokaNo ratings yet

- Position Paper On Administrative Case Involving The Iloilo City Supplementary Contract Award Before The Ombudsman PDFDocument8 pagesPosition Paper On Administrative Case Involving The Iloilo City Supplementary Contract Award Before The Ombudsman PDFJacob BlackNo ratings yet

- Prohibited Contracts RulingDocument1 pageProhibited Contracts RulingKingNo ratings yet

- Quezon vs. LexberDocument2 pagesQuezon vs. LexberAlexandraSoledadNo ratings yet

- Subcontract Agreement for Sewage Treatment Plant InstallationDocument3 pagesSubcontract Agreement for Sewage Treatment Plant InstallationKrisNo ratings yet

- Mao Ni Tanan 6 Kabuok Cases Sa StatconDocument7 pagesMao Ni Tanan 6 Kabuok Cases Sa StatconMingNo ratings yet

- Position Paper On Administrative Case Involving The Iloilo City Supplementary Contract Award Before The OmbudsmanDocument8 pagesPosition Paper On Administrative Case Involving The Iloilo City Supplementary Contract Award Before The OmbudsmanManuel Mejorada100% (14)

- Singson vs. CaltexDocument7 pagesSingson vs. CaltexElephantNo ratings yet

- Republic Vs LacapDocument5 pagesRepublic Vs LacapMelo Ponce de LeonNo ratings yet

- Comelec vs. Quijano - Shorter VersionDocument2 pagesComelec vs. Quijano - Shorter VersionMatet VenturaNo ratings yet

- Allen Vs Province of TayabasDocument7 pagesAllen Vs Province of TayabasDora the ExplorerNo ratings yet

- Sargasso Construction & Dev't Corp/pick & Shovel, Inc./atlantic Erectors, Inc. (Joint Venture VS PP)Document2 pagesSargasso Construction & Dev't Corp/pick & Shovel, Inc./atlantic Erectors, Inc. (Joint Venture VS PP)Lalaine V. DelimaNo ratings yet

- Case DigestDocument7 pagesCase DigestSittie Hayah A. AmerNo ratings yet

- de Jesus Vs GuerreroDocument7 pagesde Jesus Vs GuerreroJoel G. AyonNo ratings yet

- Commission On Audit: Republic of The PhilippinesDocument4 pagesCommission On Audit: Republic of The PhilippinesGuiller C. MagsumbolNo ratings yet

- 52-Article Text-210-1-10-20190430Document10 pages52-Article Text-210-1-10-20190430Helmi NstNo ratings yet

- Active Realty & Development Corporation, Petitioner, Daroya-Quinones, RespondentsDocument6 pagesActive Realty & Development Corporation, Petitioner, Daroya-Quinones, RespondentsGH IAYAMAENo ratings yet

- COA Ruling on NPC Contract with Private LawyerDocument6 pagesCOA Ruling on NPC Contract with Private Lawyerenan_intonNo ratings yet

- City of Quezon v. LuxbergDocument14 pagesCity of Quezon v. LuxbergShilalah OpenianoNo ratings yet

- Metro Laundry Services Vs Commission Proper, Commission On Audit, and City of Manila, G.R. No. 252411, February 15, 2022Document2 pagesMetro Laundry Services Vs Commission Proper, Commission On Audit, and City of Manila, G.R. No. 252411, February 15, 2022Gi NoNo ratings yet

- 050 Rimando Vs - NetcDocument3 pages050 Rimando Vs - NetcAizaLizaNo ratings yet

- Civil Suit 487 of 2015Document13 pagesCivil Suit 487 of 2015nicole gichuhiNo ratings yet

- (G.R. No. 137798. October 4, 2000) LUCIA R. SINGSON, Petitioner, vs. CALTEX (PHILIPPINES), INC. Respondent. Decision Gonzaga-Reyes, J.Document6 pages(G.R. No. 137798. October 4, 2000) LUCIA R. SINGSON, Petitioner, vs. CALTEX (PHILIPPINES), INC. Respondent. Decision Gonzaga-Reyes, J.hernan paladNo ratings yet

- Heirs of Gaite (Digest)Document5 pagesHeirs of Gaite (Digest)Rose de DiosNo ratings yet

- Read MeDocument15 pagesRead MeSau Fen ChanNo ratings yet

- Research Re Sec 37 RA 9184Document3 pagesResearch Re Sec 37 RA 9184Gino GinoNo ratings yet

- HAL Seeks Dismissal of Gratuity AppealDocument6 pagesHAL Seeks Dismissal of Gratuity AppealHarshitha MNo ratings yet

- Legal Opinion FormatDocument2 pagesLegal Opinion FormatUPDkath100% (4)

- Pradeep Singh Pahal and Kavita Ahuja Case SummaryDocument3 pagesPradeep Singh Pahal and Kavita Ahuja Case Summarydk0895No ratings yet

- Lucia Singson vs. Caltex (Phils)Document6 pagesLucia Singson vs. Caltex (Phils)pasmoNo ratings yet

- ATO vs Inter Technical Pacific Phil: Failure to Submit Bid Form is Fatal in Govt Infrastructure BiddingDocument13 pagesATO vs Inter Technical Pacific Phil: Failure to Submit Bid Form is Fatal in Govt Infrastructure BiddingcarafloresNo ratings yet

- Munasque v. CADocument1 pageMunasque v. CACheska WeeNo ratings yet

- Singson Vs CaltexDocument5 pagesSingson Vs CaltexEmil BautistaNo ratings yet

- Legal opinion on payment of asphalting projectsDocument3 pagesLegal opinion on payment of asphalting projectsmj tirolNo ratings yet

- Supreme Court upholds validity of non-involvement clauseDocument12 pagesSupreme Court upholds validity of non-involvement clauseAndree MorañaNo ratings yet

- MANU/KE/0304/2006: K.A. Abdul Gafoor, JDocument3 pagesMANU/KE/0304/2006: K.A. Abdul Gafoor, JPranav TanwarNo ratings yet

- Chung vs. UlandayDocument20 pagesChung vs. UlandayPia Christine BungubungNo ratings yet

- Karnataka HC Arbitration 433842Document14 pagesKarnataka HC Arbitration 433842chandan patilNo ratings yet

- ALONZO, Francess Mae - Case Digest - PubCorp - Week 7Document16 pagesALONZO, Francess Mae - Case Digest - PubCorp - Week 7Francess Mae AlonzoNo ratings yet

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintFrom EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintRating: 4 out of 5 stars4/5 (1)

- Gulf Resorts v. Philippine Charter Ins.Document14 pagesGulf Resorts v. Philippine Charter Ins.MICAELA NIALANo ratings yet

- Recruitment and Placement DisputesDocument10 pagesRecruitment and Placement DisputesAtheena Marie PalomariaNo ratings yet

- 11-16 DigestDocument12 pages11-16 DigestAtheena Marie PalomariaNo ratings yet

- PHILAM INSURANCE v. Parc ChateauDocument6 pagesPHILAM INSURANCE v. Parc ChateauAtheena Marie PalomariaNo ratings yet

- Insurance Policies Valid Despite Installment Premium PaymentsDocument4 pagesInsurance Policies Valid Despite Installment Premium PaymentsRochelle Othin Odsinada MarquesesNo ratings yet

- Administration, Enforcement, VIsitorial Powers CasesDocument27 pagesAdministration, Enforcement, VIsitorial Powers CasesAtheena Marie PalomariaNo ratings yet

- Reyes vs. Almanzor Case DigestDocument1 pageReyes vs. Almanzor Case DigestAtheena Marie PalomariaNo ratings yet

- The City Attorney For Petitioners. The Solicitor General For Public RespondentDocument13 pagesThe City Attorney For Petitioners. The Solicitor General For Public RespondentAtheena Marie PalomariaNo ratings yet

- NORMA MABEZA VsDocument2 pagesNORMA MABEZA VsAtheena Marie PalomariaNo ratings yet

- North Davao Mining Corp Vs NLRCDocument6 pagesNorth Davao Mining Corp Vs NLRCAtheena Marie PalomariaNo ratings yet

- Makati Haberdashery CaseDocument2 pagesMakati Haberdashery CaseAtheena Marie PalomariaNo ratings yet

- Auroora Vs NLRCDocument7 pagesAuroora Vs NLRCAtheena Marie PalomariaNo ratings yet

- Sales CasesDocument62 pagesSales CasesAtheena Marie PalomariaNo ratings yet

- Po Yo Bi VS Republic of The PhilippinesDocument2 pagesPo Yo Bi VS Republic of The PhilippinesJon Eric G. Co100% (2)

- Ruga vs. NLRCDocument2 pagesRuga vs. NLRCAtheena Marie PalomariaNo ratings yet

- Tragedy of The CommonsDocument1 pageTragedy of The CommonsAtheena Marie PalomariaNo ratings yet

- North Davao Mining Corp Vs NLRCDocument6 pagesNorth Davao Mining Corp Vs NLRCAtheena Marie PalomariaNo ratings yet

- Fishermen are Employees and Illegally DismissedDocument2 pagesFishermen are Employees and Illegally DismissedAtheena Marie PalomariaNo ratings yet

- Fishermen are Employees and Illegally DismissedDocument2 pagesFishermen are Employees and Illegally DismissedAtheena Marie PalomariaNo ratings yet

- Red V Coconut Products, Ltd. vs. CIRDocument2 pagesRed V Coconut Products, Ltd. vs. CIRAtheena Marie Palomaria100% (3)

- G.R. No. 167614 March 24, 2009 ANTONIO M. SERRANO, Petitioner, Gallant MARITIME SERVICES, INC. and MARLOW NAVIGATION CO., INC., RespondentsDocument40 pagesG.R. No. 167614 March 24, 2009 ANTONIO M. SERRANO, Petitioner, Gallant MARITIME SERVICES, INC. and MARLOW NAVIGATION CO., INC., RespondentsAtheena Marie PalomariaNo ratings yet

- Integrated Contractor and Plumbing Works, Inc. vs. NLRC and Glen SolonDocument2 pagesIntegrated Contractor and Plumbing Works, Inc. vs. NLRC and Glen SolonAtheena Marie PalomariaNo ratings yet

- Ang Ladlad vs. ComelecDocument16 pagesAng Ladlad vs. ComelecJohanna Mae L. AutidaNo ratings yet

- Terocel Realty, Inc. vs. Leonardo MempinDocument4 pagesTerocel Realty, Inc. vs. Leonardo MempinAtheena Marie PalomariaNo ratings yet

- Human BodyDocument36 pagesHuman BodyAtheena Marie PalomariaNo ratings yet

- How Not to Advise a FoolDocument2 pagesHow Not to Advise a FoolJag UnathNo ratings yet

- SAAMER OVERSEAS PLACEMENT AGENCY, INC. vs. JOY CABILESDocument2 pagesSAAMER OVERSEAS PLACEMENT AGENCY, INC. vs. JOY CABILESAtheena Marie PalomariaNo ratings yet

- Terocel Realty, Inc. vs. Leonardo MempinDocument4 pagesTerocel Realty, Inc. vs. Leonardo MempinAtheena Marie PalomariaNo ratings yet

- People of The Philippines vs. Rico Dela PenaDocument6 pagesPeople of The Philippines vs. Rico Dela PenaAtheena Marie PalomariaNo ratings yet

- Human BodyDocument36 pagesHuman BodyAtheena Marie PalomariaNo ratings yet

- Plaintiff-Appellant vs. vs. Defendant-Appellee Delgado, Flores, Macapagal & Dizon Ross, Selph & CarrascosoDocument3 pagesPlaintiff-Appellant vs. vs. Defendant-Appellee Delgado, Flores, Macapagal & Dizon Ross, Selph & CarrascosoSiegfred G. PerezNo ratings yet

- Ignacio v. Banate (No. L-74720. August 31, 1987)Document6 pagesIgnacio v. Banate (No. L-74720. August 31, 1987)Fatzie MendozaNo ratings yet

- CIMB Savings StatementDocument2 pagesCIMB Savings StatementNoriza GhazaliNo ratings yet

- People V Desalisa PDFDocument7 pagesPeople V Desalisa PDFNico de la PazNo ratings yet

- GARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDocument10 pagesGARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDarloxNo ratings yet

- In Re: Grand Prix Fixed Lessee LLC, Case No. 10-13825, (Jointly Administered Uder Case No. 10-13800)Document3 pagesIn Re: Grand Prix Fixed Lessee LLC, Case No. 10-13825, (Jointly Administered Uder Case No. 10-13800)Chapter 11 DocketsNo ratings yet

- Investigation Report WritingDocument25 pagesInvestigation Report WritingPSSg Aniwasal, Astrid Pongod100% (1)

- EcoWorld Malaysia - Proposed Land AcquisitionDocument9 pagesEcoWorld Malaysia - Proposed Land AcquisitiondaveleyconsNo ratings yet

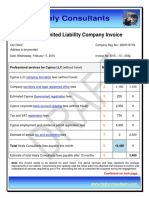

- Draft Invoice Cyprus LLC MigrationDocument7 pagesDraft Invoice Cyprus LLC MigrationShehryar KhanNo ratings yet

- Assignment 2 Answer KeyDocument2 pagesAssignment 2 Answer KeyAbdulakbar Ganzon BrigoleNo ratings yet

- Boston Bank V Manalo - : Gr. No. 158149Document2 pagesBoston Bank V Manalo - : Gr. No. 158149Anonymous C5NWrY62No ratings yet

- Overview of New Security Controls in ISO 27002 ENDocument15 pagesOverview of New Security Controls in ISO 27002 ENsotomiguelNo ratings yet

- Solicitor General v Metro Manila Authority: Ordinance Removing License Plates for Traffic Violations InvalidDocument1 pageSolicitor General v Metro Manila Authority: Ordinance Removing License Plates for Traffic Violations Invalidgeni_pearlc100% (1)

- Accountability and Public Expenditure Management in Decentralised CambodiaDocument86 pagesAccountability and Public Expenditure Management in Decentralised CambodiaSaravorn100% (1)

- 03 Arabay Vs CFIDocument3 pages03 Arabay Vs CFIJustin Andre Siguan100% (1)

- Complaint - Fairbanks v. Roller (1 June 2017) - RedactedDocument13 pagesComplaint - Fairbanks v. Roller (1 June 2017) - RedactedLaw&CrimeNo ratings yet

- Menka Jha - LinkedInDocument9 pagesMenka Jha - LinkedInVVB MULTI VENTURE FINANCENo ratings yet

- Course PlanDocument3 pagesCourse PlannurNo ratings yet

- Compel Annual Stockholders' MeetingDocument4 pagesCompel Annual Stockholders' MeetingJake MendozaNo ratings yet

- PaySlip of JanuaryDocument1 pagePaySlip of JanuaryBharat YadavNo ratings yet

- Incoming Passenger Card Australia EditableDocument2 pagesIncoming Passenger Card Australia EditableINDERPREETNo ratings yet

- Feleke Firewall Note 2023Document21 pagesFeleke Firewall Note 2023Abni booNo ratings yet

- Green v. United States, 355 U.S. 184 (1957)Document27 pagesGreen v. United States, 355 U.S. 184 (1957)Scribd Government DocsNo ratings yet

- Modules 13, 14 and 15Document11 pagesModules 13, 14 and 15George EvangelistaNo ratings yet

- Tle9agricropproduction - q1 - m9 - Observingworkplacepracticesandreportingproblemsincompletingworkforhorticulturalproduction - v3Document24 pagesTle9agricropproduction - q1 - m9 - Observingworkplacepracticesandreportingproblemsincompletingworkforhorticulturalproduction - v3Maricris Pamulaklakin AlmendrasNo ratings yet

- Assessing Business Taxes and Fees in CITYDocument11 pagesAssessing Business Taxes and Fees in CITYRio Albarico100% (1)

- Screenshot 2023-12-01 at 22.49.33Document30 pagesScreenshot 2023-12-01 at 22.49.33abualevelsNo ratings yet

- Simpsons - String PDFDocument6 pagesSimpsons - String PDFPaola RussoNo ratings yet

- Wong Keng Liang The Lizard King CaseDocument11 pagesWong Keng Liang The Lizard King CaseaishahNo ratings yet

- Improving Micro Savings Mobilization Using A Mobile AppDocument3 pagesImproving Micro Savings Mobilization Using A Mobile AppAnonymous hi0qt7uNo ratings yet