You might also like

- Computer Hardware Service Centre: Project Report ofDocument10 pagesComputer Hardware Service Centre: Project Report ofEMMANUEL TV INDIANo ratings yet

- VLL6 IAx YGo HZW PVJTZ WZDCi G0 P AQr 98 No CFBC DJ WDocument16 pagesVLL6 IAx YGo HZW PVJTZ WZDCi G0 P AQr 98 No CFBC DJ WEMMANUEL TV INDIANo ratings yet

- Computer Business Centre: Project Report ofDocument10 pagesComputer Business Centre: Project Report ofEMMANUEL TV INDIANo ratings yet

- How To InstallDocument2 pagesHow To Installmor seckNo ratings yet

- Leather Belt: Project Report ofDocument20 pagesLeather Belt: Project Report ofEMMANUEL TV INDIANo ratings yet

- Rose Cultivation: Project Report ofDocument14 pagesRose Cultivation: Project Report ofEMMANUEL TV INDIANo ratings yet

- Jeggings Manufacturing Unit: Project Report ofDocument23 pagesJeggings Manufacturing Unit: Project Report ofEMMANUEL TV INDIANo ratings yet

- Computer Training Institute: Project Report ofDocument9 pagesComputer Training Institute: Project Report ofEMMANUEL TV INDIANo ratings yet

- Non Woven Bag: Project Report ofDocument19 pagesNon Woven Bag: Project Report ofEMMANUEL TV INDIANo ratings yet

- Box Makingg PDFDocument19 pagesBox Makingg PDFEMMANUEL TV INDIANo ratings yet

- Leather Belt: Project Report ofDocument20 pagesLeather Belt: Project Report ofEMMANUEL TV INDIANo ratings yet

- Plastrof ParisDocument19 pagesPlastrof ParisEMMANUEL TV INDIANo ratings yet

- Liquid Hand Wash PDFDocument23 pagesLiquid Hand Wash PDFEMMANUEL TV INDIANo ratings yet

- Box Making PDFDocument28 pagesBox Making PDFEMMANUEL TV INDIANo ratings yet

- Liquid Hand Wash PDFDocument23 pagesLiquid Hand Wash PDFEMMANUEL TV INDIANo ratings yet

- Liquid Hand Wash PDFDocument23 pagesLiquid Hand Wash PDFEMMANUEL TV INDIANo ratings yet

- Box Makingg PDFDocument19 pagesBox Makingg PDFEMMANUEL TV INDIANo ratings yet

- Box Making PDFDocument28 pagesBox Making PDFEMMANUEL TV INDIANo ratings yet

- File Password Is 44556677Document1 pageFile Password Is 44556677EMMANUEL TV INDIANo ratings yet

- Box Makingg PDFDocument19 pagesBox Makingg PDFEMMANUEL TV INDIANo ratings yet

- Natural Mineral Water PDFDocument2 pagesNatural Mineral Water PDFPrakash PalNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Assignment 1Document2 pagesAssignment 1georgeNo ratings yet

- Angel InvestorDocument2 pagesAngel InvestorThuận Lê100% (1)

- Income Statement and Statement of Financial Position Prepared byDocument7 pagesIncome Statement and Statement of Financial Position Prepared byFakhrul IslamNo ratings yet

- Public Private PartnershipsDocument4 pagesPublic Private PartnershipsshahriarsadighiNo ratings yet

- 2020 - IMA Agreement (Directional) With Annex A PDFDocument5 pages2020 - IMA Agreement (Directional) With Annex A PDFKrisha Marie CarlosNo ratings yet

- 8 PDFDocument77 pages8 PDFHemanthThotaNo ratings yet

- Motex AssignmentDocument13 pagesMotex Assignmentmotuma dugasaNo ratings yet

- VideoDocument137 pagesVideoimidazolaNo ratings yet

- Course OtamDocument4 pagesCourse Otamkam456No ratings yet

- Ringkasan Kinerja Perusahaan TercatatDocument3 pagesRingkasan Kinerja Perusahaan TercatatDian PrasetyoNo ratings yet

- 10 Innovations and Challenges in Msme SectorDocument5 pages10 Innovations and Challenges in Msme SectorShukla SuyashNo ratings yet

- Sign-Up Form For The Direct Express Card For Benefit PaymentsDocument2 pagesSign-Up Form For The Direct Express Card For Benefit PaymentsDawn Calvin67% (3)

- Construction All RisksDocument6 pagesConstruction All RisksAzman YahayaNo ratings yet

- Powers of Corporation TableDocument2 pagesPowers of Corporation TableAna MendezNo ratings yet

- Decision Areas in Financial ManagementDocument15 pagesDecision Areas in Financial ManagementSana Moid100% (3)

- Twin Deficits HypothesisDocument3 pagesTwin Deficits HypothesisinnovatorinnovatorNo ratings yet

- Ordinance Resolution 2024Document2 pagesOrdinance Resolution 2024Weng KayNo ratings yet

- Holiday Homework Class XI Accountancy PDFDocument8 pagesHoliday Homework Class XI Accountancy PDFAlokNo ratings yet

- Chap015 Auditing Debt and Equity CapitalDocument31 pagesChap015 Auditing Debt and Equity CapitalStevia Tjioe100% (6)

- Robert Mundel & Mercus Fleming Model (IS LM BP Model) PDFDocument11 pagesRobert Mundel & Mercus Fleming Model (IS LM BP Model) PDFSukumar SarkarNo ratings yet

- The Credit Channel Is An Enhancement Mechanism For Traditional Monetary PolicyDocument2 pagesThe Credit Channel Is An Enhancement Mechanism For Traditional Monetary PolicyigrinisNo ratings yet

- DeliveryHeroSE Annual Financial Statement FinalDocument108 pagesDeliveryHeroSE Annual Financial Statement FinalimranNo ratings yet

- Recruitment and Selection Process For 1st Level Officer in Bank AlfalahDocument28 pagesRecruitment and Selection Process For 1st Level Officer in Bank AlfalahArslan Nawaz100% (1)

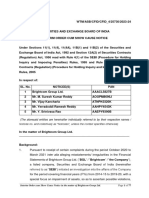

- Pension Guide: Based On Institutional Framework FOR Expediting Pension Cases Developed by Establishment DivisionDocument26 pagesPension Guide: Based On Institutional Framework FOR Expediting Pension Cases Developed by Establishment DivisionAcademy Of Commerce And Management SciencesNo ratings yet

- TA 22 Deposit Register 150222Document1 pageTA 22 Deposit Register 150222Priya DharshiniNo ratings yet

- Annual Report 2022 en Final WebsiteDocument76 pagesAnnual Report 2022 en Final WebsiteSin SeutNo ratings yet

- Why Finkulp 18.08Document7 pagesWhy Finkulp 18.08Yadav VineetNo ratings yet

- CA Inter Paper 2 All Question PapersDocument175 pagesCA Inter Paper 2 All Question PapersNivedita SharmaNo ratings yet

- Top 50 RulesDocument53 pagesTop 50 RulesShaji HakeemNo ratings yet

- ABM Fundamentals of ABM 1 Module 1 Introduction To AccountingDocument18 pagesABM Fundamentals of ABM 1 Module 1 Introduction To Accountingeva hernandez528No ratings yet