You might also like

- Globus Spirits: New Capacities Planned, Margins Continue To ExpandDocument4 pagesGlobus Spirits: New Capacities Planned, Margins Continue To ExpandHoward RoarkNo ratings yet

- ICICI Direct - Dhampur SugarDocument7 pagesICICI Direct - Dhampur SugarAJNo ratings yet

- Globus Spirits - IDirect - 200921 - EBRDocument4 pagesGlobus Spirits - IDirect - 200921 - EBREquity NestNo ratings yet

- 1.vinati Organics Initial (ICICI) (02.07.21)Document14 pages1.vinati Organics Initial (ICICI) (02.07.21)beza manojNo ratings yet

- IDirect UnitedBreweries Q4FY20Document6 pagesIDirect UnitedBreweries Q4FY20dnwekfnkfnknf skkjdbNo ratings yet

- IDirect AmaraRaja CoUpdate Feb21Document6 pagesIDirect AmaraRaja CoUpdate Feb21Romelu MartialNo ratings yet

- Saregama India: Near Term Challenges PersistDocument5 pagesSaregama India: Near Term Challenges Persistnikhil gayamNo ratings yet

- Hero Motocorp: (Herhon)Document10 pagesHero Motocorp: (Herhon)ayushNo ratings yet

- Globus SpiritsDocument5 pagesGlobus SpiritsTejesh GoudNo ratings yet

- Icici DmartDocument6 pagesIcici DmartGOUTAMNo ratings yet

- Mold-Tek Packaging - Q4FY19 - Result Update - 12062019 - 13-06-2019 - 09Document6 pagesMold-Tek Packaging - Q4FY19 - Result Update - 12062019 - 13-06-2019 - 09Ashutosh GuptaNo ratings yet

- Berger Paints India: Colourful Growth StoryDocument21 pagesBerger Paints India: Colourful Growth StoryVishnu KanthNo ratings yet

- AR Equity PDFDocument6 pagesAR Equity PDFnani reddyNo ratings yet

- Adani GasDocument5 pagesAdani Gasal.ramasamyNo ratings yet

- ICICI Direct Maruti Suzuki IndiaDocument9 pagesICICI Direct Maruti Suzuki IndiaFarah HNo ratings yet

- Mahindra & Mahindra: Strong Quarter New Launches To Drive GrowthDocument9 pagesMahindra & Mahindra: Strong Quarter New Launches To Drive Growthparchure123No ratings yet

- Apollo Tyres: Margins Surprise PositivelyDocument10 pagesApollo Tyres: Margins Surprise PositivelySanjeev ThadaniNo ratings yet

- Escorts: All-Round Optimism Bolsters Constructive ViewDocument10 pagesEscorts: All-Round Optimism Bolsters Constructive ViewasdhahdahsdjhNo ratings yet

- Apollo Tyres: Debt, Return Ratio Commentary EncouragingDocument11 pagesApollo Tyres: Debt, Return Ratio Commentary EncouragingRanjan BeheraNo ratings yet

- Vinati Organics: Newer Businesses To Drive Growth AheadDocument6 pagesVinati Organics: Newer Businesses To Drive Growth AheadtamilNo ratings yet

- Motherson Sumi: Impressive Margin Profile, Sustenance Holds KeyDocument8 pagesMotherson Sumi: Impressive Margin Profile, Sustenance Holds KeyAnurag MishraNo ratings yet

- Mangalore Refinery & Petrochem: Near Term Outlook Challenging..Document5 pagesMangalore Refinery & Petrochem: Near Term Outlook Challenging..Lekkala RameshNo ratings yet

- IDirect NRBBearings CoUpdate Jun21Document7 pagesIDirect NRBBearings CoUpdate Jun21ViralShahNo ratings yet

- Goodyear India 19-03-2021 IciciDocument6 pagesGoodyear India 19-03-2021 IcicianjugaduNo ratings yet

- IDirect NeogenChemicals ICDocument18 pagesIDirect NeogenChemicals ICPorus Saranjit SinghNo ratings yet

- ICICI Direct Balkrishna IndustriesDocument9 pagesICICI Direct Balkrishna Industriesshankar alkotiNo ratings yet

- IDirect AartiInds Q4FY21Document9 pagesIDirect AartiInds Q4FY21AkchikaNo ratings yet

- Time TechnoplastDocument8 pagesTime Technoplastagrawal.minNo ratings yet

- Pfizer LTD: Stable Growth With Consistent Margin Improvement..Document4 pagesPfizer LTD: Stable Growth With Consistent Margin Improvement..utsavmehtaNo ratings yet

- Kalpataru Power: Slower Execution Amid Pandemic DisruptionsDocument8 pagesKalpataru Power: Slower Execution Amid Pandemic DisruptionsnakilNo ratings yet

- Accelya Solutions: Revenue Trajectory Continues To ImproveDocument4 pagesAccelya Solutions: Revenue Trajectory Continues To ImprovepremNo ratings yet

- Hero Motocorp: (Herhon)Document9 pagesHero Motocorp: (Herhon)ayushNo ratings yet

- Coal India: CMP: INR234 Sputtering Production Growth Impacting VolumesDocument10 pagesCoal India: CMP: INR234 Sputtering Production Growth Impacting Volumessaran21No ratings yet

- Bodal Chemicals (BODCHE) : Expansion in Place, Volume Led Growth Ahead!Document9 pagesBodal Chemicals (BODCHE) : Expansion in Place, Volume Led Growth Ahead!P.B VeeraraghavuluNo ratings yet

- Castrol India IC May21Document17 pagesCastrol India IC May21SomendraNo ratings yet

- Filatex India: All-Time High Spreads Aid Strong Margin PerformanceDocument8 pagesFilatex India: All-Time High Spreads Aid Strong Margin PerformanceMohan MuthusamyNo ratings yet

- Asahi Songwon Colors - 3QFY18 RU - 15-02-2018 - SystematixDocument6 pagesAsahi Songwon Colors - 3QFY18 RU - 15-02-2018 - SystematixshahavNo ratings yet

- Ganesha Ecosphere Limited: To India L MitedDocument21 pagesGanesha Ecosphere Limited: To India L MitedSiddharth SehgalNo ratings yet

- Aarti Industries - Q1FY20 - Result Update - Axis DirectDocument6 pagesAarti Industries - Q1FY20 - Result Update - Axis DirectdarshanmaldeNo ratings yet

- IDirect IEX Q4FY21Document5 pagesIDirect IEX Q4FY21SushilNo ratings yet

- APL Apollo Tubes - Q1FY20 - Result Update - 16!09!2019 - 16Document6 pagesAPL Apollo Tubes - Q1FY20 - Result Update - 16!09!2019 - 16Akshat MehtaNo ratings yet

- IDirect UnitedSpirits Q4FY21Document6 pagesIDirect UnitedSpirits Q4FY21Ranjith ChackoNo ratings yet

- Huhtamaki - CU-IDirect-Mar 3, 2022Document4 pagesHuhtamaki - CU-IDirect-Mar 3, 2022rajesh katareNo ratings yet

- Jubilant Q1FY21 ResultsDocument9 pagesJubilant Q1FY21 ResultsDeepak SharmaNo ratings yet

- Sugar Sector by Icici DirectDocument24 pagesSugar Sector by Icici DirectpradeepthiteNo ratings yet

- Man Industries LTD.: CMP Rs.58 (2.0X Fy22E P/E) Not RatedDocument5 pagesMan Industries LTD.: CMP Rs.58 (2.0X Fy22E P/E) Not RatedshahavNo ratings yet

- Vinati Organics LTD: Growth To Pick-Up..Document5 pagesVinati Organics LTD: Growth To Pick-Up..Bhaveek OstwalNo ratings yet

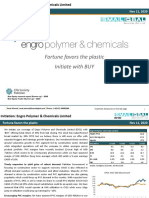

- EPCL - Fortune Favors The Plastic-3Document14 pagesEPCL - Fortune Favors The Plastic-3Fawad SaleemNo ratings yet

- Loesche - VRM Vs Ball MillDocument6 pagesLoesche - VRM Vs Ball MillVipin GoelNo ratings yet

- Ciptadana Sekuritas AALI - 1H20 Earnings Beat ExpectationDocument6 pagesCiptadana Sekuritas AALI - 1H20 Earnings Beat ExpectationHamba AllahNo ratings yet

- IDirect RallisInd CoUpdate Apr17Document4 pagesIDirect RallisInd CoUpdate Apr17saran21No ratings yet

- Equirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja ExportsDocument41 pagesEquirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja Exportsrchawdhry123100% (2)

- Blue Dart Express (NOT RATED) - BOBCAPS SecDocument3 pagesBlue Dart Express (NOT RATED) - BOBCAPS SecdarshanmaldeNo ratings yet

- Time Technoplast: New Order Win Paints Good Picture For FY22EDocument6 pagesTime Technoplast: New Order Win Paints Good Picture For FY22EVipul Braj BhartiaNo ratings yet

- Sheela Foam: Newer Long-Term Opportunities Are (Likely) Opening UpDocument6 pagesSheela Foam: Newer Long-Term Opportunities Are (Likely) Opening UpshahavNo ratings yet

- Himadri Chemical Research ReportDocument5 pagesHimadri Chemical Research ReportADNo ratings yet

- Aarti Industries - 1QFY19 RU - KR ChokseyDocument7 pagesAarti Industries - 1QFY19 RU - KR ChokseydarshanmaldeNo ratings yet

- Abbott India: FY20 Performance Reflects Strength of Power BrandsDocument5 pagesAbbott India: FY20 Performance Reflects Strength of Power BrandspremNo ratings yet

- Sandhar Technologies Profit Set To More Than Double Over FY18-20EDocument12 pagesSandhar Technologies Profit Set To More Than Double Over FY18-20Eharsh_2961No ratings yet

- RESOLVED THAT Pursuant To The Provisions of Sections 23 (1) (B), 42, 55, 62 (1) (C)Document40 pagesRESOLVED THAT Pursuant To The Provisions of Sections 23 (1) (B), 42, 55, 62 (1) (C)Debjit AdakNo ratings yet

- Bfsi - Icici Direct (Su - Oct 2020)Document14 pagesBfsi - Icici Direct (Su - Oct 2020)Debjit AdakNo ratings yet

- India Banks: EquitiesDocument42 pagesIndia Banks: EquitiesDebjit AdakNo ratings yet

- Indian Banks (Cracking Code 7.18 in Depth Analysis of Annual Reports) 20181109Document188 pagesIndian Banks (Cracking Code 7.18 in Depth Analysis of Annual Reports) 20181109Debjit AdakNo ratings yet

- Indian Banking - Sector Report - 15-07-2021 - SystematixDocument153 pagesIndian Banking - Sector Report - 15-07-2021 - SystematixDebjit AdakNo ratings yet

- Ethanol A Renaissance For Sugar Industry in India: Ravi GuptaDocument31 pagesEthanol A Renaissance For Sugar Industry in India: Ravi GuptaDebjit AdakNo ratings yet

- Happiest Minds LTD IPO: Reason For Subscribing To The IPODocument3 pagesHappiest Minds LTD IPO: Reason For Subscribing To The IPODebjit AdakNo ratings yet

- Paramount Cables Magazine Writeup Dec15Document3 pagesParamount Cables Magazine Writeup Dec15Debjit AdakNo ratings yet

- Call For Research Projects: Sector-29, Gandhinagar, Gujarat-382030Document17 pagesCall For Research Projects: Sector-29, Gandhinagar, Gujarat-382030Debjit AdakNo ratings yet

- HindalcoLimited PDFDocument64 pagesHindalcoLimited PDFDebjit AdakNo ratings yet

- Clarity On Product SharingDocument4 pagesClarity On Product SharingDebjit AdakNo ratings yet

- Weekly Newsletter 20 JuneDocument6 pagesWeekly Newsletter 20 JuneDebjit AdakNo ratings yet

- Oil & Gas - Hike ImpactDocument7 pagesOil & Gas - Hike ImpactDebjit AdakNo ratings yet

- Handout 1Document13 pagesHandout 1Krisha ErikaNo ratings yet

- The Keynesian System II Money, Interest, and IncomeDocument28 pagesThe Keynesian System II Money, Interest, and IncomeVenkatesh Venu GopalNo ratings yet

- BUS 430 Syllabus Fall 2018Document7 pagesBUS 430 Syllabus Fall 2018rickNo ratings yet

- Dmart JPMorganDocument50 pagesDmart JPMorganRavi KiranNo ratings yet

- Financial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMDocument27 pagesFinancial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMMehmet Isbilen100% (1)

- International Financial Management PPT Chap 1Document26 pagesInternational Financial Management PPT Chap 1serge folegweNo ratings yet

- The 2020 Story: Ceramic TilesDocument44 pagesThe 2020 Story: Ceramic TilesArchit SarafNo ratings yet

- Nepalese Film Industries - EssayDocument4 pagesNepalese Film Industries - EssayRex ShresthaNo ratings yet

- Strategy AssignmentDocument17 pagesStrategy AssignmentprasanthkurupNo ratings yet

- MT-760 Deut81326542195Document3 pagesMT-760 Deut81326542195reza younesy100% (3)

- Nestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesDocument39 pagesNestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesFarah NazNo ratings yet

- 2011 UBS Rogue Trader Scandal - Wikipedia-1Document30 pages2011 UBS Rogue Trader Scandal - Wikipedia-1RadityaNo ratings yet

- CH 3 Bus Envt Hsstimes SlideDocument63 pagesCH 3 Bus Envt Hsstimes Slidedhaanya goelNo ratings yet

- Bank (Final)Document25 pagesBank (Final)MishuNo ratings yet

- Swap PDF!!!!!Document24 pagesSwap PDF!!!!!Dylan LeeNo ratings yet

- Exercise No.4 Bus. Co.Document56 pagesExercise No.4 Bus. Co.Jeane Mae BooNo ratings yet

- Technical IndicatorsDocument54 pagesTechnical IndicatorsRavee MishraNo ratings yet

- Order in The Matter of Disc Assets Lead India LTDDocument25 pagesOrder in The Matter of Disc Assets Lead India LTDShyam SunderNo ratings yet

- CHA Participant Reference GuideDocument152 pagesCHA Participant Reference GuideMegNo ratings yet

- (Compare Us) Reverse Piercing of The Corporate Veil - A Straightforward Path To Justice by Nicholas AllenDocument16 pages(Compare Us) Reverse Piercing of The Corporate Veil - A Straightforward Path To Justice by Nicholas AllenNicole LimNo ratings yet

- Maskeliya Plantations PLC and Kahawatta Plantations PLC (1199)Document22 pagesMaskeliya Plantations PLC and Kahawatta Plantations PLC (1199)Bajalock VirusNo ratings yet

- Ex 2 5Document5 pagesEx 2 5andrechrstian18No ratings yet

- TBE Tutorial Slide - Part A CDocument380 pagesTBE Tutorial Slide - Part A CSyed Isa100% (1)

- Data Analysis and InterpretationDocument12 pagesData Analysis and Interpretationsaimhatre1122004No ratings yet

- Tutorial Questions FinDocument16 pagesTutorial Questions FinNhu Nguyen HoangNo ratings yet

- Vizag-Chennai Industrial Corridor - Full ReportDocument388 pagesVizag-Chennai Industrial Corridor - Full ReportPrasad GogineniNo ratings yet

- UntitledDocument6 pagesUntitledMuhammad AbdullahNo ratings yet

- Financial Ratio Analysis FormulasDocument4 pagesFinancial Ratio Analysis FormulasVaishali Jhaveri100% (1)

- Final Exam IamDocument10 pagesFinal Exam IamAhmed ZEMZEMNo ratings yet

- Building Customer RelationshipDocument9 pagesBuilding Customer RelationshipDon Mario100% (1)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsFrom EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsRating: 4.5 out of 5 stars4.5/5 (386)

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessFrom EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessRating: 5 out of 5 stars5/5 (456)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesFrom EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesRating: 5 out of 5 stars5/5 (1636)

- Summary of 12 Rules for Life: An Antidote to ChaosFrom EverandSummary of 12 Rules for Life: An Antidote to ChaosRating: 4.5 out of 5 stars4.5/5 (294)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaFrom EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaRating: 4.5 out of 5 stars4.5/5 (266)

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessFrom EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessRating: 4.5 out of 5 stars4.5/5 (328)

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindFrom EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindRating: 4.5 out of 5 stars4.5/5 (57)

- Summary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityFrom EverandSummary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityNo ratings yet

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageFrom EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageRating: 4.5 out of 5 stars4.5/5 (329)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessFrom EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNo ratings yet

- Summary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsFrom EverandSummary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsNo ratings yet

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesFrom EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesRating: 4.5 out of 5 stars4.5/5 (274)

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsFrom EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsRating: 4.5 out of 5 stars4.5/5 (709)

- Summary of The Algebra of Wealth: A Simple Formula for Financial SecurityFrom EverandSummary of The Algebra of Wealth: A Simple Formula for Financial SecurityRating: 4 out of 5 stars4/5 (1)

- Extreme Ownership by Jocko Willink and Leif Babin - Book Summary: How U.S. Navy SEALS Lead And WinFrom EverandExtreme Ownership by Jocko Willink and Leif Babin - Book Summary: How U.S. Navy SEALS Lead And WinRating: 4.5 out of 5 stars4.5/5 (75)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryFrom EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryRating: 5 out of 5 stars5/5 (557)

- Chaos: Charles Manson, the CIA, and the Secret History of the Sixties by Tom O'Neill: Conversation StartersFrom EverandChaos: Charles Manson, the CIA, and the Secret History of the Sixties by Tom O'Neill: Conversation StartersRating: 2.5 out of 5 stars2.5/5 (3)

- Summary of Atomic Habits by James ClearFrom EverandSummary of Atomic Habits by James ClearRating: 5 out of 5 stars5/5 (170)

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningFrom EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningRating: 4.5 out of 5 stars4.5/5 (55)

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeFrom EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeRating: 4.5 out of 5 stars4.5/5 (128)

- Summary of Nuclear War by Annie Jacobsen: A ScenarioFrom EverandSummary of Nuclear War by Annie Jacobsen: A ScenarioRating: 4 out of 5 stars4/5 (1)

- Summary of Eat to Beat Disease by Dr. William LiFrom EverandSummary of Eat to Beat Disease by Dr. William LiRating: 5 out of 5 stars5/5 (52)

- Summary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursFrom EverandSummary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursNo ratings yet

- The Effective Executive by Peter Drucker - Book Summary: The Definitive Guide to Getting the Right Things DoneFrom EverandThe Effective Executive by Peter Drucker - Book Summary: The Definitive Guide to Getting the Right Things DoneRating: 4.5 out of 5 stars4.5/5 (19)

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessFrom EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessRating: 4.5 out of 5 stars4.5/5 (188)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingFrom EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingRating: 4.5 out of 5 stars4.5/5 (114)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsFrom EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsNo ratings yet

- Summary of "Measure What Matters" by John Doerr: How Google, Bono, and the Gates Foundation Rock the World with OKRs — Finish Entire Book in 15 MinutesFrom EverandSummary of "Measure What Matters" by John Doerr: How Google, Bono, and the Gates Foundation Rock the World with OKRs — Finish Entire Book in 15 MinutesRating: 4.5 out of 5 stars4.5/5 (62)