You might also like

- Ing Banking Vs Cir DigestDocument2 pagesIng Banking Vs Cir DigestJuan AntonioNo ratings yet

- CIR Vs Phil Aluminum WheelsDocument6 pagesCIR Vs Phil Aluminum WheelsCherry Jean RomanoNo ratings yet

- People Vs Carlos, 47 Phil 626Document5 pagesPeople Vs Carlos, 47 Phil 626flornatsNo ratings yet

- CTA upholds dismissal of VAT refund claimDocument11 pagesCTA upholds dismissal of VAT refund claimChennieNo ratings yet

- BDO V RepublicDocument2 pagesBDO V RepublicallisonNo ratings yet

- F. CIR vs. Solidbank Corp., G.R. No. 148191, Nov. 25, 2003Document3 pagesF. CIR vs. Solidbank Corp., G.R. No. 148191, Nov. 25, 2003Rhenee Rose Reas SugboNo ratings yet

- CBK Power Company Limited Vs CirDocument6 pagesCBK Power Company Limited Vs CirAnonymous VtsflLix1No ratings yet

- C. Bloomberry Resorts and Hotels Inc. vs. Bureau of Internal RevenueDocument2 pagesC. Bloomberry Resorts and Hotels Inc. vs. Bureau of Internal RevenueJoieNo ratings yet

- Gatchalian vs. DelimDocument5 pagesGatchalian vs. DelimYong NazNo ratings yet

- CIR upholds taxability of gov't employee compensationDocument3 pagesCIR upholds taxability of gov't employee compensationZachary SiayngcoNo ratings yet

- People vs. Yatco. Etc., Et Al.Document8 pagesPeople vs. Yatco. Etc., Et Al.Gertrude PillenaNo ratings yet

- Arrow Transport Corp. vs. BOTDocument9 pagesArrow Transport Corp. vs. BOTAyra ArcillaNo ratings yet

- Final income tax rates for individuals and corporationsDocument4 pagesFinal income tax rates for individuals and corporationsJulie Mae Caling MalitNo ratings yet

- CPAR B94 TAX Final PB Exam - QuestionsDocument14 pagesCPAR B94 TAX Final PB Exam - QuestionsSilver LilyNo ratings yet

- Doctrinal Digest:: Cir Vs Bpi G.R. No. 147375, June 26, 2006Document10 pagesDoctrinal Digest:: Cir Vs Bpi G.R. No. 147375, June 26, 2006JMANo ratings yet

- GCL Retirement Plan Tax RefundDocument6 pagesGCL Retirement Plan Tax RefundLord AumarNo ratings yet

- ASIA TRUST DEVELOPMENT BANK, INC Vs CIRDocument2 pagesASIA TRUST DEVELOPMENT BANK, INC Vs CIRPaolo NazarenoNo ratings yet

- Mitsubishi Corporation-Manila Branch, Petitioner, vs. Commissioner of Internal REVENUE, RespondentDocument5 pagesMitsubishi Corporation-Manila Branch, Petitioner, vs. Commissioner of Internal REVENUE, RespondentevilsageNo ratings yet

- Mobil Philippines v. City Treasurer of Makati 1.business Tax v. Income TaxDocument4 pagesMobil Philippines v. City Treasurer of Makati 1.business Tax v. Income TaxFloyd MagoNo ratings yet

- CIR v. AcesiteDocument2 pagesCIR v. AcesiteATRNo ratings yet

- Intramuros Administration vs. Offshore Construction - 857 SCRA (2017)Document7 pagesIntramuros Administration vs. Offshore Construction - 857 SCRA (2017)Kathleen KindipanNo ratings yet

- Villanueva Vs BalaguerDocument13 pagesVillanueva Vs BalaguerJani MisterioNo ratings yet

- Commissioner v. United Cadiz Sugar Farmers Assoc Multi-Purpose CooperativeDocument7 pagesCommissioner v. United Cadiz Sugar Farmers Assoc Multi-Purpose CooperativeKit FloresNo ratings yet

- CIR Vs ST Luke S Medical CenterDocument6 pagesCIR Vs ST Luke S Medical CenterOlan Dave LachicaNo ratings yet

- Cir v. Primetown (Manner of Computing Time)Document2 pagesCir v. Primetown (Manner of Computing Time)michikoNo ratings yet

- CIR v. PNB ExceptionDocument3 pagesCIR v. PNB ExceptionAngelique Padilla UgayNo ratings yet

- SC rules RA 9504 exemptions apply for full 2008Document38 pagesSC rules RA 9504 exemptions apply for full 2008Darrel John SombilonNo ratings yet

- Abra Valley Inc. vs. Judge AquinoDocument3 pagesAbra Valley Inc. vs. Judge AquinoShai F Velasquez-NogoyNo ratings yet

- Samar-1 Electric Coop. v. CirDocument1 pageSamar-1 Electric Coop. v. CirLoNo ratings yet

- DIGEST - FISHWEALTH CANNING CORPORATION Vs CIRDocument1 pageDIGEST - FISHWEALTH CANNING CORPORATION Vs CIRArthur Sy100% (1)

- Duty Free vs. COA: Government Employees Subject To The SSL (Salary Standardization Law) PTA, A Government-Owned andDocument1 pageDuty Free vs. COA: Government Employees Subject To The SSL (Salary Standardization Law) PTA, A Government-Owned andAnonymous MikI28PkJc100% (1)

- CIR v. P&G Philippine tax credit deniedDocument2 pagesCIR v. P&G Philippine tax credit deniedNaomi QuimpoNo ratings yet

- Court Upholds Tax Deductions But Limits Professional FeesDocument3 pagesCourt Upholds Tax Deductions But Limits Professional Feesjleo1No ratings yet

- P&G Phils Can Claim Tax RefundDocument3 pagesP&G Phils Can Claim Tax RefundKarl MinglanaNo ratings yet

- Association of International Shipping Lines, Inc. vs. Secretary of Finance, GR No. 222239 Dated January 15, 2020 PDFDocument24 pagesAssociation of International Shipping Lines, Inc. vs. Secretary of Finance, GR No. 222239 Dated January 15, 2020 PDFAbbey Agno PerezNo ratings yet

- CIR v. First Express PawnshopDocument1 pageCIR v. First Express PawnshopAnneNo ratings yet

- 11 Maceda vs. Macaraig, JRDocument35 pages11 Maceda vs. Macaraig, JRshlm bNo ratings yet

- 1.2 CIR V Aichi Forging Company of Asia, Inc.Document11 pages1.2 CIR V Aichi Forging Company of Asia, Inc.Gloria Diana DulnuanNo ratings yet

- Delpher Trades Corp. v. Intermediate Appellate CourtDocument10 pagesDelpher Trades Corp. v. Intermediate Appellate CourtKTNo ratings yet

- RCBC Vs CIRDocument2 pagesRCBC Vs CIRAnneNo ratings yet

- In Re Atty Bernardo ZialcitaDocument3 pagesIn Re Atty Bernardo ZialcitaMCNo ratings yet

- Carlos V Mindoro SugarDocument2 pagesCarlos V Mindoro SugarKristine GarciaNo ratings yet

- Evidence Sept 19Document18 pagesEvidence Sept 19JV DeeNo ratings yet

- PNOC vs. Court of Appeals upholds CTA review of tax compromiseDocument2 pagesPNOC vs. Court of Appeals upholds CTA review of tax compromisejohn vidadNo ratings yet

- Howard National Bank v. WilsonDocument9 pagesHoward National Bank v. WilsonPia GNo ratings yet

- Fort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDocument28 pagesFort Bonifacio Development Corporation vs. Commissioner of Internal RevenueAriel AbisNo ratings yet

- DigestDocument2 pagesDigestkarenNo ratings yet

- Shell Oil Workers' v. Shell Company of The PhilippinesDocument16 pagesShell Oil Workers' v. Shell Company of The PhilippinesAnisah AquilaNo ratings yet

- Right to Repurchase PropertyDocument4 pagesRight to Repurchase PropertyXsche XscheNo ratings yet

- People Vs TanDocument2 pagesPeople Vs TanJulian DubaNo ratings yet

- Abs-Cbn Vs Philippine Multi-Media SystemDocument14 pagesAbs-Cbn Vs Philippine Multi-Media SystemAnonymous KvztB3No ratings yet

- Mendez Vs People 726 SCRA 203 2014Document1 pageMendez Vs People 726 SCRA 203 2014Anonymous MikI28PkJcNo ratings yet

- Republic V Razon TAX DigestDocument3 pagesRepublic V Razon TAX DigestZainalee DawnNo ratings yet

- 12 CIR vs. Phoenix (GR No. L-19727, May 20, 1965)Document13 pages12 CIR vs. Phoenix (GR No. L-19727, May 20, 1965)Alfred GarciaNo ratings yet

- NLRC Ruling on Dismissal UpheldDocument3 pagesNLRC Ruling on Dismissal UpheldHans LazaroNo ratings yet

- CIR Vs Aluminum WheelsDocument3 pagesCIR Vs Aluminum WheelsJenifferRimandoNo ratings yet

- Carpio, JDocument4 pagesCarpio, JKennethAnthonyMagdamitNo ratings yet

- Escape Taxation with Tax AmnestyDocument7 pagesEscape Taxation with Tax AmnestyJeunaj LardizabalNo ratings yet

- Cir V Phil Aluminum WheelsDocument2 pagesCir V Phil Aluminum WheelsKia BiNo ratings yet

- Case 59 CS Garments Vs CirDocument3 pagesCase 59 CS Garments Vs CirJulian Guevarra0% (1)

- Reflection On Sumilao CaseDocument3 pagesReflection On Sumilao CaseGyrsyl Jaisa GuerreroNo ratings yet

- Reflection On Sumilao CaseDocument3 pagesReflection On Sumilao CaseGyrsyl Jaisa GuerreroNo ratings yet

- Taxation I Case Digest Compilation: (Third Division) Reason For Delay: As A Consequence of The Division of TheDocument2 pagesTaxation I Case Digest Compilation: (Third Division) Reason For Delay: As A Consequence of The Division of TheGyrsyl Jaisa GuerreroNo ratings yet

- Sumilao CaseDocument4 pagesSumilao CaseGyrsyl Jaisa GuerreroNo ratings yet

- Ros V DENRDocument3 pagesRos V DENRGyrsyl Jaisa GuerreroNo ratings yet

- The Boons and Banes of New Normal in The Field of LawDocument2 pagesThe Boons and Banes of New Normal in The Field of LawGyrsyl Jaisa GuerreroNo ratings yet

- Taxation Case Digest on Tax EvasionDocument3 pagesTaxation Case Digest on Tax EvasionGyrsyl Jaisa GuerreroNo ratings yet

- Villanueva Vs IloiloDocument3 pagesVillanueva Vs IloiloGyrsyl Jaisa GuerreroNo ratings yet

- Angeles University Foundation Vs AngelesDocument3 pagesAngeles University Foundation Vs AngelesGyrsyl Jaisa GuerreroNo ratings yet

- Villanueva Vs IloiloDocument3 pagesVillanueva Vs IloiloGyrsyl Jaisa GuerreroNo ratings yet

- Resins, Inc. v. Auditor GeneralDocument1 pageResins, Inc. v. Auditor GeneralGyrsyl Jaisa GuerreroNo ratings yet

- Taxation I Case Digest Compilation: (Third Division) Reason For Delay: As A Consequence of The Division of TheDocument2 pagesTaxation I Case Digest Compilation: (Third Division) Reason For Delay: As A Consequence of The Division of TheGyrsyl Jaisa GuerreroNo ratings yet

- Asturias Sugar Central V CommissionerDocument2 pagesAsturias Sugar Central V CommissionerGyrsyl Jaisa GuerreroNo ratings yet

- Angeles University Foundation Vs AngelesDocument3 pagesAngeles University Foundation Vs AngelesGyrsyl Jaisa GuerreroNo ratings yet

- Gutierrez vs. CIR 1957: Taxation I Case Digest CompilationDocument2 pagesGutierrez vs. CIR 1957: Taxation I Case Digest CompilationGyrsyl Jaisa GuerreroNo ratings yet

- CIR v. Tours Specialist Inc.Document2 pagesCIR v. Tours Specialist Inc.Gyrsyl Jaisa GuerreroNo ratings yet

- Villanueva Vs IloiloDocument3 pagesVillanueva Vs IloiloGyrsyl Jaisa GuerreroNo ratings yet

- (First Division) : Commissioner v. Kiener Co. Ltd. 1975Document2 pages(First Division) : Commissioner v. Kiener Co. Ltd. 1975Gyrsyl Jaisa GuerreroNo ratings yet

- Rule 129 - METROBANK v. MIRANDADocument7 pagesRule 129 - METROBANK v. MIRANDAGyrsyl Jaisa GuerreroNo ratings yet

- Asturias Sugar Central V CommissionerDocument2 pagesAsturias Sugar Central V CommissionerGyrsyl Jaisa GuerreroNo ratings yet

- Gutierrez vs. CIR 1957: Taxation I Case Digest CompilationDocument2 pagesGutierrez vs. CIR 1957: Taxation I Case Digest CompilationGyrsyl Jaisa GuerreroNo ratings yet

- Philippine Obligations and Contracts Case DigestDocument1 pagePhilippine Obligations and Contracts Case DigestGyrsyl Jaisa GuerreroNo ratings yet

- Tankeh Vs DBPDocument2 pagesTankeh Vs DBPGyrsyl Jaisa GuerreroNo ratings yet

- Daily plastic bottle waste by grade at SNNHSDocument3 pagesDaily plastic bottle waste by grade at SNNHSGyrsyl Jaisa GuerreroNo ratings yet

- Chapter 7: Voidable ContractsDocument2 pagesChapter 7: Voidable ContractsGyrsyl Jaisa GuerreroNo ratings yet

- Gaisano Cagayan, Inc vs. Insurance Company of North America-2006Document5 pagesGaisano Cagayan, Inc vs. Insurance Company of North America-2006JennyAlogBignayanNo ratings yet

- Rule 129 - METROBANK v. MIRANDADocument7 pagesRule 129 - METROBANK v. MIRANDAGyrsyl Jaisa GuerreroNo ratings yet

- People Vs Clemente Casta y CarolinoDocument5 pagesPeople Vs Clemente Casta y CarolinoGyrsyl Jaisa GuerreroNo ratings yet

- Galman V PamaranDocument4 pagesGalman V PamaranGyrsyl Jaisa GuerreroNo ratings yet

- Meaning and Significance of Fiscal DeficitDocument4 pagesMeaning and Significance of Fiscal DeficitBhaskar AroraNo ratings yet

- Valued Added Tax Problems SolvingDocument3 pagesValued Added Tax Problems SolvingLouiseNo ratings yet

- Bitumen Prices Wef 01-02-11Document1 pageBitumen Prices Wef 01-02-11Vizag RoadsNo ratings yet

- Sample Sanction OrderDocument2 pagesSample Sanction OrderNayan Vankar100% (1)

- Reen LawnsDocument8 pagesReen LawnsAshish BhallaNo ratings yet

- Sohrab Bararia: Classification of Solar Power-Based Projects Under GST - An Unsettled DisputeDocument3 pagesSohrab Bararia: Classification of Solar Power-Based Projects Under GST - An Unsettled Disputeabc defNo ratings yet

- National Power Corporation V Province of Lanao Del NorteDocument2 pagesNational Power Corporation V Province of Lanao Del NorteMae Clare D. BendoNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Prem KumarNo ratings yet

- Gmail - Pearson VUE Confirmation of PaymentDocument2 pagesGmail - Pearson VUE Confirmation of PaymentShahab IntezariNo ratings yet

- DocScanner 26 Apr 2022 9 58 AMDocument82 pagesDocScanner 26 Apr 2022 9 58 AMSWAPNIL JADHAVNo ratings yet

- PIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityDocument1 pagePIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityphillipNo ratings yet

- Taxation TSN 3 Exam Coverage SummaryDocument33 pagesTaxation TSN 3 Exam Coverage SummaryPearl Angeli Quisido CanadaNo ratings yet

- Press Release Template 01Document2 pagesPress Release Template 01mkb07No ratings yet

- Pistons Company adjusting entriesDocument2 pagesPistons Company adjusting entriesjhobsNo ratings yet

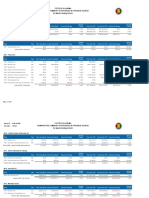

- Republic of The Philippines Court of Tax Appeals Quezon City First DivisionDocument79 pagesRepublic of The Philippines Court of Tax Appeals Quezon City First DivisionYna YnaNo ratings yet

- Taxation Law ReviewerDocument6 pagesTaxation Law ReviewerAlex RabanesNo ratings yet

- Inter Tech 3Document3 pagesInter Tech 3Harsh DiwakerNo ratings yet

- MicrosoftDocument2 pagesMicrosoftKrisi MartinezNo ratings yet

- Chapter 6 24Document5 pagesChapter 6 24MCNo ratings yet

- FY 2022 Revenue TotalsDocument296 pagesFY 2022 Revenue TotalsCaleb TaylorNo ratings yet

- GR NO. 144707, July 2004: People of The Philippines, Petitioner, VsDocument3 pagesGR NO. 144707, July 2004: People of The Philippines, Petitioner, VsmaresNo ratings yet

- 6 RR 05-99 PDFDocument5 pages6 RR 05-99 PDFbiklatNo ratings yet

- Appendix 24 - Qrror - Far 5Document1 pageAppendix 24 - Qrror - Far 5pdmu regionixNo ratings yet

- Activity Sheets in Fundamentals of Accountanc2Document5 pagesActivity Sheets in Fundamentals of Accountanc2Irish NicolasNo ratings yet

- InvoiceDocument1 pageInvoiceVeerappan MuthuramanNo ratings yet

- Payment of Bonus Form A B C and DDocument13 pagesPayment of Bonus Form A B C and DAmarjeet singhNo ratings yet

- ITDocument4 pagesITMahesh KumarNo ratings yet

- 1-CIR Vs General Foods, Inc. - GR NO. 143672Document1 page1-CIR Vs General Foods, Inc. - GR NO. 143672Jason BUENANo ratings yet

- Lasa Haldwani Revenue Officer Resume 2023 01 18 123335Document2 pagesLasa Haldwani Revenue Officer Resume 2023 01 18 123335lasa haldwaniNo ratings yet

- InvoiceDocument1 pageInvoicedhaval100% (1)