You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- 2023 CFA L2 Book 2 FRA - CI-2Document100 pages2023 CFA L2 Book 2 FRA - CI-2PR100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Name:: Account Holder: Opening Balance 0.00 EURDocument1 pageName:: Account Holder: Opening Balance 0.00 EUR13KARAT0% (1)

- Business 682 Debate Outline Guidelines and ExampleDocument5 pagesBusiness 682 Debate Outline Guidelines and ExampleZainab AbidNo ratings yet

- Class - Participation - BUS - 682.03 - Summer17Document6 pagesClass - Participation - BUS - 682.03 - Summer17Zainab AbidNo ratings yet

- 1 Contact Information: San Francisco State University (Sfsu) Fin 350: Business Finance SUMMER 2017Document12 pages1 Contact Information: San Francisco State University (Sfsu) Fin 350: Business Finance SUMMER 2017Zainab AbidNo ratings yet

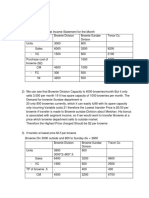

- Brownie Division Brownie Sundae Division Trevor CoDocument2 pagesBrownie Division Brownie Sundae Division Trevor CoZainab AbidNo ratings yet

- Problems Partnership Dissolution and LiquidationDocument5 pagesProblems Partnership Dissolution and LiquidationNick ivan AlvaresNo ratings yet

- Banking Maths ProjectDocument16 pagesBanking Maths ProjectAakash Sarkar60% (5)

- 138 N I Act NoticeDocument2 pages138 N I Act NoticeharshalaNo ratings yet

- Financial Ratio Analysis GuideDocument6 pagesFinancial Ratio Analysis GuideJuan Pascual CosareNo ratings yet

- From The Following Particulars Compute Gross Annual Value MRV: 18000 FRV: 21000 ARV:36000 SRV: 24000 Urr (In MonthsDocument5 pagesFrom The Following Particulars Compute Gross Annual Value MRV: 18000 FRV: 21000 ARV:36000 SRV: 24000 Urr (In Monthsrathison neonNo ratings yet

- PRODUCT DISCLOSURE SHEET (Islamic Mortgage) : 1. What Is This Product About?Document12 pagesPRODUCT DISCLOSURE SHEET (Islamic Mortgage) : 1. What Is This Product About?Azamuddin JasrelNo ratings yet

- The Historical Development of The International Financial Market From Bretton WoodsDocument28 pagesThe Historical Development of The International Financial Market From Bretton WoodsNancy Ruang-aram100% (1)

- Banking Project Work by Rishav KumarDocument22 pagesBanking Project Work by Rishav KumarRishav KumarNo ratings yet

- Barclay Case StudyDocument8 pagesBarclay Case StudySujit S NairNo ratings yet

- INVESTMENT FinalDocument40 pagesINVESTMENT FinalADNANE OULKHAJNo ratings yet

- Tutorial 6Document4 pagesTutorial 6Jian Zhi TehNo ratings yet

- Taxbanter Special Topic MaterialsDocument84 pagesTaxbanter Special Topic MaterialsJessica YuNo ratings yet

- Business Finance: Grade 12 Senior High SchoolDocument16 pagesBusiness Finance: Grade 12 Senior High SchoolPaula RealcoNo ratings yet

- Robert Keohane "After Hegemony"Document17 pagesRobert Keohane "After Hegemony"Сілвестер НосенкоNo ratings yet

- What Is An Islamic Bank? How Different Is It From A Conventional Bank?Document4 pagesWhat Is An Islamic Bank? How Different Is It From A Conventional Bank?LeeyaRazakNo ratings yet

- Ch06 JeterDocument26 pagesCh06 JeterLydia WulandariNo ratings yet

- Day Trading 101Document55 pagesDay Trading 101Heisen LukeNo ratings yet

- Muamalaat, The Alternative To The Riba System ExistsDocument40 pagesMuamalaat, The Alternative To The Riba System ExistsDENNY SATYA ARIBOWONo ratings yet

- Qqyvzu Bafm K Ifjokj Esa Vkidk Lokxr GS: (SMS) : Contact Me' 98457 88800 1800 103 6001 040 4455 6000 8108, - 400051Document12 pagesQqyvzu Bafm K Ifjokj Esa Vkidk Lokxr GS: (SMS) : Contact Me' 98457 88800 1800 103 6001 040 4455 6000 8108, - 400051Charanjeet KohliNo ratings yet

- June 2009 p1Document12 pagesJune 2009 p1zhart1921No ratings yet

- Economics 2 XiiDocument17 pagesEconomics 2 Xiiapi-3703686No ratings yet

- WK - 7 - Relative Valuation PDFDocument33 pagesWK - 7 - Relative Valuation PDFreginazhaNo ratings yet

- Go4itCreditCardTermsConditions PDFDocument29 pagesGo4itCreditCardTermsConditions PDFJismin JosephNo ratings yet

- AP 01 - Cash To Accrual BasisDocument11 pagesAP 01 - Cash To Accrual BasisGabriel OrolfoNo ratings yet

- Guthrie's ChickenDocument5 pagesGuthrie's ChickenpthavNo ratings yet

- Penny Stocks To Hold For The Long-TermDocument6 pagesPenny Stocks To Hold For The Long-TermPGM5HNo ratings yet

- Griham Housing Finance LTD: Your Road To A Dream HomeDocument21 pagesGriham Housing Finance LTD: Your Road To A Dream HomeSSADNo ratings yet

- Nature of Cash & Cashflows Ma2Document12 pagesNature of Cash & Cashflows Ma2ali hansiNo ratings yet