You might also like

- Tax statement for Mrs. Elizabeth FarajiDocument29 pagesTax statement for Mrs. Elizabeth FarajiDead Beat's RandomNo ratings yet

- XYZ Company flexible budget and variance analysisDocument15 pagesXYZ Company flexible budget and variance analysisTanvir OnifNo ratings yet

- Roshan BSLDocument7 pagesRoshan BSLroshan satpathyNo ratings yet

- Income From Salary Solution ZDocument3 pagesIncome From Salary Solution ZMuhammad FaisalNo ratings yet

- Assignment TAX (21 AIS 039)Document18 pagesAssignment TAX (21 AIS 039)Amran OviNo ratings yet

- Fin - 623 Assignment 2Document5 pagesFin - 623 Assignment 2Abdussalam gillNo ratings yet

- Calculating Income from Salary and House PropertyDocument9 pagesCalculating Income from Salary and House PropertyArpita Artani100% (1)

- Shree Chanakya Education Society's Indira Institute of Management, Pune Master of Business Administration Semester - IIDocument5 pagesShree Chanakya Education Society's Indira Institute of Management, Pune Master of Business Administration Semester - IIBanti guptaNo ratings yet

- Veronica Rozario's tax calculation for AY 2021-2022Document5 pagesVeronica Rozario's tax calculation for AY 2021-2022Shakib studentNo ratings yet

- Motilal Excel PlanDocument8 pagesMotilal Excel Plansourajit kunduNo ratings yet

- Part ADocument4 pagesPart APaisley RichesNo ratings yet

- Solution SalariesDocument16 pagesSolution SalariesAniket AgrawalNo ratings yet

- Divine Company Began OperationsDocument1 pageDivine Company Began OperationsQueen ValleNo ratings yet

- Case Study IFP Azmir and ZettyDocument30 pagesCase Study IFP Azmir and Zettyainasyuhada912No ratings yet

- Problems On Income From Salaries: Tax SupplementDocument20 pagesProblems On Income From Salaries: Tax SupplementJkNo ratings yet

- Taxable Salary Problem With Solution Part 1Document2 pagesTaxable Salary Problem With Solution Part 1NagadeepaNo ratings yet

- Paper 4Document16 pagesPaper 4Kali KhannaNo ratings yet

- 9.1 INCOME FROM PROPERTY Notes Questions With SolutionsDocument5 pages9.1 INCOME FROM PROPERTY Notes Questions With SolutionsHASNAT SABIRNo ratings yet

- Previous Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Document4 pagesPrevious Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Sumit PattanaikNo ratings yet

- HRA Sums.Document4 pagesHRA Sums.Saranya kandhasamyNo ratings yet

- Problems On Business/Profession Income: SEM It AssignmentDocument9 pagesProblems On Business/Profession Income: SEM It AssignmentNikhilNo ratings yet

- Benefits. by of Sales: 2020. SuperannuationDocument1 pageBenefits. by of Sales: 2020. SuperannuationArya RoshanNo ratings yet

- Questions & Answers: 2 SalariesDocument26 pagesQuestions & Answers: 2 SalariesSabyasachi Ghosh67% (3)

- Degree Application 2018Document2 pagesDegree Application 2018ldineshkumarNo ratings yet

- Salary Solution 97Document4 pagesSalary Solution 97Al SukranNo ratings yet

- Salary Solution 97Document4 pagesSalary Solution 97Al SukranNo ratings yet

- Questions & Answers - Salary IncomeDocument14 pagesQuestions & Answers - Salary IncomeKiran BendeNo ratings yet

- Project Report Dary FarmDocument7 pagesProject Report Dary FarmAbdul Hakim ShaikhNo ratings yet

- Solution Tax667 - Jun 2018Document9 pagesSolution Tax667 - Jun 2018Aiyani NabihahNo ratings yet

- Principles of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryDocument7 pagesPrinciples of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryWarriach WarriachNo ratings yet

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Document29 pagesSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNo ratings yet

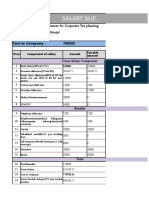

- Salary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117Document5 pagesSalary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117D'quorNo ratings yet

- Ots 24 24009366 Annexure SialileaDocument17 pagesOts 24 24009366 Annexure Sialileaapi-3774915No ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Taxation Nyama AssignmentDocument14 pagesTaxation Nyama AssignmentTakudzwa BenjaminNo ratings yet

- HRA and SalaruDocument1 pageHRA and SalaruAnushree DeyNo ratings yet

- ch14 ExercisesDocument10 pagesch14 ExercisesAriin TambunanNo ratings yet

- M12 Tax ActivityDocument6 pagesM12 Tax ActivityJanna RodriguezNo ratings yet

- Taxation Assignment No 1Document8 pagesTaxation Assignment No 1Ha MimNo ratings yet

- Tax Answerrs and QuestionsDocument33 pagesTax Answerrs and QuestionsoluwafunmilolaabiolaNo ratings yet

- MockDocument6 pagesMockWEI QUAN LEENo ratings yet

- Income TAX: Particular Case 1 Case 2Document15 pagesIncome TAX: Particular Case 1 Case 2Shekh SalmanNo ratings yet

- Working Lecture 7Document17 pagesWorking Lecture 7Sara KarenNo ratings yet

- Techniques of Capital Budgeting SumsDocument15 pagesTechniques of Capital Budgeting Sumshardika jadavNo ratings yet

- CTC SCM Operations Asset DesignDocument3 pagesCTC SCM Operations Asset DesignShubham AgarwalNo ratings yet

- Assignment No 02 Business Law and Taxation: Tauraira Arshad 16320 SolutionDocument2 pagesAssignment No 02 Business Law and Taxation: Tauraira Arshad 16320 SolutionSYEDA -No ratings yet

- Fin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Document2 pagesFin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Abdussalam gillNo ratings yet

- 3.tax Free PDFDocument3 pages3.tax Free PDFArun ShettarNo ratings yet

- Fin420.540 Jan 2018 Q2-5Document8 pagesFin420.540 Jan 2018 Q2-5Amar AzuanNo ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- 4.3 Solution To Income From Salary - Class Work & Home Assignment QuestionsDocument39 pages4.3 Solution To Income From Salary - Class Work & Home Assignment QuestionsKASHISH GUPTANo ratings yet

- Taxation 2004 SolvedDocument18 pagesTaxation 2004 Solvedapi-3832224100% (2)

- Ajay Kumar Jaiswal TDS 2019-20Document10 pagesAjay Kumar Jaiswal TDS 2019-20AJAY KUMAR JAISWALNo ratings yet

- Taxable Income Calculation Mrs. NarayaniDocument5 pagesTaxable Income Calculation Mrs. NarayaniSumit PattanaikNo ratings yet

- B1 Renand Dsouza TYBFMDocument8 pagesB1 Renand Dsouza TYBFMRenandNo ratings yet

- August SalaryDocument1 pageAugust SalarySyed RizwanNo ratings yet

- Activity 1 Partnership Formation and OperationDocument3 pagesActivity 1 Partnership Formation and OperationDianna Rose VicoNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- MLA (Modern Language Association)Document1 pageMLA (Modern Language Association)rathison neonNo ratings yet

- Directory of Open Access Journals (DOAJ) Indexing CriteriaDocument2 pagesDirectory of Open Access Journals (DOAJ) Indexing Criteriarathison neonNo ratings yet

- Group CompiliedDocument30 pagesGroup Compiliedrathison neonNo ratings yet

- Rathison B (Ra2132202010006)Document2 pagesRathison B (Ra2132202010006)rathison neonNo ratings yet

- 1 Income From PGBPDocument21 pages1 Income From PGBPrathison neonNo ratings yet

- Im Cover PageDocument1 pageIm Cover Pagerathison neonNo ratings yet

- SRM Commerce Dept Timetable for Cycle Tests & Model ExamsDocument6 pagesSRM Commerce Dept Timetable for Cycle Tests & Model Examsrathison neonNo ratings yet

- An Academic Perspective On Technical Analysis-NeelyDocument25 pagesAn Academic Perspective On Technical Analysis-Neelygoldorak2No ratings yet

- BIS Loan Request for $200K Warehouse ExpansionDocument4 pagesBIS Loan Request for $200K Warehouse ExpansionOscar Arana50% (2)

- Vector Intro - FraportDocument11 pagesVector Intro - FraportumbradomNo ratings yet

- 365 Ways To Get RichDocument43 pages365 Ways To Get RichRobert Maximilian100% (1)

- Customer Centric Data and AnalyticsDocument18 pagesCustomer Centric Data and AnalyticschrysobergiNo ratings yet

- Rural Marketing 260214 PDFDocument282 pagesRural Marketing 260214 PDFarulsureshNo ratings yet

- Tax Banggawan2019 Ch.15-ADocument12 pagesTax Banggawan2019 Ch.15-ANoreen LeddaNo ratings yet

- Running Head: Case Study Coca Cola Company 1Document12 pagesRunning Head: Case Study Coca Cola Company 1Larbi JosephNo ratings yet

- BBMC 1113 Management Accounting: Distinguish Between A "Prime Cost" and A "Production Overheads Cost"Document2 pagesBBMC 1113 Management Accounting: Distinguish Between A "Prime Cost" and A "Production Overheads Cost"王宇璇No ratings yet

- KapilDocument109 pagesKapilShivmohan JaiswalNo ratings yet

- McDonalds Final Exam (VerC)Document8 pagesMcDonalds Final Exam (VerC)Jose BarrosNo ratings yet

- The Teaching Hub Class Xii Accountancy Chapter 2: The Fundamental of Partnership FirmDocument3 pagesThe Teaching Hub Class Xii Accountancy Chapter 2: The Fundamental of Partnership FirmAthArvA .TNo ratings yet

- Regulatory Framework of Merchant BankingDocument12 pagesRegulatory Framework of Merchant BankingKirti Khattar60% (5)

- Regional Economic Integration and Trade BlocsDocument35 pagesRegional Economic Integration and Trade BlocsTapesh SharmaNo ratings yet

- Mobile App Business PlanDocument12 pagesMobile App Business PlanMuhammad Hidayah0% (1)

- Insurance LawDocument12 pagesInsurance Lawvishal agarwalNo ratings yet

- Marcus ResumeDocument9 pagesMarcus ResumeArmanbekAlkinNo ratings yet

- Ax2009 Enus TL1 03Document78 pagesAx2009 Enus TL1 03amirulzNo ratings yet

- Fe 25 CircularDocument10 pagesFe 25 CircularMaria ChaudhryNo ratings yet

- 1.4 Classification of ProductDocument11 pages1.4 Classification of Productbabunaidu2006No ratings yet

- BankingDocument4 pagesBankingkumareshNo ratings yet

- Lwob - Application-Form Edited Edited EditedDocument2 pagesLwob - Application-Form Edited Edited Editedjessamaeballesteros21100% (1)

- Marketing Management Notes For MG University MBA First SemesterDocument63 pagesMarketing Management Notes For MG University MBA First SemesterSebin Jose100% (2)

- The Global Pharmaceutical IndustryDocument8 pagesThe Global Pharmaceutical IndustryVelan10No ratings yet

- Innovation Management Principles From Iso 50500 SeriesDocument15 pagesInnovation Management Principles From Iso 50500 SeriesEduardo Girón AguirreNo ratings yet

- Modified Tax Calculator With Form-16 - Version 8.2.2 (T) For 2013-14Document28 pagesModified Tax Calculator With Form-16 - Version 8.2.2 (T) For 2013-14Bijender Pal ChoudharyNo ratings yet

- CASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Document1 pageCASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Ataur RahmanNo ratings yet

- Accounting Guide for Non-ProfitsDocument152 pagesAccounting Guide for Non-ProfitsJil Zulueta100% (1)

- Souleymanou KadouamaiDocument12 pagesSouleymanou KadouamaijavisNo ratings yet

- Fcf81Final Placement Notice S&S Associates 2020Document3 pagesFcf81Final Placement Notice S&S Associates 2020swabhiNo ratings yet