You might also like

- Real Traders II: How One CFO Trader Used the Power of Leverage to make $110k in 9 WeeksFrom EverandReal Traders II: How One CFO Trader Used the Power of Leverage to make $110k in 9 WeeksNo ratings yet

- CAN SLIM Analysis Using Online ToolsDocument8 pagesCAN SLIM Analysis Using Online ToolsDeepesh Kothari100% (1)

- Business of Share Trading: From Starting Out to Cashing in with TradingFrom EverandBusiness of Share Trading: From Starting Out to Cashing in with TradingNo ratings yet

- FileDocument1 pageFileSrinNo ratings yet

- Can Slim A Growth Approach Using Technical and Fundamental Data PDFDocument4 pagesCan Slim A Growth Approach Using Technical and Fundamental Data PDFWan ShahmisufiNo ratings yet

- Green Line Breakout (GLB) Explained GMI Remains GreenDocument9 pagesGreen Line Breakout (GLB) Explained GMI Remains GreenChris BoumaNo ratings yet

- Mark Minervini (@markminervini) - Twitter4Document1 pageMark Minervini (@markminervini) - Twitter4LNo ratings yet

- 2005 Mta Ed Seminar MurphyDocument22 pages2005 Mta Ed Seminar MurphyKhai Huynh100% (1)

- Turtle Trading MantraDocument1 pageTurtle Trading MantraYingyong ChiawchansinNo ratings yet

- Ssi Webinar Tom Dorsey PresentationDocument16 pagesSsi Webinar Tom Dorsey PresentationIqbal CaesariawanNo ratings yet

- Catalogue V 22Document20 pagesCatalogue V 22percysearchNo ratings yet

- Insider Monkey HF Newsletter - May 2013Document92 pagesInsider Monkey HF Newsletter - May 2013rvignozzi1No ratings yet

- The Australian Share Market - A History of DeclinesDocument12 pagesThe Australian Share Market - A History of DeclinesNick RadgeNo ratings yet

- Book ListDocument10 pagesBook Listdj1284No ratings yet

- Market Wizards Book SeriesDocument3 pagesMarket Wizards Book SeriesRafael SouzaNo ratings yet

- SellingRulesArticleMay16 PDFDocument8 pagesSellingRulesArticleMay16 PDFGourav SinghalNo ratings yet

- A Trader CheckList - ActiveTraderIQ ArticleDocument3 pagesA Trader CheckList - ActiveTraderIQ ArticleHussan MisthNo ratings yet

- CAN SLIM Trading Strategy OverviewDocument1 pageCAN SLIM Trading Strategy OverviewSudeesh Kumar Pabbathi100% (1)

- Tim Rayment ArticleDocument3 pagesTim Rayment ArticleIstiaque AhmedNo ratings yet

- MarkDocument5 pagesMarkShubhamSetiaNo ratings yet

- A.C.E. Investing: Course InstructorsDocument17 pagesA.C.E. Investing: Course Instructorsbigtrends100% (1)

- Williams %R ScansDocument18 pagesWilliams %R Scansbigtrends100% (1)

- The 5 Secrets To Highly Profitable Swing Trading: Introduction - Why So Many Pros Swing TradeDocument3 pagesThe 5 Secrets To Highly Profitable Swing Trading: Introduction - Why So Many Pros Swing TradeSweety DasNo ratings yet

- List of BooksDocument10 pagesList of BooksstylinbytarunNo ratings yet

- Traders Expo Las Vegas Intensive Workshop November 2011 Pocket PivotsDocument38 pagesTraders Expo Las Vegas Intensive Workshop November 2011 Pocket PivotsteppeiNo ratings yet

- Eckhardt Trading's Disclosure DocumentDocument21 pagesEckhardt Trading's Disclosure DocumentroskenboyNo ratings yet

- Specialists Use of The Media by Richard NeyDocument4 pagesSpecialists Use of The Media by Richard NeyaddqdaddqdNo ratings yet

- Recommended Reading PDFDocument1 pageRecommended Reading PDFNabila Salma50% (2)

- Bull Char Tau Tho Strategy We in Stein HandoutsDocument10 pagesBull Char Tau Tho Strategy We in Stein HandoutsIstiaque AhmedNo ratings yet

- Stp2 Step 5 DocumentationDocument9 pagesStp2 Step 5 DocumentationSooraj MittalNo ratings yet

- Trend Following Commodity Trading AdvisorDocument14 pagesTrend Following Commodity Trading AdvisorTempest SpinNo ratings yet

- 5 Bar Reversal Pattern Trading StrategyDocument1 page5 Bar Reversal Pattern Trading Strategyalistair7682No ratings yet

- How Would You Characterize Your Trading Style?: Tony Oz: Short-Term Trading, Part IDocument8 pagesHow Would You Characterize Your Trading Style?: Tony Oz: Short-Term Trading, Part ItonerangerNo ratings yet

- The Turtle Experiment: Richard Dennis Wanted To Find Out Whether Great Traders Are Born or MadeDocument7 pagesThe Turtle Experiment: Richard Dennis Wanted To Find Out Whether Great Traders Are Born or MadedonmuthuNo ratings yet

- TurtleTrader Interview QuestionsDocument2 pagesTurtleTrader Interview QuestionsMichael Covel100% (1)

- Self Sabotage Reexamined: by Van K. Tharp, PH.DDocument8 pagesSelf Sabotage Reexamined: by Van K. Tharp, PH.DYashkumar JainNo ratings yet

- Evidence Based Technical Analysis Download PDFDocument2 pagesEvidence Based Technical Analysis Download PDFTamara0% (1)

- Greg Morris - 2017 Economic & Investment Summit Presentation - Questionable PracticesDocument53 pagesGreg Morris - 2017 Economic & Investment Summit Presentation - Questionable Practicesstreettalk700No ratings yet

- Street Smart - User ManualDocument466 pagesStreet Smart - User Manualjose58No ratings yet

- Toby Crabel NR2Document5 pagesToby Crabel NR2Aditya SoniNo ratings yet

- Technical Analysis II - Share Market SchoolDocument1 pageTechnical Analysis II - Share Market Schoolbibhuti biswasNo ratings yet

- Technical Analysis in A NutshellDocument46 pagesTechnical Analysis in A Nutshelltechnicalcall100% (1)

- Wyckoff Trading Method SummaryDocument2 pagesWyckoff Trading Method SummaryGuilherme OliveiraNo ratings yet

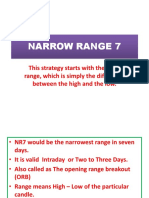

- NR7Document18 pagesNR7RAGHU S100% (1)

- Trading Manual PDFDocument23 pagesTrading Manual PDFTamás TóthNo ratings yet

- Beat the Market by Knowing What Stocks to Buy and SellDocument9 pagesBeat the Market by Knowing What Stocks to Buy and SellPrashantKumarNo ratings yet

- Cup & Handle PatternDocument4 pagesCup & Handle PatternArun KushwahaNo ratings yet

- Kerry Lov Vorn Toolbox No LinksDocument4 pagesKerry Lov Vorn Toolbox No LinksCristina FernandezNo ratings yet

- The Secular Trend and Cyclical Outlook For Bonds, Stocks and CommoditiesDocument69 pagesThe Secular Trend and Cyclical Outlook For Bonds, Stocks and Commoditiescommodi21No ratings yet

- O'NeilDocument99 pagesO'NeilNita JosephNo ratings yet

- A Tale of Two TradersDocument4 pagesA Tale of Two Tradersmayankjain24inNo ratings yet

- Essential guides to stock, options, forex and futures trading strategiesDocument1 pageEssential guides to stock, options, forex and futures trading strategieskjkjkj9099No ratings yet

- Canslim Anlysys PDFDocument31 pagesCanslim Anlysys PDFanh100% (1)

- CAN SLIM AnalysisDocument55 pagesCAN SLIM Analysisram_1201897785No ratings yet

- Security Analysis 6th Edition IntroductionDocument3 pagesSecurity Analysis 6th Edition IntroductionTheodor ToncaNo ratings yet

- Use of fundamental data for active investingDocument30 pagesUse of fundamental data for active investingkanteron6443No ratings yet

- How to Invest in Stocks Like a ProDocument17 pagesHow to Invest in Stocks Like a ProAditya Jaiswal100% (2)

- 18 trading strategies and goals for a trader's dayDocument8 pages18 trading strategies and goals for a trader's dayRavi RamanNo ratings yet

- Trade & Think Like A Champion 1Document5 pagesTrade & Think Like A Champion 1OmSai RamjiNo ratings yet

- Questionnaire HDDocument1 pageQuestionnaire HDVamsi KrishnaNo ratings yet

- MulanDocument2 pagesMulanVamsi KrishnaNo ratings yet

- JPM Big Data and AI StrategiesDocument280 pagesJPM Big Data and AI Strategiesargo82100% (1)

- GE Heathcare CaseDocument9 pagesGE Heathcare CaseVamsi KrishnaNo ratings yet

- MulanDocument2 pagesMulanVamsi KrishnaNo ratings yet

- Cement Pricing Strategy PDFDocument11 pagesCement Pricing Strategy PDFVamsi KrishnaNo ratings yet

- AlgoTrading101 Full SyllabusDocument6 pagesAlgoTrading101 Full SyllabusEmmanuelDasiNo ratings yet

- Your Salary: Single Semimonthly 2Document14 pagesYour Salary: Single Semimonthly 2Vamsi KrishnaNo ratings yet

- Generate Income and Manage Risk with Options StrategiesDocument2 pagesGenerate Income and Manage Risk with Options StrategiesVamsi KrishnaNo ratings yet

- Retailers' InteractionDocument1 pageRetailers' InteractionVamsi KrishnaNo ratings yet

- Vamsi - Data For AnalysisDocument3 pagesVamsi - Data For AnalysisVamsi KrishnaNo ratings yet

- SocialCostBenefitAnalysis DelhiMetroDocument30 pagesSocialCostBenefitAnalysis DelhiMetrorobogineerNo ratings yet

- A Survey On Computer Automated Trading in Indian Stock MarketsDocument10 pagesA Survey On Computer Automated Trading in Indian Stock MarketsVamsi KrishnaNo ratings yet

- Marks - Quiz 3 21.03 PDFDocument5 pagesMarks - Quiz 3 21.03 PDFsnehalNo ratings yet

- OPR Project Report: Submitted byDocument16 pagesOPR Project Report: Submitted byVamsi KrishnaNo ratings yet

- AlgoTrading101 Full SyllabusDocument6 pagesAlgoTrading101 Full SyllabusEmmanuelDasiNo ratings yet

- Acquiring and Retaining Customers in UK BanksDocument13 pagesAcquiring and Retaining Customers in UK Banksabalasa54No ratings yet

- Store density mapping and competitor GTM analysisDocument1 pageStore density mapping and competitor GTM analysisVamsi KrishnaNo ratings yet

- J F Mam J J A S o N D 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31Document5 pagesJ F Mam J J A S o N D 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31Vamsi KrishnaNo ratings yet

- Demographics On Cross SellDocument16 pagesDemographics On Cross SellVamsi KrishnaNo ratings yet

- 1 s2.0 S0895717713000290 Main PDFDocument18 pages1 s2.0 S0895717713000290 Main PDFdiegoman10No ratings yet

- More Than Digital Plus Traditional: A Truly: Omnichannel Customer ExperienceDocument8 pagesMore Than Digital Plus Traditional: A Truly: Omnichannel Customer ExperienceVamsi KrishnaNo ratings yet

- Identifying cross-selling opportunities using lifestyle segmentation and survival analysisDocument17 pagesIdentifying cross-selling opportunities using lifestyle segmentation and survival analysisVamsi KrishnaNo ratings yet

- Application of Predictive Analytics in Volume Forecasting and Resource PlanningDocument69 pagesApplication of Predictive Analytics in Volume Forecasting and Resource PlanningVamsi KrishnaNo ratings yet

- Stages Search Online Review WebsiteDocument1 pageStages Search Online Review WebsiteVamsi KrishnaNo ratings yet

- DigitalTransformation Journey in Lending PDFDocument1 pageDigitalTransformation Journey in Lending PDFVamsi KrishnaNo ratings yet

- Valentinngobo 2004Document32 pagesValentinngobo 2004Vamsi KrishnaNo ratings yet

- Stages Search Online Review WebsiteDocument1 pageStages Search Online Review WebsiteVamsi KrishnaNo ratings yet

- Personal Loan 1Document2 pagesPersonal Loan 1Vamsi KrishnaNo ratings yet

- Skill Shift Automation and The Future of The WorkforceDocument2 pagesSkill Shift Automation and The Future of The WorkforcejordybeltNo ratings yet

- Capsule ProposalDocument2 pagesCapsule ProposalPaula Ysabel BuensucesoNo ratings yet

- Entire All: C. Probability of Success in Any Given TrialDocument10 pagesEntire All: C. Probability of Success in Any Given Triallana del reyNo ratings yet

- Astm MarineDocument16 pagesAstm MarinejhonmarcNo ratings yet

- Pump MixerDocument31 pagesPump MixerPrashant MalveNo ratings yet

- Linking Organizational Culture and Customer Satisf PDFDocument21 pagesLinking Organizational Culture and Customer Satisf PDFMarta KumelaNo ratings yet

- Developing a Framework for Promoting Internal EfficiencyDocument25 pagesDeveloping a Framework for Promoting Internal EfficiencyiPhone Hacks100% (2)

- Rhetorical Analysis: Act I Scene 2: Cassius' SpeechDocument3 pagesRhetorical Analysis: Act I Scene 2: Cassius' Speechapi-329175631No ratings yet

- Mine Planning and Feasibility StudyDocument36 pagesMine Planning and Feasibility Studyjasmin daculaNo ratings yet

- 101 MUET Hacks - A Cheat Sheet For MUET Report WritingDocument14 pages101 MUET Hacks - A Cheat Sheet For MUET Report Writingdesiree heavensNo ratings yet

- Tender Evaluation and Ranking for Contract NameDocument18 pagesTender Evaluation and Ranking for Contract Nameheda kaleniaNo ratings yet

- EIA-Module 2Document41 pagesEIA-Module 2Norah ElizNo ratings yet

- Eap 2 Q3Document69 pagesEap 2 Q3Mis SyNo ratings yet

- Engineering PDFDocument6 pagesEngineering PDFRagul AadhityaNo ratings yet

- Teacher Job Satisfaction in GhanaDocument90 pagesTeacher Job Satisfaction in Ghanah_bilal69No ratings yet

- The Sexual Activity QuestionnaireDocument10 pagesThe Sexual Activity Questionnaireศุภชัย ศิลาวัชรพลNo ratings yet

- SWOT Analysis Insights for Strategic PlanningDocument4 pagesSWOT Analysis Insights for Strategic PlanningSimeony SimeNo ratings yet

- PortlandnessDocument3 pagesPortlandnessSasquatch Books0% (1)

- Narrative ReportDocument9 pagesNarrative ReportPearl AudeNo ratings yet

- Action Plan RubricsDocument5 pagesAction Plan RubricsJuan ObiernaNo ratings yet

- 9 - Comparative Test - Part II - Covermeters PDFDocument13 pages9 - Comparative Test - Part II - Covermeters PDFaskarahNo ratings yet

- Community Needs Assessment: Learning ObjectiveDocument12 pagesCommunity Needs Assessment: Learning ObjectiveSHS Room 3 PC 3No ratings yet

- Employee Retention Project FinalDocument32 pagesEmployee Retention Project FinalVaishu SweetNo ratings yet

- The Object Dedection Capabilities of The Bathymetry System - ENDocument84 pagesThe Object Dedection Capabilities of The Bathymetry System - ENutkuNo ratings yet

- Critical Appraisal On Project Management Approaches in E-GovernmentDocument6 pagesCritical Appraisal On Project Management Approaches in E-GovernmentPaulo AndradeNo ratings yet

- (Elgar Original Reference) Luigino Bruni, Pier Luigi Porta-Handbook On The Economics of Happiness-Edward Elgar (2006) PDFDocument635 pages(Elgar Original Reference) Luigino Bruni, Pier Luigi Porta-Handbook On The Economics of Happiness-Edward Elgar (2006) PDFJulio VargasNo ratings yet

- Engineering Management Other Functions of ManagementDocument49 pagesEngineering Management Other Functions of ManagementGreg Agullana Cañares Jr.67% (3)

- Skew Ness Kurtosis and MomentsDocument31 pagesSkew Ness Kurtosis and MomentsDr. POONAM KAUSHALNo ratings yet

- Lesson 2 - Data Collection Notes - StudentsDocument19 pagesLesson 2 - Data Collection Notes - StudentsSaid Sabri KibwanaNo ratings yet

- Unit 3. Sampling DistributionDocument10 pagesUnit 3. Sampling DistributionMildred Arellano Sebastian100% (2)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet