You might also like

- BIR Ruling 456-2011Document5 pagesBIR Ruling 456-2011Mikz PolzzNo ratings yet

- Tax Bulletin by SGV As of Oct 2014Document18 pagesTax Bulletin by SGV As of Oct 2014adobopinikpikanNo ratings yet

- 209890-2017-Opulent Landowners Inc. v. Commissioner of PDFDocument29 pages209890-2017-Opulent Landowners Inc. v. Commissioner of PDFJobar BuenaguaNo ratings yet

- RMC No. 32-2022Document5 pagesRMC No. 32-2022Shiela Marie MaraonNo ratings yet

- RR No. 13-98Document16 pagesRR No. 13-98Ana DocallosNo ratings yet

- Revised VAT Guidelines for Philippine TaxpayersDocument15 pagesRevised VAT Guidelines for Philippine Taxpayersdencave1No ratings yet

- BIR Ruling 27-02Document2 pagesBIR Ruling 27-02erikagcv100% (1)

- Strict Compliance With The Ten-Day Rule For Application of Authority To TravelDocument1 pageStrict Compliance With The Ten-Day Rule For Application of Authority To TravelEdward MagatNo ratings yet

- RMC 75-2018 Prescribes The Mandatory Statutory Requirement and Function of A Letter of AuthorityDocument2 pagesRMC 75-2018 Prescribes The Mandatory Statutory Requirement and Function of A Letter of AuthorityMiming BudoyNo ratings yet

- AMLCFT and TFS For DNFBPs and NBFIsDocument176 pagesAMLCFT and TFS For DNFBPs and NBFIssitiamera razaliNo ratings yet

- Arm's Length StandardDocument3 pagesArm's Length StandardmatinikkiNo ratings yet

- BIR Ruling 10-98Document3 pagesBIR Ruling 10-98Russell PageNo ratings yet

- 33-CIR v. Wander Philippines, Inc. G.R. No. L-68375 April 15, 1988Document4 pages33-CIR v. Wander Philippines, Inc. G.R. No. L-68375 April 15, 1988Jopan SJNo ratings yet

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- Rmo 01-90 - Amended Penalty ProvisionDocument14 pagesRmo 01-90 - Amended Penalty ProvisionRester John Nonato0% (1)

- LifeBlood - Assessment Process Tax 2Document17 pagesLifeBlood - Assessment Process Tax 2Monjid AbpiNo ratings yet

- Supreme Court Rules Muntinlupa City Ordinance Imposing 3% Tax on Alcohol, Tobacco Sales InvalidDocument8 pagesSupreme Court Rules Muntinlupa City Ordinance Imposing 3% Tax on Alcohol, Tobacco Sales InvalidPaul Joshua SubaNo ratings yet

- Security Rmc39 07Document2 pagesSecurity Rmc39 07Printet08No ratings yet

- Operations Order SBM NO. 2014-013Document3 pagesOperations Order SBM NO. 2014-013Thelma Evangelista100% (1)

- BIR Ruling 023-09Document5 pagesBIR Ruling 023-09Juno Geronimo100% (1)

- CTA 8459 (CADPI) - No DST On Bank Loans, Year-End BalanceDocument74 pagesCTA 8459 (CADPI) - No DST On Bank Loans, Year-End BalanceJerwin DaveNo ratings yet

- Revised Checklist of Requirements For Private Employment Agency (Pea)Document1 pageRevised Checklist of Requirements For Private Employment Agency (Pea)ChipNo ratings yet

- Chapter 1 Cases RianoDocument479 pagesChapter 1 Cases RianoAnonymous 4WA9UcnU2XNo ratings yet

- BIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated OutDocument4 pagesBIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated Outliz kawiNo ratings yet

- Sworn Statement For Application of Permit To Use Loose Leaf Books of AccountsDocument1 pageSworn Statement For Application of Permit To Use Loose Leaf Books of AccountsTesston BullionNo ratings yet

- Classroom Notes On DSTDocument6 pagesClassroom Notes On DSTLalaine ReyesNo ratings yet

- Summary of Significant CTA Decisions (February 2011)Document2 pagesSummary of Significant CTA Decisions (February 2011)ShaneBeriñaImperialNo ratings yet

- Revenue Audit Memorandum 1-98Document5 pagesRevenue Audit Memorandum 1-98Nikos CabreraNo ratings yet

- 2004 BIR - Ruling - DA 320 04 - 20180419 1159 Ho7dm4Document2 pages2004 BIR - Ruling - DA 320 04 - 20180419 1159 Ho7dm4Yya Ladignon100% (2)

- RR 16-99Document6 pagesRR 16-99matinikkiNo ratings yet

- Ra 9337Document23 pagesRa 9337cheska_abigail950No ratings yet

- Compliance Monitoring CertificateDocument1 pageCompliance Monitoring CertificateEly SibayanNo ratings yet

- Bir Ruling 197-93 (May 7, 1993)Document5 pagesBir Ruling 197-93 (May 7, 1993)matinikkiNo ratings yet

- Rmo 63-99Document1 pageRmo 63-99saintkarriNo ratings yet

- Revenue Memorandum Circular No. 09-06: January 25, 2006Document5 pagesRevenue Memorandum Circular No. 09-06: January 25, 2006dom0202No ratings yet

- Revenue Regulations on Minimum Corporate Income TaxDocument5 pagesRevenue Regulations on Minimum Corporate Income TaxKayzer SabaNo ratings yet

- Legal Opinion de MinimisDocument6 pagesLegal Opinion de MinimisjoyiveeongNo ratings yet

- RR 12-98Document3 pagesRR 12-98matinikki100% (1)

- SBFZ Business Registration RequirementsDocument1 pageSBFZ Business Registration RequirementsInquiry PVMNo ratings yet

- Byblgg: Itinerary ReceiptDocument4 pagesByblgg: Itinerary Receiptcherry lyn calama-anNo ratings yet

- RR 9 98 PDFDocument7 pagesRR 9 98 PDFJoey Villas MaputiNo ratings yet

- Tax Update RR 18-2012Document32 pagesTax Update RR 18-2012johamarz6245No ratings yet

- Republic of The Philippines) City of Makati) S.S. Treasurer's AffidavitDocument1 pageRepublic of The Philippines) City of Makati) S.S. Treasurer's AffidavitJoey Albert De GuzmanNo ratings yet

- Bulk Sales Law SummaryDocument12 pagesBulk Sales Law SummaryManuel VillanuevaNo ratings yet

- FGEN: Declaration of Cash DividendsDocument2 pagesFGEN: Declaration of Cash DividendsBusinessWorldNo ratings yet

- Donor's Tax-2Document36 pagesDonor's Tax-2Razel Mhin MendozaNo ratings yet

- Key LS Personnel: PNP Retirement LawsDocument6 pagesKey LS Personnel: PNP Retirement Lawssc law officeNo ratings yet

- Shining Star Playschool Articles of IncorporationDocument10 pagesShining Star Playschool Articles of IncorporationPax YabutNo ratings yet

- Affidavit of Independence SampleDocument1 pageAffidavit of Independence SampleKatrina ManiquisNo ratings yet

- Research CAR and Nominal SharesDocument5 pagesResearch CAR and Nominal Sharesarkina_sunshineNo ratings yet

- Deed of Sole HeirDocument1 pageDeed of Sole HeirLuisa LopezNo ratings yet

- PFF053 MembersContributionRemittanceForm V02-FillableDocument2 pagesPFF053 MembersContributionRemittanceForm V02-FillableCYvelle TorefielNo ratings yet

- RR 3-98Document6 pagesRR 3-98matinikkiNo ratings yet

- Ruben G. Tecson, CPA: Independent Auditor'S ReportDocument3 pagesRuben G. Tecson, CPA: Independent Auditor'S Reportfranchesca marie t. uyNo ratings yet

- Sec Memo Circular No.6 Series of 2008 Section 3Document2 pagesSec Memo Circular No.6 Series of 2008 Section 3orlyNo ratings yet

- Taguig Ord No.21 S.1998 Insurance (CGL)Document4 pagesTaguig Ord No.21 S.1998 Insurance (CGL)Renz MonteroNo ratings yet

- Registration and Accounting ServicesDocument4 pagesRegistration and Accounting ServicesJonathan PradasNo ratings yet

- The Regional Director Bureau of Internal RevenueDocument1 pageThe Regional Director Bureau of Internal RevenueRomrick TorregosaNo ratings yet

- Tax Alert - 2005 - SepDocument7 pagesTax Alert - 2005 - SepjeffreyNo ratings yet

- Bir Ruling No. 383-87Document3 pagesBir Ruling No. 383-87matinikkiNo ratings yet

- United States of America v. Ruiz, 136 SCRA 487 (1985)Document2 pagesUnited States of America v. Ruiz, 136 SCRA 487 (1985)Ckey ArNo ratings yet

- RMC No. 081-12 - Interest Income On Financial InstrumentsDocument5 pagesRMC No. 081-12 - Interest Income On Financial InstrumentsCkey ArNo ratings yet

- RMC - 2013-5 - DOF-DBM-BOCJoint CircularDocument4 pagesRMC - 2013-5 - DOF-DBM-BOCJoint CircularCkey ArNo ratings yet

- BIR clarifies audit program and tax agent responsibilitiesDocument2 pagesBIR clarifies audit program and tax agent responsibilitiesCkey ArNo ratings yet

- Mobil Philippines Exploration, Inc v. Customs Arrestre Service, 18 SCRA 1120 (1966)Document3 pagesMobil Philippines Exploration, Inc v. Customs Arrestre Service, 18 SCRA 1120 (1966)Ckey ArNo ratings yet

- 2010 Income Tax ReturnDocument2 pages2010 Income Tax ReturnCkey ArNo ratings yet

- Republic v. Sandiganbayan (Second Division) 484 SCRA 119 (2006)Document3 pagesRepublic v. Sandiganbayan (Second Division) 484 SCRA 119 (2006)Ckey ArNo ratings yet

- Philippine Nationa Bank v. Pabalan, 83 SCRA 595 (1978)Document2 pagesPhilippine Nationa Bank v. Pabalan, 83 SCRA 595 (1978)Ckey ArNo ratings yet

- Head Injury Case Award UpheldDocument4 pagesHead Injury Case Award UpheldCkey ArNo ratings yet

- BIR - Application For Permit To Adopt Computerized Accounting SystemDocument12 pagesBIR - Application For Permit To Adopt Computerized Accounting SystemCkey ArNo ratings yet

- BIR - Invoicing RequirementsDocument17 pagesBIR - Invoicing RequirementsCkey ArNo ratings yet

- Manual Books of AccountsDocument3 pagesManual Books of AccountsCkey ArNo ratings yet

- Implementing withholding VAT on gov transactionsDocument2 pagesImplementing withholding VAT on gov transactionsCkey ArNo ratings yet

- FAN without PAN violates due processDocument3 pagesFAN without PAN violates due processCkey ArNo ratings yet

- Amended VAT return not allowed due to prior notice of investigationDocument1 pageAmended VAT return not allowed due to prior notice of investigationCkey ArNo ratings yet

- RR No. 26-2002 Staggered FilingDocument5 pagesRR No. 26-2002 Staggered FilingCkey ArNo ratings yet

- Registration Requirements Books AccountsDocument3 pagesRegistration Requirements Books AccountsCkey ArNo ratings yet

- Opinion On Employees Retirement FundDocument3 pagesOpinion On Employees Retirement FundCkey ArNo ratings yet

- P&A - Your Retirement Fund Contributions MatterDocument2 pagesP&A - Your Retirement Fund Contributions MatterCkey ArNo ratings yet

- Provision of Training ServicesDocument6 pagesProvision of Training ServicesCkey ArNo ratings yet

- VAT Official ReceiptsDocument5 pagesVAT Official ReceiptsCkey ArNo ratings yet

- Withholding Tax On IT ServicesDocument6 pagesWithholding Tax On IT ServicesCkey ArNo ratings yet

- Withholding Tax On IT ServicesDocument6 pagesWithholding Tax On IT ServicesCkey ArNo ratings yet

- DST On Policy Holders Registered With PEZADocument5 pagesDST On Policy Holders Registered With PEZACkey ArNo ratings yet

- RR No. 2011-005 - FBT - de Minimis Benefits v2Document5 pagesRR No. 2011-005 - FBT - de Minimis Benefits v2Ckey ArNo ratings yet

- IAET and PEZA EntitiesDocument6 pagesIAET and PEZA EntitiesCkey ArNo ratings yet

- Revenue Regulation 05-08Document3 pagesRevenue Regulation 05-08Agnes Bianca MendozaNo ratings yet

- BIR Ruling No. 095-95 - Consignment Sales - Issuance of Sales InvoiceDocument2 pagesBIR Ruling No. 095-95 - Consignment Sales - Issuance of Sales InvoiceCkey ArNo ratings yet

- RR 02-01Document4 pagesRR 02-01saintkarriNo ratings yet

- Smart Notes Acca f6 2015 (35 Pages)Document38 pagesSmart Notes Acca f6 2015 (35 Pages)SrabonBarua100% (2)

- 2checkout Convertplus: Solution BriefDocument14 pages2checkout Convertplus: Solution BriefhmeyoyanNo ratings yet

- Handbook On Sales U8Document41 pagesHandbook On Sales U8shaik ameer100% (3)

- Wmcustomer 17586699 E73 CustomerInvoice PDFDocument1 pageWmcustomer 17586699 E73 CustomerInvoice PDFmdazajalamNo ratings yet

- Doctrine of Territorial Nexus: Leading Case LawsDocument3 pagesDoctrine of Territorial Nexus: Leading Case Lawssmera singhNo ratings yet

- NEFT/RTGS Challan: Yamuna Expressway Industrial Development Authority ICL1072699866994 ICIC0000103Document2 pagesNEFT/RTGS Challan: Yamuna Expressway Industrial Development Authority ICL1072699866994 ICIC0000103Bharat SharmaNo ratings yet

- Regulations for online ATP system and printing requirementsDocument5 pagesRegulations for online ATP system and printing requirementsJA LogsNo ratings yet

- TUA Income Tax Course SyllabusDocument5 pagesTUA Income Tax Course SyllabusFerdinand Caralde Narciso ImportadoNo ratings yet

- 500,000 PHP to USD conversion rate todayDocument1 page500,000 PHP to USD conversion rate todayPatriceNo ratings yet

- Group 6Document27 pagesGroup 6Joyce Kay AzucenaNo ratings yet

- Personal Reliefs Eligibility ToolDocument5 pagesPersonal Reliefs Eligibility ToolBharat MaddulaNo ratings yet

- Maths PPT Income Tax-Diya ShahDocument5 pagesMaths PPT Income Tax-Diya ShahBrain ChampsNo ratings yet

- RR 07-03Document3 pagesRR 07-03saintkarriNo ratings yet

- Means of Avoiding or Minimizing The Burden of TaxationDocument13 pagesMeans of Avoiding or Minimizing The Burden of TaxationMargaret LachoNo ratings yet

- Aldi Senate SubmissionDocument4 pagesAldi Senate SubmissionMathewDunckleyNo ratings yet

- Jo Valles - SPBUSDocument250 pagesJo Valles - SPBUSSheena MiñosaNo ratings yet

- Bharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Document2 pagesBharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Jinto JacobNo ratings yet

- BIR RR11-2018 SECTION 2.57.3. Persons Required To Deduct and WithholdDocument2 pagesBIR RR11-2018 SECTION 2.57.3. Persons Required To Deduct and WithholdacelaerdenNo ratings yet

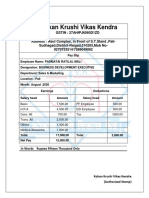

- Kokan Krushi Vikas Kendra pay slips August to October 2020Document3 pagesKokan Krushi Vikas Kendra pay slips August to October 2020DevenNo ratings yet

- Your Statement: Smart AccessDocument2 pagesYour Statement: Smart Accessmohamed elmakhzniNo ratings yet

- Earnings Per ShareDocument3 pagesEarnings Per ShareYeshua DeluxiusNo ratings yet

- Proposal - Vlad's Emporium LimitedDocument6 pagesProposal - Vlad's Emporium LimitedNatali DavydenkoNo ratings yet

- Report IBPMECMCXXXX760BBP - SB 0169-1Document5 pagesReport IBPMECMCXXXX760BBP - SB 0169-1MuhammadAsimNo ratings yet

- 5338 - September 2021 - P33MK3ZQEFJQM1AFODHYA3BR5477351240762656333113912Document1 page5338 - September 2021 - P33MK3ZQEFJQM1AFODHYA3BR5477351240762656333113912Shreyash SahayNo ratings yet

- IRD (IT) - 05-01 Eng VersionDocument2 pagesIRD (IT) - 05-01 Eng VersionZawtun MinNo ratings yet

- DTF 802Document2 pagesDTF 802Peter R MantiaNo ratings yet

- Tax Invoice for Software Reliability Assessment BookDocument1 pageTax Invoice for Software Reliability Assessment BookPrasann BandeNo ratings yet

- Assessment of Companies Coverage and TaxationDocument40 pagesAssessment of Companies Coverage and TaxationMayur RathodNo ratings yet

- UCP Tax Guide: Income Tax for IndividualsDocument9 pagesUCP Tax Guide: Income Tax for IndividualsDin Rose GonzalesNo ratings yet

- Audit of Liabilities 1 PDFDocument1 pageAudit of Liabilities 1 PDFPatricia SingsonNo ratings yet