You might also like

- Maths 10Document3 pagesMaths 10Farheen NawaziNo ratings yet

- DepreciationDocument26 pagesDepreciationSHENUNo ratings yet

- Unit 3 Depreciation AccountingDocument38 pagesUnit 3 Depreciation AccountingBharathi RajuNo ratings yet

- Depreciation Provisions and Reserves Class 11 NotesDocument48 pagesDepreciation Provisions and Reserves Class 11 Notesjainayan8190No ratings yet

- Definition of DepreciationDocument10 pagesDefinition of DepreciationSureshKumarNo ratings yet

- Depreciation Methods and AccountingDocument24 pagesDepreciation Methods and Accountingdishydashy88No ratings yet

- Treasury and Fund ManagementDocument5 pagesTreasury and Fund ManagementAbdul Qudoos tunio :05No ratings yet

- Depreciation 2023-2024 Iisjed Class For 12th Standard CBSEDocument29 pagesDepreciation 2023-2024 Iisjed Class For 12th Standard CBSETaLHa iNaM sameerNo ratings yet

- CH 7 - Depreciation - 1.1Document127 pagesCH 7 - Depreciation - 1.1HYDER ALINo ratings yet

- DEPRECIATIONDocument2 pagesDEPRECIATIONmaryellll457No ratings yet

- Module-4 Depreciation and Inventory ValuationDocument12 pagesModule-4 Depreciation and Inventory ValuationUday ShankarNo ratings yet

- Depreciate An Asset in One YearDocument10 pagesDepreciate An Asset in One Yearbalucbe35No ratings yet

- AssestDocument23 pagesAssestirene oriarewoNo ratings yet

- DepreciationDocument33 pagesDepreciationKleeanne Nicole UmpadNo ratings yet

- DepreciationDocument52 pagesDepreciationPiyush Malhotra50% (2)

- DepreciationDocument20 pagesDepreciationdivya8955No ratings yet

- EEC Unit5-DepreciationDocument4 pagesEEC Unit5-DepreciationSankara nathNo ratings yet

- Depreciation' NatureDocument21 pagesDepreciation' NatureKristia AnagapNo ratings yet

- Chapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesDocument9 pagesChapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesHareem Zoya WarsiNo ratings yet

- Chapter 2 - Plant AssetDocument8 pagesChapter 2 - Plant AssetMelkamu Dessie TamiruNo ratings yet

- DepreciationnnDocument127 pagesDepreciationnnHYDER ALINo ratings yet

- Session 7 - Depreciation AccountingDocument23 pagesSession 7 - Depreciation AccountingManan AgarwalNo ratings yet

- Acct 100 Chapter 8 Notes S22Document60 pagesAcct 100 Chapter 8 Notes S22Cyntia ArellanoNo ratings yet

- Depreciation NotesDocument4 pagesDepreciation NotesAmit AgarwalNo ratings yet

- DepreciationDocument25 pagesDepreciationIvyJoyce50% (2)

- Meaning and DefinitionDocument5 pagesMeaning and DefinitionAdi PoeteraNo ratings yet

- Depreciation-AS 6: Typical Problems Areas of Fixed AccountingDocument4 pagesDepreciation-AS 6: Typical Problems Areas of Fixed AccountingRevanth NvNo ratings yet

- Chapter 7 DepreciationDocument50 pagesChapter 7 Depreciationpriyam.200409No ratings yet

- Depreciation Methods For Wasting Assets: Name:Syed Zain ROLLNO:19351 Subject:Auditing Teachers Name: Madhura MaamDocument12 pagesDepreciation Methods For Wasting Assets: Name:Syed Zain ROLLNO:19351 Subject:Auditing Teachers Name: Madhura MaamSyed ZainNo ratings yet

- Depreciation: Mathematics of InvestmentDocument18 pagesDepreciation: Mathematics of InvestmentAjese C. Almirez100% (1)

- Units of Production Method of DepreciationDocument3 pagesUnits of Production Method of DepreciationPraneeth SaiNo ratings yet

- Depreciation and Provision For DepreciationDocument2 pagesDepreciation and Provision For DepreciationAnsha Twilight14No ratings yet

- Fair Value Matching PrincipleDocument5 pagesFair Value Matching PrincipleGracie Kiarie100% (1)

- Cash Book and DepreciationDocument8 pagesCash Book and Depreciationbalajigorle53No ratings yet

- Financial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsDocument55 pagesFinancial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsmukul3087_305865623No ratings yet

- Chapter 11: Depreciation, Impairments and DepletionDocument24 pagesChapter 11: Depreciation, Impairments and DepletionRahat KhanNo ratings yet

- Chap 5Document10 pagesChap 5khedira sami100% (1)

- Depreciation MethodsDocument17 pagesDepreciation MethodsAbdullah RamzanNo ratings yet

- Depreciation and Methods of Calculating Depreciation Difference Between Depreciation, Amortization and Depletion"Document7 pagesDepreciation and Methods of Calculating Depreciation Difference Between Depreciation, Amortization and Depletion"Maria QamarNo ratings yet

- ACC101 Chapter8newDocument19 pagesACC101 Chapter8newLaras Sukma Nurani TirtawidjajaNo ratings yet

- The Depreciation MethodsDocument9 pagesThe Depreciation MethodsPrince-SimonJohnMwanzaNo ratings yet

- Basic Financial AccountingDocument13 pagesBasic Financial Accountingalok beheraNo ratings yet

- DepreciationDocument5 pagesDepreciationAniket Paul ChoudhuryNo ratings yet

- What Is Depreciation in Business?Document6 pagesWhat Is Depreciation in Business?Baneo MayuriNo ratings yet

- C27 Depreciation PDFDocument20 pagesC27 Depreciation PDFRomuell BanaresNo ratings yet

- DEPRECIATIONDocument4 pagesDEPRECIATIONAlexander DimaliposNo ratings yet

- What Are The Main Types of Depreciation Methods?: Depreciation Expense Book ValueDocument6 pagesWhat Are The Main Types of Depreciation Methods?: Depreciation Expense Book ValueBR Lake City LHRNo ratings yet

- Chapter 11Document26 pagesChapter 11ENG ZI QINGNo ratings yet

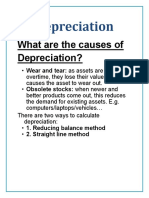

- What Are The Causes of Depreciation?Document10 pagesWhat Are The Causes of Depreciation?Everyday LearnNo ratings yet

- Corporatefinanceinstitute Com Resources Knowledge Accounting Types DepreciationDocument10 pagesCorporatefinanceinstitute Com Resources Knowledge Accounting Types DepreciationstudentNo ratings yet

- Assignment-2: Name: Mayank ROLL NO.:181210029Document5 pagesAssignment-2: Name: Mayank ROLL NO.:181210029Mayank KajlaNo ratings yet

- Chapter 7 DepDocument18 pagesChapter 7 DepvandhanaNo ratings yet

- Depreciation Method of ValuationDocument17 pagesDepreciation Method of ValuationAnagha AjayNo ratings yet

- Depreciation: By: Ibrahim KaplanDocument23 pagesDepreciation: By: Ibrahim KaplanManzoor Samim100% (1)

- 5 - DepreciationDocument31 pages5 - Depreciationdewatharschinia19No ratings yet

- Accountancy Depreciation Seminar Group 7Document13 pagesAccountancy Depreciation Seminar Group 7Lakshay BajajNo ratings yet

- Methods of DepreciationDocument12 pagesMethods of Depreciationamun din100% (1)

- Accounting For Depreciation Accounting For DepreciationDocument32 pagesAccounting For Depreciation Accounting For DepreciationKaranNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Assignment: 1: School of Electronics Engineering ECE4009-Wireless and Mobile CommunicationsDocument2 pagesAssignment: 1: School of Electronics Engineering ECE4009-Wireless and Mobile CommunicationsAYUSH GURTU 17BEC0185No ratings yet

- Wireless and Mobile Communication: Lab Task - 3 Slot: L1+ L2Document4 pagesWireless and Mobile Communication: Lab Task - 3 Slot: L1+ L2AYUSH GURTU 17BEC0185No ratings yet

- Asset-V1 VIT+BMT1005+2020+type@asset+block@week 3 Lecture NotesDocument9 pagesAsset-V1 VIT+BMT1005+2020+type@asset+block@week 3 Lecture NotesAYUSH GURTU 17BEC0185No ratings yet

- Asset-V1 - VIT BMT1005 2020 Type@asset block@Week-11-Annuity-MaterialDocument7 pagesAsset-V1 - VIT BMT1005 2020 Type@asset block@Week-11-Annuity-MaterialAYUSH GURTU 17BEC0185No ratings yet

- Task:: Lab Task - 4 Slot: L1+ L2 TEAM: AYUSH GURTU (Reg - No: 17BEC0185)Document2 pagesTask:: Lab Task - 4 Slot: L1+ L2 TEAM: AYUSH GURTU (Reg - No: 17BEC0185)AYUSH GURTU 17BEC0185No ratings yet

- Asset-V1 VIT+BMT1005+2020+type@asset+block@Annuities TableDocument2 pagesAsset-V1 VIT+BMT1005+2020+type@asset+block@Annuities TableAYUSH GURTU 17BEC0185No ratings yet

- TCS - Digital 2Document23 pagesTCS - Digital 2AYUSH GURTU 17BEC0185No ratings yet

- StackDocument48 pagesStackAYUSH GURTU 17BEC0185No ratings yet

- SDOT Training Day2Document93 pagesSDOT Training Day2AYUSH GURTU 17BEC0185No ratings yet

- DS TreeDocument41 pagesDS TreeAYUSH GURTU 17BEC0185No ratings yet

- Asset-V1 VIT+MSC1004+2020+type@asset+block@W9 NotesDocument72 pagesAsset-V1 VIT+MSC1004+2020+type@asset+block@W9 NotesAYUSH GURTU 17BEC0185No ratings yet

- Asset-V1 VIT+MSC1004+2020+type@asset+block@W5 NotesDocument55 pagesAsset-V1 VIT+MSC1004+2020+type@asset+block@W5 NotesAYUSH GURTU 17BEC0185No ratings yet

- Coerver Training DrillsDocument5 pagesCoerver Training Drillsburvi200111860% (1)

- Persuasion PyramidDocument1 pagePersuasion PyramidKenzie DoctoleroNo ratings yet

- BS 6089 - 2010 - Assessment of Insitu Compressive TestDocument40 pagesBS 6089 - 2010 - Assessment of Insitu Compressive TestMike Chan100% (2)

- Àmjj JJMJJ JJMJJJJJJJ JJJJJJJ JJ: JJJ JJJ JJJDocument7 pagesÀmjj JJMJJ JJMJJJJJJJ JJJJJJJ JJ: JJJ JJJ JJJDezekiel DriapNo ratings yet

- Data Structures and Problem Solving Using JavaDocument20 pagesData Structures and Problem Solving Using JavaBrent Xavier AgnoNo ratings yet

- Tariq Ali 1Document62 pagesTariq Ali 1Hafeezullah ShareefNo ratings yet

- Input OutputcrwillDocument21 pagesInput OutputcrwillAbhishek SinghNo ratings yet

- C.8 SOLUTIONS (Problems I - IX)Document9 pagesC.8 SOLUTIONS (Problems I - IX)Bianca AcoymoNo ratings yet

- W1 8GEC 2A Readings in The Philippine History IPED ModuleDocument74 pagesW1 8GEC 2A Readings in The Philippine History IPED ModuleMico S. IglesiaNo ratings yet

- GBC Module 1Document69 pagesGBC Module 1MOHAMED82% (129)

- Circular WaveguideDocument19 pagesCircular WaveguideLam DinhNo ratings yet

- EacdocDocument84 pagesEacdocJohanMonNo ratings yet

- PF2 S02-10 in Burning DawnDocument31 pagesPF2 S02-10 in Burning Dawnxajos85812No ratings yet

- 2 PassivetransportDocument8 pages2 PassivetransportFayeNo ratings yet

- India: "Truth Alone Triumphs"Document103 pagesIndia: "Truth Alone Triumphs"Rajesh NaiduNo ratings yet

- Valley Line LRT Preliminary DesignDocument26 pagesValley Line LRT Preliminary DesigncaleyramsayNo ratings yet

- Basic Hygiene & Food Safety Training ModuleDocument43 pagesBasic Hygiene & Food Safety Training ModuleRelianceHRNo ratings yet

- 5E Lesson Plan Template: TeacherDocument6 pages5E Lesson Plan Template: Teacherapi-534260240No ratings yet

- Visualization BenchmarkingDocument15 pagesVisualization BenchmarkingRanjith S100% (1)

- Sachet MarketingDocument7 pagesSachet MarketingTom JohnNo ratings yet

- CH 4 Network SecurityDocument37 pagesCH 4 Network SecurityHirko GemechuNo ratings yet

- CSN-261: Data Structures Laboratory: Lab Assignment 5 (L5)Document3 pagesCSN-261: Data Structures Laboratory: Lab Assignment 5 (L5)GajananNo ratings yet

- AC405 Assignment R185840RDocument3 pagesAC405 Assignment R185840RDiatomspinalcordNo ratings yet

- On Campus BA - Consultant JDDocument2 pagesOn Campus BA - Consultant JDSivaramakrishna SobhaNo ratings yet

- E Dies Astm d5963 CuttingdiesDocument1 pageE Dies Astm d5963 CuttingdiesNate MercerNo ratings yet

- Electrothermal Industries PDFDocument10 pagesElectrothermal Industries PDFAna Marie AllamNo ratings yet

- Sebaceous Gland Secretion Is A Major Physiologic Route of Vitamin E Delivery To SkinDocument5 pagesSebaceous Gland Secretion Is A Major Physiologic Route of Vitamin E Delivery To SkinumegeeNo ratings yet

- Goat Fattening Rs. 0.85 MillionDocument18 pagesGoat Fattening Rs. 0.85 MillionZakir Ali100% (1)

- Affordable HousingDocument12 pagesAffordable HousingTenzin KesangNo ratings yet

- CC W3 AWS Basic InfraDocument57 pagesCC W3 AWS Basic InfraMuhammad Tehseen KhanNo ratings yet