You might also like

- April 2014 MLC Multiple Choice Solutions: L L L L L L D Q L L LDocument9 pagesApril 2014 MLC Multiple Choice Solutions: L L L L L L D Q L L LHông HoaNo ratings yet

- Fall 2006 Exam M Solutions: Pa APVDocument29 pagesFall 2006 Exam M Solutions: Pa APVHông HoaNo ratings yet

- Problem Set 2 - SolutionsDocument3 pagesProblem Set 2 - Solutionshoi chingNo ratings yet

- CH 9Document53 pagesCH 9Matt BeardNo ratings yet

- 2012 04 MLC Exam SolDocument20 pages2012 04 MLC Exam SolAki TsukiyomiNo ratings yet

- Exercises in Life-, Health-And Pension-MathematicsDocument5 pagesExercises in Life-, Health-And Pension-MathematicsDipen PandyaNo ratings yet

- 2do Parcial - Cavanna Mateo - 901291Document11 pages2do Parcial - Cavanna Mateo - 901291Sofia HernándezNo ratings yet

- Solutions For Exercises in Chapter 2Document3 pagesSolutions For Exercises in Chapter 2Felipe DiazNo ratings yet

- To Dooooo LocoDocument15 pagesTo Dooooo LocofelipeNo ratings yet

- Decision Science - AssignmentDocument6 pagesDecision Science - AssignmentShilpi SinghNo ratings yet

- Grafik t vs (ln〖10〗^3 (A) ) /ln10: Desi Wulandari 160332605877 Offering IDocument4 pagesGrafik t vs (ln〖10〗^3 (A) ) /ln10: Desi Wulandari 160332605877 Offering IDesiNo ratings yet

- A $42888.18 The Simple Interest Formula IsDocument3 pagesA $42888.18 The Simple Interest Formula IsSoro IsmaelNo ratings yet

- Tutorial Answer: Annuities: AnswersDocument6 pagesTutorial Answer: Annuities: AnswersNurul HudaNo ratings yet

- Decision Science AssignmentDocument4 pagesDecision Science AssignmentShivani MallikNo ratings yet

- PracticeProblems 4315 SolutionsDocument9 pagesPracticeProblems 4315 SolutionsKashifRizwanNo ratings yet

- Statisztikai Alapismeretek - Bugya Titusz 2003Document211 pagesStatisztikai Alapismeretek - Bugya Titusz 2003Gyuri SzerencsésNo ratings yet

- Math (PH M Minh Khoa)Document22 pagesMath (PH M Minh Khoa)Minh Khoa PhạmNo ratings yet

- Solution Manual For Introductory Statistics 9th by MannDocument25 pagesSolution Manual For Introductory Statistics 9th by MannKatelynWebsterikzj100% (43)

- ListaEstatisticaProbabilidade 1Document5 pagesListaEstatisticaProbabilidade 1Adrielly IslyNo ratings yet

- Ch19 21Document3 pagesCh19 21Shivansh ChawlaNo ratings yet

- ReviewProblems1 Solution PDFDocument14 pagesReviewProblems1 Solution PDFRosalie-Ann MasséNo ratings yet

- FM09-CH 16Document12 pagesFM09-CH 16Mukul KadyanNo ratings yet

- Irr and Incremental IrrDocument10 pagesIrr and Incremental IrrrashiNo ratings yet

- Irr and Incremental IrrDocument10 pagesIrr and Incremental IrrrashiNo ratings yet

- Nsbe9ege Ism ch10Document35 pagesNsbe9ege Ism ch10高一二No ratings yet

- Edu 2021 Fall Solutions Ltam FormaDocument29 pagesEdu 2021 Fall Solutions Ltam FormaPrincess BlessingNo ratings yet

- Tugas Distribusi Probabilitas Ivonella 1Document8 pagesTugas Distribusi Probabilitas Ivonella 1Ivonella maraniNo ratings yet

- AF208 Major Assignment Year 2014: Name: ID: Center: Tutorial: TutorDocument8 pagesAF208 Major Assignment Year 2014: Name: ID: Center: Tutorial: Tutoramir abdulNo ratings yet

- Electric Circuits 10Th Edition Nilsson Solutions Manual Full Chapter PDFDocument36 pagesElectric Circuits 10Th Edition Nilsson Solutions Manual Full Chapter PDFjerrold.zuniga266100% (11)

- Ial Maths s1 Ex7d PDFDocument5 pagesIal Maths s1 Ex7d PDFahmed ramadanNo ratings yet

- Assignment 5Document3 pagesAssignment 5EmadNo ratings yet

- Linear ProgrammingDocument8 pagesLinear ProgrammingJustin Pindit LASAKNo ratings yet

- Final Spring07 Solutions SampleDocument15 pagesFinal Spring07 Solutions SampleAnass BNo ratings yet

- Economy Prob Set 2Document9 pagesEconomy Prob Set 2Joselito DaroyNo ratings yet

- Manual de Soluciones Capítulo 7 Ejercicios 7.2 2. 32,000 R (1 + 0.1336/52)Document36 pagesManual de Soluciones Capítulo 7 Ejercicios 7.2 2. 32,000 R (1 + 0.1336/52)StevenNo ratings yet

- Digital Image Processing Lab Manual: Experiment-1Document13 pagesDigital Image Processing Lab Manual: Experiment-1Anonymous G5D0xzq2No ratings yet

- Tarea #3 - Litardo. DanielaDocument6 pagesTarea #3 - Litardo. DanielaDaniela FernandaNo ratings yet

- MB10 AnnuitasDocument8 pagesMB10 Annuitasm habiburrahman55No ratings yet

- 0,1 a 1 6a a 3a = ⇒ = + +: μ) E (X − = = p (x) x) E (XDocument11 pages0,1 a 1 6a a 3a = ⇒ = + +: μ) E (X − = = p (x) x) E (XMAIQUEL VELOSONo ratings yet

- JK2e Ch006 SMDocument30 pagesJK2e Ch006 SMSakshi AgarwalNo ratings yet

- 2022 Ebmv301 TM2 MemoDocument7 pages2022 Ebmv301 TM2 MemoSouthNo ratings yet

- It Is Important To Note That in The Optimal Q The Two Costs Are EqualDocument6 pagesIt Is Important To Note That in The Optimal Q The Two Costs Are EqualKaren MárquezNo ratings yet

- Perhitungan Regresi Dengan Excell Secara ManualDocument7 pagesPerhitungan Regresi Dengan Excell Secara Manualnaning mekawatiNo ratings yet

- Compound InterestDocument6 pagesCompound InterestJustin Pindit LASAKNo ratings yet

- Ch13s PDFDocument25 pagesCh13s PDFLuis AntonioNo ratings yet

- MA2177 Ex6 SolDocument3 pagesMA2177 Ex6 Solkyle cheungNo ratings yet

- Lampiran Perhitungan: PengukuransudutputarjenissampelDocument4 pagesLampiran Perhitungan: PengukuransudutputarjenissampelMulia Sri RahmawatiNo ratings yet

- Taller 7Document11 pagesTaller 7Stiven Orjuela GomezNo ratings yet

- ch06 IsmDocument34 pagesch06 IsmQuero22No ratings yet

- Ang .I 180 Ang .I 180 Ang .I 180 Ang .I 540: 1) Calculo Cierre AngularDocument4 pagesAng .I 180 Ang .I 180 Ang .I 180 Ang .I 540: 1) Calculo Cierre Angularrussel calderon chochocaNo ratings yet

- Statistics For Business and Economics Revised 12th Edition Anderson Solutions ManualDocument27 pagesStatistics For Business and Economics Revised 12th Edition Anderson Solutions Manualchieverespectsew100% (25)

- F2 Maths MSDocument12 pagesF2 Maths MSkaratinagirlssecNo ratings yet

- Della Rifka - Tugas Individu SKP Meet 14Document7 pagesDella Rifka - Tugas Individu SKP Meet 14Wildan Bisyri AzizNo ratings yet

- Decision ScienceDocument8 pagesDecision ScienceHimanshi YadavNo ratings yet

- Doane Chap012 ASBE 7e SMDocument78 pagesDoane Chap012 ASBE 7e SMpavistatsNo ratings yet

- Simple InterestDocument6 pagesSimple InterestJustin Pindit LASAKNo ratings yet

- Predimensionamiento de Columnas: Bloque BDocument11 pagesPredimensionamiento de Columnas: Bloque BAlexander Vargas TiradoNo ratings yet

- Electric Circuits 10th Edition Nilsson Solutions ManualDocument54 pagesElectric Circuits 10th Edition Nilsson Solutions Manualedwardleonw10100% (31)

- Instructor's Manual to Accompany CALCULUS WITH ANALYTIC GEOMETRYFrom EverandInstructor's Manual to Accompany CALCULUS WITH ANALYTIC GEOMETRYNo ratings yet

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- Stolyarov MFE Study Guide PDFDocument279 pagesStolyarov MFE Study Guide PDFSachin SomaniNo ratings yet

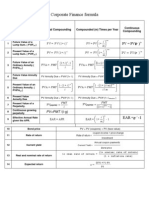

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- SOA MFE 76 Practice Ques SolsDocument70 pagesSOA MFE 76 Practice Ques SolsGracia DongNo ratings yet

- LTAM01 - Chap 2 - Assignment PDFDocument10 pagesLTAM01 - Chap 2 - Assignment PDFHông HoaNo ratings yet

- Introduction To Econometrics With RDocument400 pagesIntroduction To Econometrics With RHervé DakpoNo ratings yet

- MFE SampleQS1-76Document185 pagesMFE SampleQS1-76Jihyeon Kim100% (1)

- GMAC 09LLCAgreementDocument100 pagesGMAC 09LLCAgreementHoaNo ratings yet

- 1 Exam FM QuestionsDocument36 pages1 Exam FM QuestionsMiguel Grau100% (1)

- Exam FM QuestioonsDocument102 pagesExam FM Questioonsnkfran100% (1)

- Exam FM Sample SolutionsDocument56 pagesExam FM Sample SolutionsJessica NoviaNo ratings yet

- Fap Module ObjectivesDocument25 pagesFap Module ObjectivesHông HoaNo ratings yet

- The Gauss-Markov Theorem in Anal Sis by L. Eaton of of Echnical 422Document36 pagesThe Gauss-Markov Theorem in Anal Sis by L. Eaton of of Echnical 422Hông HoaNo ratings yet

- A Prlmal Algorithm For Interval Linear-Programming ProblemsDocument14 pagesA Prlmal Algorithm For Interval Linear-Programming ProblemsHông HoaNo ratings yet

- Chapter 4. Gauss-Markov ModelDocument20 pagesChapter 4. Gauss-Markov ModelHông HoaNo ratings yet

- Edu 2020 02 FM Percents Ogu4ljDocument1 pageEdu 2020 02 FM Percents Ogu4ljHông HoaNo ratings yet

- Stat 5102 Lecture Slides: Deck 6 Gauss-Markov Theorem, Sufficiency, Generalized Linear Models, Likelihood Ratio Tests, Categorical Data AnalysisDocument86 pagesStat 5102 Lecture Slides: Deck 6 Gauss-Markov Theorem, Sufficiency, Generalized Linear Models, Likelihood Ratio Tests, Categorical Data AnalysisHông HoaNo ratings yet

- Main PDFDocument7 pagesMain PDFMukminin BaharuddinNo ratings yet

- 2021 04 Exam FM SyllabiDocument10 pages2021 04 Exam FM SyllabiHông HoaNo ratings yet

- Archive: 1969 SheridanDocument72 pagesArchive: 1969 SheridanHông HoaNo ratings yet

- 2020 6 17 Exam Pa Project Statement PDFDocument6 pages2020 6 17 Exam Pa Project Statement PDFHông HoaNo ratings yet

- Prudential Supervision ENDocument9 pagesPrudential Supervision ENHông HoaNo ratings yet

- VN Salary Guide 2020Document28 pagesVN Salary Guide 2020Raven NgoNo ratings yet

- Exam Pa 06 19 Model SolutionDocument17 pagesExam Pa 06 19 Model SolutionHông HoaNo ratings yet

- Exam Pa 06 17 Model Solution PDFDocument21 pagesExam Pa 06 17 Model Solution PDFHông HoaNo ratings yet

- 2020 6 19 Exam Pa Project Statement PDFDocument6 pages2020 6 19 Exam Pa Project Statement PDFHông HoaNo ratings yet

- 2020 6 19 Exam Pa Project Statement PDFDocument6 pages2020 6 19 Exam Pa Project Statement PDFHông HoaNo ratings yet

- Exam Pa 06 16 Model Solution PDFDocument18 pagesExam Pa 06 16 Model Solution PDFHông HoaNo ratings yet

- 1-A Colored Substance That Is Spread Over A Surface and Dries To Leave A Thin Decorative or Protective Coating. Decorative or Protective CoatingDocument60 pages1-A Colored Substance That Is Spread Over A Surface and Dries To Leave A Thin Decorative or Protective Coating. Decorative or Protective Coatingjoselito lacuarinNo ratings yet

- History of Some Special ExplosivesDocument24 pagesHistory of Some Special ExplosivesShazil KhanNo ratings yet

- A Grammar of Power in Psychotherapy Exploring The Dynamics of Privilege (Malin Fors)Document220 pagesA Grammar of Power in Psychotherapy Exploring The Dynamics of Privilege (Malin Fors)Andrea A. Ortiz Vázquez100% (1)

- A Rare Peripheral Odontogenic Keratocyst in Floor of Mouth: A Case ReportDocument6 pagesA Rare Peripheral Odontogenic Keratocyst in Floor of Mouth: A Case ReportIJAR JOURNALNo ratings yet

- Sample Cylinders - PGI-CYLDocument8 pagesSample Cylinders - PGI-CYLcalpeeNo ratings yet

- 1000 Câu Word FormDocument36 pages1000 Câu Word FormThùy Linh LêNo ratings yet

- Year Test - Ii: (Batch - A)Document11 pagesYear Test - Ii: (Batch - A)sachin sakuNo ratings yet

- CoC VampireCharacterPrimerPDFDocument5 pagesCoC VampireCharacterPrimerPDFDavid Alexander TomblinNo ratings yet

- Week 1Document14 pagesWeek 1kohalehNo ratings yet

- Nexgard For Dogs and Puppies Free 2 Day ShippingDocument1 pageNexgard For Dogs and Puppies Free 2 Day Shippinglyly23748No ratings yet

- Bronce C90700Document2 pagesBronce C90700Luis Enrique CarranzaNo ratings yet

- Midterm and Final Exam TFNDocument6 pagesMidterm and Final Exam TFNalchriwNo ratings yet

- Neonatal SepsisDocument29 pagesNeonatal SepsisElton Ndhlovu100% (3)

- Inquiries Research Titles SOP ExamplesDocument10 pagesInquiries Research Titles SOP ExamplesEunice Pineza ManlunasNo ratings yet

- MOLYKOTE 1000 Paste 71-0218H-01Document2 pagesMOLYKOTE 1000 Paste 71-0218H-01Victor PomboNo ratings yet

- Material Data Sheet Durapro Asa: DescriptionDocument1 pageMaterial Data Sheet Durapro Asa: DescriptionAlexandru NeacsuNo ratings yet

- Imaging-Guided Chest Biopsies: Techniques and Clinical ResultsDocument10 pagesImaging-Guided Chest Biopsies: Techniques and Clinical Resultsweni kartika nugrohoNo ratings yet

- Mechanical Operation Slurry TransportDocument113 pagesMechanical Operation Slurry TransportIsrarulHaqueNo ratings yet

- Directory of Acredited Medical Testing LaboratoriesDocument93 pagesDirectory of Acredited Medical Testing LaboratoriesCALIDAD METROMEDICA E.UNo ratings yet

- 10 Achievement ChartDocument3 pages10 Achievement ChartLyka ollerasNo ratings yet

- API 510 Study GuideDocument3 pagesAPI 510 Study GuidedanikakaNo ratings yet

- MSDS TSHDocument8 pagesMSDS TSHdwiNo ratings yet

- Nath Bio-Genes at Inflection Point-2Document9 pagesNath Bio-Genes at Inflection Point-2vinodtiwari808754No ratings yet

- Planets in NakshatrasDocument6 pagesPlanets in Nakshatrasmurthyy55% (11)

- Nasoalveolar Moulding Seminar at MalakkaraDocument54 pagesNasoalveolar Moulding Seminar at MalakkaraAshwin100% (1)

- Khalifa NagwaDocument111 pagesKhalifa NagwajokonudiNo ratings yet

- Multiple Choice Questions: Topic Covered Are As FollowsDocument3 pagesMultiple Choice Questions: Topic Covered Are As FollowsBikash SahuNo ratings yet

- Cockerspaniel Pra CarriersDocument28 pagesCockerspaniel Pra CarriersJo M. ChangNo ratings yet

- Sample CV Format (JIMS FORMAT)Document3 pagesSample CV Format (JIMS FORMAT)Elay PedrosoNo ratings yet

- Lab 5 - ReportDocument9 pagesLab 5 - ReportScarlet ErzaNo ratings yet