You might also like

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioFrom EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioRating: 4.5 out of 5 stars4.5/5 (3)

- Risk and Rates of ReturnDocument22 pagesRisk and Rates of ReturnAjay Kumar BinaniNo ratings yet

- Risk and Rates of ReturnDocument16 pagesRisk and Rates of ReturnSally Goodwill100% (1)

- Risk and Return AnalysisDocument28 pagesRisk and Return AnalysisNivaashene SaravananNo ratings yet

- FM Unit 3 Lecture Notes - Risk and ReturnDocument6 pagesFM Unit 3 Lecture Notes - Risk and ReturnDebbie DebzNo ratings yet

- IFA NAZUWA (69875) Tutorial 2Document6 pagesIFA NAZUWA (69875) Tutorial 2Ifa Nazuwa ZaidilNo ratings yet

- Risks and Rates of Return ExplainedDocument2 pagesRisks and Rates of Return ExplainedCandelNo ratings yet

- Reading 50 Portfolio Risk and Return Part II AnswersDocument46 pagesReading 50 Portfolio Risk and Return Part II AnswersK59 Nguyen Thao LinhNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsDocument36 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuNo ratings yet

- CH 6 SolDocument14 pagesCH 6 Solroha_rizvi5972No ratings yet

- D - Tutorial 7 (Solutions)Document10 pagesD - Tutorial 7 (Solutions)AlfieNo ratings yet

- Session 5Document17 pagesSession 5maha khanNo ratings yet

- Capm-Apt Notes 2021Document4 pagesCapm-Apt Notes 2021hardik jainNo ratings yet

- FM 8th Edition Chapter 12 - Risk and ReturnDocument20 pagesFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNo ratings yet

- An Analysis of CAPMDocument5 pagesAn Analysis of CAPMJenipher Carlos HosannaNo ratings yet

- Risk & Return FundamentalsDocument24 pagesRisk & Return FundamentalsHadi TheoNo ratings yet

- Module 2 CAPMDocument11 pagesModule 2 CAPMTanvi DevadigaNo ratings yet

- Financial Management Basics of Risk and ReturnDocument10 pagesFinancial Management Basics of Risk and ReturnHenok FikaduNo ratings yet

- Week 7 Week 8 - Intro To Portfolio TheoryDocument24 pagesWeek 7 Week 8 - Intro To Portfolio TheoryJoshua NemiNo ratings yet

- SAPMDocument83 pagesSAPMSuchismitaghoseNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main ViewDocument47 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main ViewKazi FahimNo ratings yet

- Return and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)Document52 pagesReturn and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)anna_alwanNo ratings yet

- Jawaban Buku ALK Subramanyam Bab 7Document8 pagesJawaban Buku ALK Subramanyam Bab 7Must Joko100% (1)

- Mathematical Corporate Finance I - Unit 4Document24 pagesMathematical Corporate Finance I - Unit 4ernestessel95No ratings yet

- On Capital Asset Pricing Model: Submitted byDocument14 pagesOn Capital Asset Pricing Model: Submitted bybansiiboyNo ratings yet

- CMPMDocument8 pagesCMPMLarry DixonNo ratings yet

- Risk and Return S1 2018Document9 pagesRisk and Return S1 2018Quentin SchwartzNo ratings yet

- Topic 4Document26 pagesTopic 420070304 Nguyễn Thị PhươngNo ratings yet

- Topic Risk and ReturnDocument5 pagesTopic Risk and ReturnVic CinoNo ratings yet

- Capital Asset Pricing ModelDocument10 pagesCapital Asset Pricing Modeljackie555No ratings yet

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryDocument19 pagesCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiNo ratings yet

- Financial Management Chapter 06 IM 10th EdDocument30 pagesFinancial Management Chapter 06 IM 10th EdDr Rushen SinghNo ratings yet

- Capital Market Theory: What Happens When A Risk-Free Asset Is Added To A Portfolio of Risky Assets?Document5 pagesCapital Market Theory: What Happens When A Risk-Free Asset Is Added To A Portfolio of Risky Assets?Padyala SriramNo ratings yet

- Ch06 Solations Brigham 10th EDocument32 pagesCh06 Solations Brigham 10th ERafay HussainNo ratings yet

- Rangkuman Bab 9 Asset Pricing PrinciplesDocument4 pagesRangkuman Bab 9 Asset Pricing Principlesindah oliviaNo ratings yet

- Module #04 - Risk and Rates ReturnDocument13 pagesModule #04 - Risk and Rates ReturnRhesus UrbanoNo ratings yet

- CH 8Document56 pagesCH 8Sufyan KhanNo ratings yet

- Capital Asset Pricing Mode1Document9 pagesCapital Asset Pricing Mode1Shaloo SidhuNo ratings yet

- Capital Asset Pricing ModelDocument8 pagesCapital Asset Pricing ModelJanani RaniNo ratings yet

- Corp Fin Session 5-6-Risk and ReturnDocument22 pagesCorp Fin Session 5-6-Risk and Returnmansi agrawalNo ratings yet

- CAPM Model ExplainedDocument8 pagesCAPM Model ExplainedAshu158No ratings yet

- Capm 1 PDFDocument8 pagesCapm 1 PDFAbhishek AroraNo ratings yet

- Finance - Chapter-03-Risk in FinanceDocument25 pagesFinance - Chapter-03-Risk in FinanceMehedi HassanNo ratings yet

- Chapter 6 Risk and Return LectureDocument10 pagesChapter 6 Risk and Return LectureAia GarciaNo ratings yet

- CH 7 Portfolio RiskDocument5 pagesCH 7 Portfolio RiskPravin MandoraNo ratings yet

- Sharpe Ratio: R R E (R RDocument17 pagesSharpe Ratio: R R E (R Rvipin gargNo ratings yet

- IIMC Corp Finance 2018-19Document54 pagesIIMC Corp Finance 2018-19Ambuj AgrawalNo ratings yet

- Portfolio Long Ans QuestionDocument5 pagesPortfolio Long Ans QuestionAurora AcharyaNo ratings yet

- Chapter 6Document10 pagesChapter 6Seid KassawNo ratings yet

- What Does Capital Asset Pricing Model - CAPM Mean?Document6 pagesWhat Does Capital Asset Pricing Model - CAPM Mean?nagendraMBANo ratings yet

- Markowitz ModelDocument63 pagesMarkowitz ModeldrramaiyaNo ratings yet

- Standard Deviation and VarianceDocument2 pagesStandard Deviation and VarianceJOshua VillaruzNo ratings yet

- Nama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalDocument15 pagesNama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalAnissa AsyahraNo ratings yet

- Chapter 2Document61 pagesChapter 2Meseret HailemichaelNo ratings yet

- Risk and ReturnDocument57 pagesRisk and ReturnIsmadth2918388No ratings yet

- Portfolio Theory's Key ConceptsDocument7 pagesPortfolio Theory's Key ConceptsaanillllNo ratings yet

- CH 05Document48 pagesCH 05Ali SyedNo ratings yet

- #01 Session1Document36 pages#01 Session1YisraelaNo ratings yet

- Financial Management - Risk and ReturnDocument22 pagesFinancial Management - Risk and ReturnSoledad Perez100% (1)

- The Formula: Security Market Line Systematic RiskDocument7 pagesThe Formula: Security Market Line Systematic RiskPrem Chand BhashkarNo ratings yet

- Advanced Accounting-Volume 2Document4 pagesAdvanced Accounting-Volume 2ronnelson pascual25% (16)

- Lesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestDocument35 pagesLesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestLily DaniaNo ratings yet

- Ethics and Business Week 1Document45 pagesEthics and Business Week 1Lily DaniaNo ratings yet

- Lesson 6: Ethical Decision Making: Employee Rights Ethical Issues in The WorkplaceDocument24 pagesLesson 6: Ethical Decision Making: Employee Rights Ethical Issues in The WorkplaceLily DaniaNo ratings yet

- Exploring Moral Philosophy and Metaethical TheoriesDocument25 pagesExploring Moral Philosophy and Metaethical TheoriesLily DaniaNo ratings yet

- Lesson 3: 1. Philosophy Ethics and BusinessDocument41 pagesLesson 3: 1. Philosophy Ethics and Businessziade roalesNo ratings yet

- Lesson 4Document42 pagesLesson 4Lily DaniaNo ratings yet

- Chapter 7 Advance Accounting Volume 1 2008Document15 pagesChapter 7 Advance Accounting Volume 1 2008andrewhomil_17199886% (7)

- Multiple Choice Answers and Solutions: PAR Boogie BirdieDocument19 pagesMultiple Choice Answers and Solutions: PAR Boogie BirdieNelia Mae S. VillenaNo ratings yet

- Chapter 5-Advance Accounting (Guerrero)Document23 pagesChapter 5-Advance Accounting (Guerrero)Bianca Jane Maaliw63% (8)

- Chapter 2Document25 pagesChapter 2Ronalyn EscamillasNo ratings yet

- Multiple Choice Answers and Solutions: Aquino Locsin David HizonDocument26 pagesMultiple Choice Answers and Solutions: Aquino Locsin David HizonclaudettegasendoNo ratings yet

- Ethics LAW Practice Reason: University of MindanaoDocument22 pagesEthics LAW Practice Reason: University of MindanaoLily DaniaNo ratings yet

- Multiple Choice Answers and Solutions: Reorganization and Troubled Debt Restructuring 135Document9 pagesMultiple Choice Answers and Solutions: Reorganization and Troubled Debt Restructuring 135Nelia Mae S. VillenaNo ratings yet

- Chapter 7Document8 pagesChapter 7PattyNo ratings yet

- Chapter 1 Advanced Acctg. SolmanDocument20 pagesChapter 1 Advanced Acctg. SolmanLaraNo ratings yet

- Total Assets of Jessica P4550,000 Total Liabilities Only of Jenny CoDocument17 pagesTotal Assets of Jessica P4550,000 Total Liabilities Only of Jenny CoNelia Mae S. VillenaNo ratings yet

- Chapter 06Document18 pagesChapter 06Gonzales JhayVee100% (1)

- Answers To Cost Accounting Chapter 9Document6 pagesAnswers To Cost Accounting Chapter 9Raffy Roncales0% (1)

- Cost Accounting Answers Chapter 5Document4 pagesCost Accounting Answers Chapter 5Raffy Roncales76% (25)

- Chapter 03Document9 pagesChapter 03Gonzales JhayVeeNo ratings yet

- Cost Accounting Answers Chapter 4Document17 pagesCost Accounting Answers Chapter 4Raffy RoncalesNo ratings yet

- Answers To Cost Accounting Chapter 10Document15 pagesAnswers To Cost Accounting Chapter 10Raffy Roncales100% (2)

- Cost Accounting Answer Chapter 2 PDFDocument5 pagesCost Accounting Answer Chapter 2 PDFangel cruz0% (1)

- Financial Markets and Institutions Chapter OverviewDocument13 pagesFinancial Markets and Institutions Chapter OverviewKareyn Ann SumayloNo ratings yet

- Chapter 1 - Sol Man de LeonDocument1 pageChapter 1 - Sol Man de LeonJungkookie BaeNo ratings yet

- Chapter-8 de Leon 2014Document4 pagesChapter-8 de Leon 2014'Jaurie'TwentyFour86% (7)

- 14single EntryDocument4 pages14single EntryLily DaniaNo ratings yet

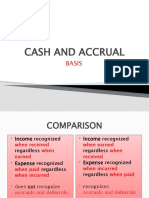

- 13cash and AccrualDocument6 pages13cash and AccrualLily DaniaNo ratings yet

- 10accounting ChangesDocument31 pages10accounting ChangesLily DaniaNo ratings yet

- 1 Aka 57Document4 pages1 Aka 57Richard FadhilahNo ratings yet

- The Innovator's Secret WeaponDocument9 pagesThe Innovator's Secret WeaponNaval VaswaniNo ratings yet

- Assignment On New Economic EnviornmentDocument13 pagesAssignment On New Economic EnviornmentPrakash KumawatNo ratings yet

- Book of AbstractsDocument156 pagesBook of Abstractsdragance106No ratings yet

- 1988 Ojhri Camp Disaster in PakistanDocument3 pages1988 Ojhri Camp Disaster in PakistanranasohailiqbalNo ratings yet

- Readme P006Document7 pagesReadme P006paras99No ratings yet

- Stafford Beer - The World We ManageDocument12 pagesStafford Beer - The World We ManageRaoul LundbergNo ratings yet

- Acefyl SPP - 03 Dec 2010Document54 pagesAcefyl SPP - 03 Dec 2010maliakbar111No ratings yet

- Chapter 6 Coming of SpainDocument4 pagesChapter 6 Coming of SpainJayvee MacapagalNo ratings yet

- Fulbright-Hays Dissertation Research AbroadDocument8 pagesFulbright-Hays Dissertation Research AbroadHelpMeWriteMyPaperPortSaintLucie100% (1)

- Nursing Care PlansDocument7 pagesNursing Care PlansNicholaiCabadduNo ratings yet

- Kotler Mm15e Inppt 12Document26 pagesKotler Mm15e Inppt 12aldi_unantoNo ratings yet

- Problems of Education in The 21st Century, Vol. 76, No. 3, 2018Document137 pagesProblems of Education in The 21st Century, Vol. 76, No. 3, 2018Scientia Socialis, Ltd.No ratings yet

- Sept 2013 NewsletterDocument6 pagesSept 2013 NewsletterBKU1965No ratings yet

- Netflix PPT by OopsieanieeDocument12 pagesNetflix PPT by OopsieanieeAdhimurizkyrNo ratings yet

- Module 1 MC4 LOGIC CRITICAL THINKINGDocument6 pagesModule 1 MC4 LOGIC CRITICAL THINKINGAubrey Ante100% (1)

- Analisis Debussy PDFDocument2 pagesAnalisis Debussy PDFMiguel SeoaneNo ratings yet

- Republic Planters Bank Vs CADocument2 pagesRepublic Planters Bank Vs CAMohammad Yusof Mauna MacalandapNo ratings yet

- R69 Sepulveda V PelaezDocument2 pagesR69 Sepulveda V PelaezfranceheartNo ratings yet

- Advanced - Vocabulary, Idioms and MetaphorsDocument3 pagesAdvanced - Vocabulary, Idioms and Metaphorsjustttka100% (3)

- 05 AHP and Scoring ModelsDocument32 pages05 AHP and Scoring ModelsIhjaz VarikkodanNo ratings yet

- Thesis Jur ErbrinkDocument245 pagesThesis Jur Erbrinkgmb09140No ratings yet

- APMP SyllabusDocument20 pagesAPMP SyllabuscapsfastNo ratings yet

- Talent ManagementDocument8 pagesTalent Managementyared haftuNo ratings yet

- 028 - Chapter 6 - L20 PDFDocument11 pages028 - Chapter 6 - L20 PDFRevathiNo ratings yet

- Digital Electronics Boolean Algebra SimplificationDocument72 pagesDigital Electronics Boolean Algebra Simplificationtekalegn barekuNo ratings yet

- Proposal On The Goals For ChangeDocument5 pagesProposal On The Goals For ChangeMelody MhedzyNo ratings yet

- Guia de Instrucciones para Piloto - Garmin 1000Document57 pagesGuia de Instrucciones para Piloto - Garmin 1000Cesar Gaspar BaltazarNo ratings yet

- Magnetic Effects of Current PDFDocument32 pagesMagnetic Effects of Current PDFAdarshNo ratings yet

- Oxford Quantum Theory Lecture NotesDocument92 pagesOxford Quantum Theory Lecture Notest ElderNo ratings yet