You might also like

- New Era University: Inventory Management of Hardware Businesses in Batasan, Quezon CityDocument35 pagesNew Era University: Inventory Management of Hardware Businesses in Batasan, Quezon Citylook porr100% (3)

- Pestle Analysis United Arab EmiratesDocument16 pagesPestle Analysis United Arab EmiratesJacob EdwardsNo ratings yet

- Operations Management AssignmentDocument4 pagesOperations Management AssignmentnidhiNo ratings yet

- Problem For Chapter 3Document3 pagesProblem For Chapter 3Clarisse Angela PostreNo ratings yet

- AFAR 1 Flexible Learning Module Midterm Topic 1 Cost Concepts and Cost BehaviorDocument14 pagesAFAR 1 Flexible Learning Module Midterm Topic 1 Cost Concepts and Cost BehaviorJessica IslaNo ratings yet

- Container Logistics in Paraguay, Terport CaseDocument5 pagesContainer Logistics in Paraguay, Terport CaseJose Grau FigueredoNo ratings yet

- Microeconomics Final ProjectDocument21 pagesMicroeconomics Final Projectapi-227406761100% (2)

- MObile GarageDocument21 pagesMObile Garageanjum malek100% (1)

- Feasabilitysoap FactoryDocument23 pagesFeasabilitysoap FactoryAnjani Kumar Mohanty100% (5)

- Chapter 3 Cost Accounting CycleDocument11 pagesChapter 3 Cost Accounting CycleSteffany RoqueNo ratings yet

- Quiz 2 - Cost AccountingDocument4 pagesQuiz 2 - Cost AccountingDong WestNo ratings yet

- Income StatementDocument20 pagesIncome StatementJasmine HaliliNo ratings yet

- Cost Strategic Management - Chap3Document28 pagesCost Strategic Management - Chap3Alber Howell MagadiaNo ratings yet

- Nacua CAC Unit2 ActivityDocument13 pagesNacua CAC Unit2 ActivityJasper John NacuaNo ratings yet

- Ma. Lyn Bren BS-Entrep 2B Applying Learned ConceptsDocument7 pagesMa. Lyn Bren BS-Entrep 2B Applying Learned Concepts2B Ma. Lyn BrenNo ratings yet

- Three Rules For Safety From Covid: Prepared By:-Ms Tinu AnandDocument21 pagesThree Rules For Safety From Covid: Prepared By:-Ms Tinu AnandPriyanshu singhNo ratings yet

- Quiz 1 Cost Accounting FDocument5 pagesQuiz 1 Cost Accounting Fretchiel love calinogNo ratings yet

- Job Order Costing 16112021 123409pmDocument8 pagesJob Order Costing 16112021 123409pmHassan AliNo ratings yet

- Cost Accounting Cost AccumulationDocument57 pagesCost Accounting Cost AccumulationRoi Martin A. De VeyraNo ratings yet

- Cost Accounting TutorialDocument49 pagesCost Accounting TutorialpreciousegualanNo ratings yet

- Cost AccountingDocument5 pagesCost Accountingretchiel love calinogNo ratings yet

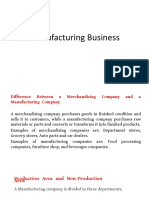

- Manufacturing BusinessDocument18 pagesManufacturing BusinessJeon JeonNo ratings yet

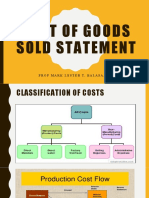

- Statement of COGSDocument3 pagesStatement of COGSIan CalinawanNo ratings yet

- Finished Goods Inventory: Exercise 1-1 (True or False)Document16 pagesFinished Goods Inventory: Exercise 1-1 (True or False)Isaiah BatucanNo ratings yet

- Job Order Costing Work SheetDocument11 pagesJob Order Costing Work SheetEllah MaeNo ratings yet

- Activity 1: Answer and ExplanationsDocument23 pagesActivity 1: Answer and ExplanationsCatherine OrdoNo ratings yet

- Financial Statements ER Problem 2 SolutionDocument11 pagesFinancial Statements ER Problem 2 SolutionSYED ALI SHAH SYED MUKHTIYAR ALINo ratings yet

- Pengelompokan BiayaDocument17 pagesPengelompokan BiayaMaya BangunNo ratings yet

- Module 5 Accounting For Manufacturing BusinessDocument5 pagesModule 5 Accounting For Manufacturing Businessmariella ellaNo ratings yet

- Cost Accounting MidDocument7 pagesCost Accounting MidHuma NadeemNo ratings yet

- Mod7 Part 2 Manufacturing OperationsDocument24 pagesMod7 Part 2 Manufacturing Operationsmarjorie magsinoNo ratings yet

- Principles of Accounting, Volume 2: Managerial AccountingDocument59 pagesPrinciples of Accounting, Volume 2: Managerial AccountingVo VeraNo ratings yet

- Cost Accounting Quiz 4Document4 pagesCost Accounting Quiz 4andreamrieNo ratings yet

- Manufacturing Costs Lecture Version 2 STUDENT VERSIONDocument15 pagesManufacturing Costs Lecture Version 2 STUDENT VERSIONLampel Louise LlandaNo ratings yet

- Cost Accounting Self Assessment Materials Labor and OverheadDocument4 pagesCost Accounting Self Assessment Materials Labor and OverheadDarwyn HonaNo ratings yet

- These Are The Key Points You Should Know For Chapter 1Document7 pagesThese Are The Key Points You Should Know For Chapter 1Jane VillanuevaNo ratings yet

- Manufacturing Account NotesDocument7 pagesManufacturing Account Notesdayna davisNo ratings yet

- Sample Questions - Accounting For OverheadDocument4 pagesSample Questions - Accounting For OverheadRedNo ratings yet

- Cost Accounting. ActivityDocument6 pagesCost Accounting. ActivityReida DelmasNo ratings yet

- Cost of Goods Sold StatementDocument18 pagesCost of Goods Sold StatementCherrylane EdicaNo ratings yet

- Cost Accounting UEMLADocument23 pagesCost Accounting UEMLAMitchie FaustinoNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

- Job Order Costing Cost Flows and External ReportingDocument22 pagesJob Order Costing Cost Flows and External ReportingMomo HiraiNo ratings yet

- Quiz Feb24Document5 pagesQuiz Feb24E RDNo ratings yet

- End of Chapter 1 Exercises - Toralde, Ma - Kristine E.Document7 pagesEnd of Chapter 1 Exercises - Toralde, Ma - Kristine E.Kristine Esplana ToraldeNo ratings yet

- Manufacturing BusinessDocument40 pagesManufacturing BusinesstygurNo ratings yet

- ACC104 - Job Order Costing - For PostingDocument22 pagesACC104 - Job Order Costing - For PostingYesha SibayanNo ratings yet

- Manufacturing Accounts For OnlineDocument12 pagesManufacturing Accounts For OnlineKennedy BwalyaNo ratings yet

- Cost AccountingDocument17 pagesCost AccountingFaisal RafiqNo ratings yet

- Midterm No. One Review: The Equivalent Units of Production For Conversion Costs WereDocument5 pagesMidterm No. One Review: The Equivalent Units of Production For Conversion Costs WereEric AgudeloNo ratings yet

- ACC104 - Fundamentals of Product and Service CostingDocument7 pagesACC104 - Fundamentals of Product and Service CostingZACARIAS, Marc Nickson DG.No ratings yet

- Introduction To Management AccountingDocument10 pagesIntroduction To Management AccountingPatrick Panlilio RetuyaNo ratings yet

- Activity 4 Cost AccountingDocument2 pagesActivity 4 Cost AccountingDe MarcusNo ratings yet

- Principles of Cost Accounting 14EDocument30 pagesPrinciples of Cost Accounting 14Etegegn mogessieNo ratings yet

- Activity 4 - Job Order CostingDocument2 pagesActivity 4 - Job Order CostingBea GarciaNo ratings yet

- 2a. Job Order Costing CRDocument17 pages2a. Job Order Costing CRAnaly Omandac PelayoNo ratings yet

- Cost Sheet Prepation-NotesDocument12 pagesCost Sheet Prepation-NotesSunita BasakNo ratings yet

- Three Rules For Safety From Covid: Prepared By:-Ms Tinu AnandDocument21 pagesThree Rules For Safety From Covid: Prepared By:-Ms Tinu AnandPriyanshu singhNo ratings yet

- Accounting For Manufacturing Cost Accounting Is Defined As A Systematic Set of Procedures For Recording and ReportingDocument5 pagesAccounting For Manufacturing Cost Accounting Is Defined As A Systematic Set of Procedures For Recording and ReportingEdgardo TangalinNo ratings yet

- Module 3 SCMDocument9 pagesModule 3 SCMKhai LaNo ratings yet

- Recording Applied Manufacturing Overhead CostsDocument3 pagesRecording Applied Manufacturing Overhead CostsFran GutierrezNo ratings yet

- Principles of Cost AccountingDocument28 pagesPrinciples of Cost AccountingKristine AlonzoNo ratings yet

- Exercises - ManufacturingDocument7 pagesExercises - ManufacturingRiana CellsNo ratings yet

- Cost Accounting Mastery - 2Document2 pagesCost Accounting Mastery - 2Mark Revarez0% (1)

- Direct Materials Direct Labor: Exercise 2 - Job Order Cost SheetDocument7 pagesDirect Materials Direct Labor: Exercise 2 - Job Order Cost SheetNile Alric AlladoNo ratings yet

- AEC 105 Prelim Study Notes 3 PDFDocument5 pagesAEC 105 Prelim Study Notes 3 PDFlist2lessNo ratings yet

- AEC 105 Prelim Study Notes 1Document4 pagesAEC 105 Prelim Study Notes 1list2lessNo ratings yet

- Ordinary Song: Ralph Jay Triumfo ArrangementDocument6 pagesOrdinary Song: Ralph Jay Triumfo Arrangementlist2lessNo ratings yet

- Passenger Seat: Arr. by Ralph Jay TriumfoDocument11 pagesPassenger Seat: Arr. by Ralph Jay Triumfolist2lessNo ratings yet

- Centre For Distance Education: AssignmentDocument5 pagesCentre For Distance Education: AssignmentCompany BrandNo ratings yet

- Mutasi Statement BRImoDocument6 pagesMutasi Statement BRImoCeklis OkeNo ratings yet

- General Tyre Annual Report June 30 2020 1Document112 pagesGeneral Tyre Annual Report June 30 2020 1M.TalhaNo ratings yet

- Causes of Stock Discrepancy and Impact OnDocument80 pagesCauses of Stock Discrepancy and Impact Onjrwazo100% (4)

- MediaDocument23 pagesMediaNikhil ChaudharyNo ratings yet

- PEC L6 Unit 3 - ExtensionDocument6 pagesPEC L6 Unit 3 - ExtensionNati MNo ratings yet

- Marketing Case Week 8Document1 pageMarketing Case Week 8tharlow maloeNo ratings yet

- 3363 - How To Make $2,000 Per Week With Beyond InfinityDocument10 pages3363 - How To Make $2,000 Per Week With Beyond InfinityBasit OnaopepoNo ratings yet

- Exercise Inventory CostingDocument2 pagesExercise Inventory CostingRatriNo ratings yet

- Product ManagementDocument80 pagesProduct ManagementRishabh JainNo ratings yet

- Purchase Contract For Crane Components - S235040703Document11 pagesPurchase Contract For Crane Components - S235040703Epure GabrielNo ratings yet

- Concrete Plant Pots: Feasibility Study and Job Order CostingDocument25 pagesConcrete Plant Pots: Feasibility Study and Job Order CostingLovely Mae Manuel LacasteNo ratings yet

- Laporan Tahunan Annual Report: PT Yanaprima Hastapersada TBKDocument118 pagesLaporan Tahunan Annual Report: PT Yanaprima Hastapersada TBKSTELLANo ratings yet

- Pocket Setter Sip Italy Vs IMB June 2018 by GiorgioDocument36 pagesPocket Setter Sip Italy Vs IMB June 2018 by GiorgioJuan Carlos Arroyave PosadaNo ratings yet

- Bsa 3a Group 1 Chapter 1 Accounting ResearchDocument3 pagesBsa 3a Group 1 Chapter 1 Accounting ResearchAnjelika ViescaNo ratings yet

- Isp A Company Built On Customer ServiceDocument3 pagesIsp A Company Built On Customer Serviceironmask20041047No ratings yet

- Treas - Payment of Real Property TaxDocument1 pageTreas - Payment of Real Property TaxCristine LectoninNo ratings yet

- HR Trends in 2021: Future of Human Resource Management: Key TakeawaysDocument18 pagesHR Trends in 2021: Future of Human Resource Management: Key TakeawaysNitikaNo ratings yet

- Invoice TableDocument1 pageInvoice Tablesuresh kumarNo ratings yet

- Alert Security V Pasaliwan G.R.182397Document3 pagesAlert Security V Pasaliwan G.R.182397Sjden TumanonNo ratings yet

- Accounting Question BanksDocument130 pagesAccounting Question BanksLinh Trần Khánh100% (1)

- GMW WEP Socio-Economic AssessmentDocument20 pagesGMW WEP Socio-Economic AssessmentTom AlexanderNo ratings yet

- CONEX PLUS INC. - Door Locks MechanismDocument2 pagesCONEX PLUS INC. - Door Locks MechanismDean DumaguingNo ratings yet