You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Cost Accounting AssignmentDocument6 pagesCost Accounting AssignmentCharles BarcelaNo ratings yet

- Costcon 1Document3 pagesCostcon 1Frances Clayne GonzalvoNo ratings yet

- Discussion 3 Accounting Cycle For Manufacturing BusinessDocument12 pagesDiscussion 3 Accounting Cycle For Manufacturing BusinessRHEGIE WAYNE PITOGONo ratings yet

- Orca Share Media1646571581803 6906221771846243726Document12 pagesOrca Share Media1646571581803 6906221771846243726LACONSAY, Nathalie B.No ratings yet

- Cost Sheet ProblemsDocument10 pagesCost Sheet Problemsprapulla sureshNo ratings yet

- Task 1: Cost Classfication Task 1 Has 3 Questions in TotalDocument3 pagesTask 1: Cost Classfication Task 1 Has 3 Questions in TotalNgọc Trâm TrầnNo ratings yet

- Test 1 ProblemsDocument48 pagesTest 1 ProblemsKaira Arora50% (2)

- Accounting QuestionsDocument7 pagesAccounting QuestionsleneNo ratings yet

- Assignment 3 Accounting PDFDocument11 pagesAssignment 3 Accounting PDFjgfjhf arwtr100% (1)

- ExercisesDocument7 pagesExercisesMaryjane De GuzmanNo ratings yet

- Activity 1 COST CONCEPTS AND COST BEHAVIOR problemsDocument8 pagesActivity 1 COST CONCEPTS AND COST BEHAVIOR problemsSittie Ainna A. UnteNo ratings yet

- Assignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR MohsinDocument11 pagesAssignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR Mohsinjgfjhf arwtr100% (1)

- Varnish Company Cost AnalysisDocument4 pagesVarnish Company Cost AnalysisAmiee Laa PulokNo ratings yet

- Cost AccDocument27 pagesCost AccAngel PulvinarNo ratings yet

- Answers to Activity 1 WorksheetDocument5 pagesAnswers to Activity 1 WorksheetjangjangNo ratings yet

- Job Order Costing QuizbowlDocument27 pagesJob Order Costing QuizbowlsarahbeeNo ratings yet

- Cost Management Part 1: Manufacturing Costs and Inventory CalculationsDocument4 pagesCost Management Part 1: Manufacturing Costs and Inventory CalculationsJosh YuuNo ratings yet

- Exercises - ManufacturingDocument7 pagesExercises - ManufacturingRiana CellsNo ratings yet

- Acco 20073 Discussion Sy2122 (Bsma 2-4)Document81 pagesAcco 20073 Discussion Sy2122 (Bsma 2-4)Paul BandolaNo ratings yet

- Acc 202 Exercise MyselfDocument5 pagesAcc 202 Exercise Myselfnhidiepnguyet08112004No ratings yet

- Revision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Document5 pagesRevision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Sujib BarmanNo ratings yet

- Baya - Exercise 4 Job Order Costing, Accounting For MaterialDocument12 pagesBaya - Exercise 4 Job Order Costing, Accounting For MaterialAngelica BayaNo ratings yet

- Job Order Costing MethodsDocument31 pagesJob Order Costing MethodszamanNo ratings yet

- Cost of goods manufactured schedule and product costsDocument3 pagesCost of goods manufactured schedule and product costsshivnilNo ratings yet

- Cost Activity 1Document12 pagesCost Activity 1Dark Ninja100% (1)

- Exercises: Job Order Costing: Q1: Lamonda Corp. Uses A Job Order Cost System. On April 1, The Accounts Had The FollowingDocument4 pagesExercises: Job Order Costing: Q1: Lamonda Corp. Uses A Job Order Cost System. On April 1, The Accounts Had The FollowingCynthia WongNo ratings yet

- Assignment #1Document5 pagesAssignment #1Crizelda BauyonNo ratings yet

- BACOSTMX Module 3 Self-ReviewerDocument5 pagesBACOSTMX Module 3 Self-ReviewerlcNo ratings yet

- Vicenzo Bernard Leandro Tioriman - 01011182025009Document6 pagesVicenzo Bernard Leandro Tioriman - 01011182025009ImVicNo ratings yet

- Direct Materials Direct Labor: Exercise 2 - Job Order Cost SheetDocument7 pagesDirect Materials Direct Labor: Exercise 2 - Job Order Cost SheetNile Alric AlladoNo ratings yet

- Job Order CostingDocument3 pagesJob Order CostingKrizia Mae FloresNo ratings yet

- Notes On Process Costing System - PDF - ProtectedDocument14 pagesNotes On Process Costing System - PDF - Protectedhildamezmur9No ratings yet

- BA 7000 Study Guide 1Document11 pagesBA 7000 Study Guide 1ekachristinerebecaNo ratings yet

- Introduction To Management AccountingDocument10 pagesIntroduction To Management AccountingPatrick Panlilio RetuyaNo ratings yet

- JOC (Discussion)Document10 pagesJOC (Discussion)Luisa ColumbinoNo ratings yet

- Journal Entries and Job Cost SheetsDocument3 pagesJournal Entries and Job Cost SheetsGayzelle MirandaNo ratings yet

- Chapter 1 Question Review - 102Document5 pagesChapter 1 Question Review - 102Mark Joseph CanoNo ratings yet

- Chapter 2 - 1 - IllustrationDocument6 pagesChapter 2 - 1 - IllustrationYonas BamlakuNo ratings yet

- Chapters 1 To 3 (Answers)Document8 pagesChapters 1 To 3 (Answers)Cho AndreaNo ratings yet

- ACC104 - Job Order Costing - For PostingDocument22 pagesACC104 - Job Order Costing - For PostingYesha SibayanNo ratings yet

- ACG 2071 Managerial AccountingDocument31 pagesACG 2071 Managerial AccountingSamantha FernandezNo ratings yet

- Cost Calculation Snowball ManufacturingDocument13 pagesCost Calculation Snowball ManufacturingBisma ShahabNo ratings yet

- Cost Accounting Concepts and CalculationsDocument6 pagesCost Accounting Concepts and CalculationsMuhammad BilalNo ratings yet

- Job Order Costing SolutionDocument9 pagesJob Order Costing SolutionMariah VillanNo ratings yet

- Important Problems With SolutionsDocument5 pagesImportant Problems With SolutionsSahil KumarNo ratings yet

- ManAc Quiz 1Document12 pagesManAc Quiz 1random122No ratings yet

- Problems - Accounting For Factory OverheadDocument3 pagesProblems - Accounting For Factory OverheadShaina Jean PiezonNo ratings yet

- Introduction to Manufacturing Costs and Financial StatementsDocument4 pagesIntroduction to Manufacturing Costs and Financial StatementsAshitero YoNo ratings yet

- To Record Raw Materials Purchased On AccountDocument4 pagesTo Record Raw Materials Purchased On AccountKathleen MercadoNo ratings yet

- Cost Acctg Cycle Activity AnswerDocument2 pagesCost Acctg Cycle Activity AnswerElaine Joyce GarciaNo ratings yet

- Exercises - Job Order CostingDocument7 pagesExercises - Job Order CostingJericho DupayaNo ratings yet

- Sir Syed University of Engineering & Technology: Answer ScriptDocument7 pagesSir Syed University of Engineering & Technology: Answer ScriptWasif FarooqNo ratings yet

- Kunci Jawaban Lab Chapter 3 OverheadDocument3 pagesKunci Jawaban Lab Chapter 3 OverheadRantiyaniNo ratings yet

- JOB ORDER COSTING-Production LossesDocument7 pagesJOB ORDER COSTING-Production LossesJude TadiosNo ratings yet

- Job Order CostingDocument4 pagesJob Order CostingTrina Mae BarrogaNo ratings yet

- Problem 1:: Job Order CostingDocument4 pagesProblem 1:: Job Order CostingTrina Mae BarrogaNo ratings yet

- ManAcc Quiz 2Document13 pagesManAcc Quiz 2Deepannita ChakrabortyNo ratings yet

- Accounting For Managers Canadian 1st Edition Collier Solutions ManualDocument17 pagesAccounting For Managers Canadian 1st Edition Collier Solutions Manualnicholassmithyrmkajxiet100% (24)

- Comparative Vs Absolute AdvantageDocument15 pagesComparative Vs Absolute AdvantageRingle JobNo ratings yet

- CPI-GNP Approaches-1Document36 pagesCPI-GNP Approaches-1Reida DelmasNo ratings yet

- Trade PolicyDocument34 pagesTrade PolicyReida DelmasNo ratings yet

- Export & ImportDocument7 pagesExport & ImportReida DelmasNo ratings yet

- Introduction To IMF-1Document53 pagesIntroduction To IMF-1Reida DelmasNo ratings yet

- Acquire New Knowledge at UC with Philosophy, Vision, Mission and Core ValuesDocument39 pagesAcquire New Knowledge at UC with Philosophy, Vision, Mission and Core ValuesReida DelmasNo ratings yet

- PE MidtermDocument10 pagesPE MidtermReida DelmasNo ratings yet

- Finals PEDocument12 pagesFinals PEReida DelmasNo ratings yet

- Stock Market CrashDocument10 pagesStock Market Crashapi-710564150No ratings yet

- GFM Mock QuestionsDocument13 pagesGFM Mock QuestionsBhanu TejaNo ratings yet

- Assignment Ishan SharmaDocument8 pagesAssignment Ishan SharmaIshan SharmaNo ratings yet

- Managerial and Financial AccountingDocument42 pagesManagerial and Financial AccountingRodrigo de Oliveira LeiteNo ratings yet

- AFO+ +Mock+TestDocument12 pagesAFO+ +Mock+TestArrow NagNo ratings yet

- Southeast Asian Views On The United States - Perceptions Versus Objective Reality - FULCRUMDocument13 pagesSoutheast Asian Views On The United States - Perceptions Versus Objective Reality - FULCRUMshotatekenNo ratings yet

- Kathryn Newman Chapter 6 Questions 1 16Document3 pagesKathryn Newman Chapter 6 Questions 1 16Kim FloresNo ratings yet

- Walmart's Supply Chain SuccessDocument4 pagesWalmart's Supply Chain Successmaximillan njagiNo ratings yet

- CH 7 Costs of ProductionDocument42 pagesCH 7 Costs of Productionanon_670361819No ratings yet

- Reasong QuesDocument3 pagesReasong QuesAmitoz SinghNo ratings yet

- Self-Check Activities: Thinking BeyondDocument3 pagesSelf-Check Activities: Thinking BeyondAngelie Shan NavarroNo ratings yet

- Mirjana Radović-Marković, Borislav Đukonović - Macroeconomics of Western Balkans in The Context of The Global Work and Business Environment-Information Age Publishing (2022)Document180 pagesMirjana Radović-Marković, Borislav Đukonović - Macroeconomics of Western Balkans in The Context of The Global Work and Business Environment-Information Age Publishing (2022)pakor79No ratings yet

- Strategy Guide: IndexDocument13 pagesStrategy Guide: Indexdeepak777No ratings yet

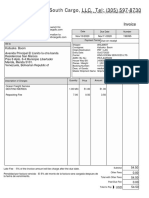

- South Cargo, LLC. Tel: (305) 597-8730: InvoiceDocument1 pageSouth Cargo, LLC. Tel: (305) 597-8730: InvoiceChevyveronaNo ratings yet

- Larfarge-22 ArDocument302 pagesLarfarge-22 ArLou VreNo ratings yet

- 11 Risk and ReturnDocument11 pages11 Risk and ReturnHarinder SinghNo ratings yet

- Hocmai TOEIC 450 Word Formation PracticeDocument5 pagesHocmai TOEIC 450 Word Formation PracticeDụ ThụNo ratings yet

- FDD Monograph Crisis in LebanonDocument57 pagesFDD Monograph Crisis in LebanonAnderson Bellido QuicañoNo ratings yet

- Sem II Transportation Economics N EvaluationDocument2 pagesSem II Transportation Economics N EvaluationDwijendra ChanumoluNo ratings yet

- Proforma - 121093Document1 pageProforma - 121093rudramaafia770No ratings yet

- Strategic Management Midterm Exam Question B Answer-2Document3 pagesStrategic Management Midterm Exam Question B Answer-2Aayush AgarwalNo ratings yet

- RA No. 10667Document16 pagesRA No. 10667Sab Amantillo BorromeoNo ratings yet

- Chapter 19Document32 pagesChapter 19Phuong Vy PhamNo ratings yet

- Bopp FilmsDocument4 pagesBopp FilmsHimanshuNo ratings yet

- Different Organization Structures 11111Document3 pagesDifferent Organization Structures 11111Đức LợiNo ratings yet

- Economics PYQ SSCDocument48 pagesEconomics PYQ SSCNitin Vishwakarma100% (1)

- IGCSE-OL - Bus - CH - 3 - Answers To CB ActivitiesDocument3 pagesIGCSE-OL - Bus - CH - 3 - Answers To CB ActivitiesAdrián CastilloNo ratings yet

- Corrugated Paper BoxDocument13 pagesCorrugated Paper BoxGulfCartonNo ratings yet

- SubDocument1,452 pagesSubA MNo ratings yet

- Chapter-6 - Importing, Exporting and Trade Relations-1Document12 pagesChapter-6 - Importing, Exporting and Trade Relations-1Lysss EpssssNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)