You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Sta. Maria-San Pedro Elementary School: Statement of AccountDocument4 pagesSta. Maria-San Pedro Elementary School: Statement of AccountCriselda AdameNo ratings yet

- Milton Friedman 50 Years Later EbookDocument147 pagesMilton Friedman 50 Years Later EbookVitor Hazin100% (2)

- Annual Procurement Plan 2020-21.Document7 pagesAnnual Procurement Plan 2020-21.alibuxjatoiNo ratings yet

- A Review and Study On Stabilization of Expansive Soil Using Brick DustDocument8 pagesA Review and Study On Stabilization of Expansive Soil Using Brick DustalibuxjatoiNo ratings yet

- Use of Brick Dust and Fly Ash As A Soil Stabilizer: November 2019Document5 pagesUse of Brick Dust and Fly Ash As A Soil Stabilizer: November 2019alibuxjatoiNo ratings yet

- Determinants of Profitability of Islamic Banks, A Case Study of PakistanDocument15 pagesDeterminants of Profitability of Islamic Banks, A Case Study of PakistanalibuxjatoiNo ratings yet

- Effect of Marble Dust and Burnt Brick DuDocument3 pagesEffect of Marble Dust and Burnt Brick DualibuxjatoiNo ratings yet

- Ber PDFDocument1 pageBer PDFalibuxjatoiNo ratings yet

- 10 Companies Detail Before SolverDocument72 pages10 Companies Detail Before SolveralibuxjatoiNo ratings yet

- Types of RainfallDocument2 pagesTypes of RainfallalibuxjatoiNo ratings yet

- Attendance Sheets Technical & FinancialDocument4 pagesAttendance Sheets Technical & FinancialalibuxjatoiNo ratings yet

- What Do You Know About Pavement Design and Its Types? Also Differentiate Between Flexible and Rigid PavementDocument5 pagesWhat Do You Know About Pavement Design and Its Types? Also Differentiate Between Flexible and Rigid PavementalibuxjatoiNo ratings yet

- PAVEMENTS Design Course OutlineDocument2 pagesPAVEMENTS Design Course OutlinealibuxjatoiNo ratings yet

- Steel Properties: Engr: Muhammad Yasir Samoo BE Civil MUET JamshoroDocument10 pagesSteel Properties: Engr: Muhammad Yasir Samoo BE Civil MUET JamshoroalibuxjatoiNo ratings yet

- What Is A 'Mean-Variance Analysis'Document2 pagesWhat Is A 'Mean-Variance Analysis'alibuxjatoiNo ratings yet

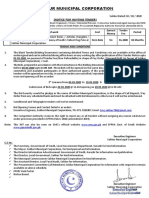

- Sukkur Municipal Corporation: (Notice For Inviting Tender)Document1 pageSukkur Municipal Corporation: (Notice For Inviting Tender)alibuxjatoiNo ratings yet

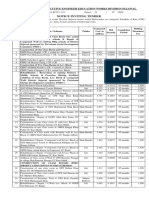

- Notice Inviting Tender: Office of The Executive Engineer Education Works Division SujawalDocument4 pagesNotice Inviting Tender: Office of The Executive Engineer Education Works Division SujawalalibuxjatoiNo ratings yet

- General Abstract PDFDocument8 pagesGeneral Abstract PDFalibuxjatoiNo ratings yet

- Banks Investment in Govt Securities Rises To Rs6.33trDocument2 pagesBanks Investment in Govt Securities Rises To Rs6.33tralibuxjatoiNo ratings yet

- Chapter 4Document28 pagesChapter 4Nhi Phan TúNo ratings yet

- APISWA Report 280923 DigitalDocument31 pagesAPISWA Report 280923 DigitaldashaNo ratings yet

- Dr. Amitabh MishraDocument36 pagesDr. Amitabh MishrameenasarathaNo ratings yet

- IBO 1 - 10yearsDocument37 pagesIBO 1 - 10yearsManuNo ratings yet

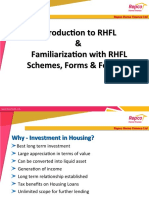

- New RHFL Schemes & Forms - May 2022Document36 pagesNew RHFL Schemes & Forms - May 2022Surya PmlNo ratings yet

- Apic S03Document1 pageApic S03Christiam Ortega100% (2)

- Hkcee Economics - 3.4 Unit Tax - P.1Document5 pagesHkcee Economics - 3.4 Unit Tax - P.1Toby ChengNo ratings yet

- How To Read The Balance SheetDocument13 pagesHow To Read The Balance SheetbalajitrNo ratings yet

- Mark and Spencer Excel For Calc - 130319 FINAL DRAFTDocument12 pagesMark and Spencer Excel For Calc - 130319 FINAL DRAFTRama KediaNo ratings yet

- Eefc Account1Document15 pagesEefc Account1navneet bagriNo ratings yet

- Penilaian Kualitas Kinerja Keuangan Perusahaan PerDocument16 pagesPenilaian Kualitas Kinerja Keuangan Perusahaan PerCABE GEMINGNo ratings yet

- QUIZ AKL - I Semester I TA 2019/2020Document6 pagesQUIZ AKL - I Semester I TA 2019/2020Bob Ahsan FikaNo ratings yet

- Tugas Chapter 2Document2 pagesTugas Chapter 2ALIA TUNGGA DEWINo ratings yet

- ECO121 - Test 02 - Individual Assignment 02 Lê TH DGDocument5 pagesECO121 - Test 02 - Individual Assignment 02 Lê TH DGThuy DuonggNo ratings yet

- Eureka Enterprises Inc Manufactures Bathroom Fixtures The StocDocument1 pageEureka Enterprises Inc Manufactures Bathroom Fixtures The StocM Bilal SaleemNo ratings yet

- MICRO AND SMALL ProjectDocument17 pagesMICRO AND SMALL ProjectJapgur Kaur100% (1)

- Financial Management Economics For Finance 2023 1671444579Document26 pagesFinancial Management Economics For Finance 2023 1671444579RADHIKANo ratings yet

- In This Chapter, Look For The Answers To These Questions:: Chapter 11 Public Goods and Common ResourcesDocument20 pagesIn This Chapter, Look For The Answers To These Questions:: Chapter 11 Public Goods and Common Resourcesco lamNo ratings yet

- Crop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationDocument3 pagesCrop and Water Productivity, Energy Auditing, Carbon Footprints and Soil Health Indicators of Bt-Cotton Transplanting Led System IntensificationAmanNo ratings yet

- Contract Summary PT Bumi Medika Indonesia For Pustu MeradaDocument2 pagesContract Summary PT Bumi Medika Indonesia For Pustu MeradaLingkaNo ratings yet

- IMS Proschool IFRS EbookDocument143 pagesIMS Proschool IFRS EbookhariinshrNo ratings yet

- Jcien.2023.176.2.web Small-20230420121947Document52 pagesJcien.2023.176.2.web Small-20230420121947Ashutosh Chandra DwivediNo ratings yet

- CH 1a - Introduction To Supply Chain & Logistics ManagementDocument31 pagesCH 1a - Introduction To Supply Chain & Logistics ManagementHamza SaleemNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument43 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- Msvi Final ProjectDocument19 pagesMsvi Final ProjectAreeb KhanNo ratings yet

- Ephrem Birhanu Final Thesis11Document99 pagesEphrem Birhanu Final Thesis11teklil tiganiNo ratings yet

- Transfer Pricing: Mcgraw-Hill/IrwinDocument38 pagesTransfer Pricing: Mcgraw-Hill/IrwinBusiness MatterNo ratings yet

- Intuition DiscountingDocument56 pagesIntuition DiscountingklklNo ratings yet