You might also like

- July StatementDocument2 pagesJuly Statementalys100% (1)

- BitcoinDocument2 pagesBitcoinNadiminty Mahesh0% (1)

- Fintech Laws and Regulations 2023Document19 pagesFintech Laws and Regulations 2023PREX WEXNo ratings yet

- Factors driving digitalization in bankingDocument18 pagesFactors driving digitalization in bankingप्रवीण घिमिरेNo ratings yet

- Amna Tariq (Fintech) 2Document7 pagesAmna Tariq (Fintech) 2Amna TariqNo ratings yet

- Shared Service Business PlanDocument10 pagesShared Service Business PlanBerkti GetuNo ratings yet

- Mobile Money and PSBDocument4 pagesMobile Money and PSBmaheshnaNo ratings yet

- Digitalization in Banking and Factors That Makes It More CompellingDocument18 pagesDigitalization in Banking and Factors That Makes It More CompellingJaljala NirmanNo ratings yet

- Fintech Ecosystem Fintech Start-Ups FintechDocument2 pagesFintech Ecosystem Fintech Start-Ups FintechTimNo ratings yet

- PARADIGM SHIFT IN BANKING THROUGH FINTECHDocument3 pagesPARADIGM SHIFT IN BANKING THROUGH FINTECHAbdullah AssilNo ratings yet

- Digital Financial Services (DFS) Challenge Facility Digital Financial Services (DFS) - Innovation Challenge Facility InnovationDocument10 pagesDigital Financial Services (DFS) Challenge Facility Digital Financial Services (DFS) - Innovation Challenge Facility InnovationSyed Abbas Haider ZaidiNo ratings yet

- Article On Cashless IndiaDocument9 pagesArticle On Cashless Indiavk sarangdevotNo ratings yet

- Digital Payments Transformation Roadmap ReportDocument44 pagesDigital Payments Transformation Roadmap ReportChris aribasNo ratings yet

- The E-Zwich Electronic Clearing and Payment System David Andreas Hesse AccraDocument5 pagesThe E-Zwich Electronic Clearing and Payment System David Andreas Hesse AccraahialeybbNo ratings yet

- Electronic Banking Uganda 2021Document15 pagesElectronic Banking Uganda 2021mugambwadenis99No ratings yet

- Financial InclusionDocument6 pagesFinancial InclusionsignNo ratings yet

- Payment Systems Review Jan-Mar 2013 Quarterly Growth TrendsDocument5 pagesPayment Systems Review Jan-Mar 2013 Quarterly Growth TrendsSibtain JiwaniNo ratings yet

- Rural Financial Inclusions Through Digital Banking Services in IndiaDocument4 pagesRural Financial Inclusions Through Digital Banking Services in IndiaShishir GuptaNo ratings yet

- Financial Sector Deepening Ethiopia Blog - Mobile Money in EthiopiaDocument6 pagesFinancial Sector Deepening Ethiopia Blog - Mobile Money in EthiopiaMehari GizachewNo ratings yet

- RESEARCH The Effect of Cashless TransactDocument13 pagesRESEARCH The Effect of Cashless TransactSabrina LouiseNo ratings yet

- Business Proposal For Using Fintech in Banking ArenaDocument4 pagesBusiness Proposal For Using Fintech in Banking ArenawoosanNo ratings yet

- Southeast Asia Coming of The Digital Challenger BanksDocument21 pagesSoutheast Asia Coming of The Digital Challenger BanksSubhro SenguptaNo ratings yet

- Mobile Banking: A Boon For unbanked-IIDocument3 pagesMobile Banking: A Boon For unbanked-IIsrujalshahNo ratings yet

- Scope of Digital Payment SystemDocument7 pagesScope of Digital Payment Systemsameer shaikhNo ratings yet

- Providing Means of Payment For Today and For The FutureDocument6 pagesProviding Means of Payment For Today and For The FutureAyesha KhanNo ratings yet

- Increase-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToDocument3 pagesIncrease-The Government's Encouragement To Use Electronic Wallets Has Contributed Much ToMahima SharmaNo ratings yet

- Fintech-banking sectorDocument17 pagesFintech-banking sectorhimanshu bhattNo ratings yet

- An Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFDocument9 pagesAn Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFAjiboye TooniNo ratings yet

- Fintech Case StudyDocument5 pagesFintech Case StudyAMIT KUMAR CHAUHAN100% (1)

- From Cash To QR Codes - ThunesDocument17 pagesFrom Cash To QR Codes - ThunestamlqNo ratings yet

- Sotir 2015Document73 pagesSotir 2015Emeka EruokwuNo ratings yet

- FIN 401 Final Report BodyDocument9 pagesFIN 401 Final Report Body1711........100% (1)

- Hillsmbero 1Document36 pagesHillsmbero 1pmthogoNo ratings yet

- UPI For Feature Phones - Blog - BhavyaDocument5 pagesUPI For Feature Phones - Blog - BhavyaBhavya SolankiNo ratings yet

- Opportunities and Challenges of FinTech PDFDocument7 pagesOpportunities and Challenges of FinTech PDFviadjbvdNo ratings yet

- Opportunities and Challenges of FintechDocument7 pagesOpportunities and Challenges of FintechMayuri RawatNo ratings yet

- Mobile Money Part of The African Financial Inclusion SolutionDocument6 pagesMobile Money Part of The African Financial Inclusion SolutionAdedNo ratings yet

- Moico - ACT1 - FINANCIAL INNOVATIONSDocument4 pagesMoico - ACT1 - FINANCIAL INNOVATIONSAlliànca Elijah MoicoNo ratings yet

- Current Situation of Mobile Financial ServicesDocument7 pagesCurrent Situation of Mobile Financial ServicesRafsan KhondokerNo ratings yet

- Report Desertation 1 (1) 2Document49 pagesReport Desertation 1 (1) 2Walter tawanda MusosaNo ratings yet

- FinTech Transforming Consumer BankingDocument10 pagesFinTech Transforming Consumer BankingAhmed Abd El GawadNo ratings yet

- Group 4 BVCR ReportDocument36 pagesGroup 4 BVCR ReportUtkarsh BansalNo ratings yet

- Digital Banking in India4Document6 pagesDigital Banking in India4loganx91No ratings yet

- Asian Economic Policy Review - 2022 - Morgan - Fintech and Financial Inclusion in Southeast Asia and IndiaDocument26 pagesAsian Economic Policy Review - 2022 - Morgan - Fintech and Financial Inclusion in Southeast Asia and IndiaFelicia Wong Shing YingNo ratings yet

- Fintech ProjectDocument11 pagesFintech ProjectJaveria UmarNo ratings yet

- Recent Trends in BankingDocument4 pagesRecent Trends in Bankingsuresh50% (2)

- Asynchronous Assignment Bank Management: Submitted byDocument6 pagesAsynchronous Assignment Bank Management: Submitted bytanyaNo ratings yet

- Banking Project: Name-Sanika Patil Class - Fybcom Div-B ROLL NO - 216Document15 pagesBanking Project: Name-Sanika Patil Class - Fybcom Div-B ROLL NO - 216sanika patilNo ratings yet

- Fin TechDocument7 pagesFin TechHarsh ChaudharyNo ratings yet

- The Current Scenario of Fin-Tech in The World and Also in BangladeshDocument2 pagesThe Current Scenario of Fin-Tech in The World and Also in BangladeshBarkat UllahNo ratings yet

- The Future of FinanceDocument30 pagesThe Future of FinanceRenuka SharmaNo ratings yet

- virgo_proposalDocument8 pagesvirgo_proposalWalterNo ratings yet

- Fintech: Bitcoin EY's 2017 Fintech Adoption IndexDocument5 pagesFintech: Bitcoin EY's 2017 Fintech Adoption IndexAkanksha KadamNo ratings yet

- Research Desertation For Walter 1stDocument66 pagesResearch Desertation For Walter 1stWalter tawanda MusosaNo ratings yet

- Employee Convenience Center Project ReportDocument30 pagesEmployee Convenience Center Project ReportMaxPanduNo ratings yet

- BS Adfree 19.05.2019Document9 pagesBS Adfree 19.05.2019Battula Surender SudhamaNo ratings yet

- Effect of Financial Innovation On Credit Risk (Non - Performing Loan Ratios) of Commercial Banks in KenyaDocument8 pagesEffect of Financial Innovation On Credit Risk (Non - Performing Loan Ratios) of Commercial Banks in KenyaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Digital Transformatioin FinanceDocument15 pagesDigital Transformatioin FinancesuhitaNo ratings yet

- Regulation of Digital Financial Services Against Cyber CrimeDocument15 pagesRegulation of Digital Financial Services Against Cyber CrimecpamutuiNo ratings yet

- Pakista 2Document2 pagesPakista 2Undaunted SpiritNo ratings yet

- Gtbank ProposalDocument18 pagesGtbank Proposalmeaudmajor majwalaNo ratings yet

- Nigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Document11 pagesNigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Ajiboye JosephNo ratings yet

- Nigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Document11 pagesNigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Ajiboye JosephNo ratings yet

- Nigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Document11 pagesNigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Ajiboye JosephNo ratings yet

- In The Simplest Form, I Want To Believe This Would Be My Most Basic ResponsibilitiesDocument2 pagesIn The Simplest Form, I Want To Believe This Would Be My Most Basic ResponsibilitiesAjiboye JosephNo ratings yet

- The African Software Engineering Pay LandscapeDocument12 pagesThe African Software Engineering Pay LandscapeAjiboye JosephNo ratings yet

- The African Engineering Pay Landscape2Document18 pagesThe African Engineering Pay Landscape2Ajiboye JosephNo ratings yet

- Nigeria, Ghana, Kenya, Egypt and South AfricaDocument3 pagesNigeria, Ghana, Kenya, Egypt and South AfricaAjiboye JosephNo ratings yet

- In The Simplest Form, I Want To Believe This Would Be My Most Basic ResponsibilitiesDocument2 pagesIn The Simplest Form, I Want To Believe This Would Be My Most Basic ResponsibilitiesAjiboye JosephNo ratings yet

- How To Redeem Insta VouchersDocument1 pageHow To Redeem Insta VouchersSanthoshini ChitluriNo ratings yet

- SWIFT FIN Payment Format Guide For European AcctsDocument19 pagesSWIFT FIN Payment Format Guide For European AcctsShivaji ManeNo ratings yet

- Lista Longvie Emp Afines Venc 01-04-12 PDFDocument3 pagesLista Longvie Emp Afines Venc 01-04-12 PDFMauro PepeNo ratings yet

- Payment Systems Department: Head Office, Dhaka 1000Document6 pagesPayment Systems Department: Head Office, Dhaka 1000Ashok Chandra HalderNo ratings yet

- UNITED AUTOMOBILES VEHICLE PRICE LIST AND ACCESSORIESDocument1 pageUNITED AUTOMOBILES VEHICLE PRICE LIST AND ACCESSORIESRishabh MahajanNo ratings yet

- Close ICICI Bank Demat AccountDocument1 pageClose ICICI Bank Demat AccountP Venu Gopala RaoNo ratings yet

- Schedule of ChargesDocument11 pagesSchedule of ChargesMuhammad Rakibul IslamNo ratings yet

- Direct DebitDocument13 pagesDirect DebitAbdi NamoNo ratings yet

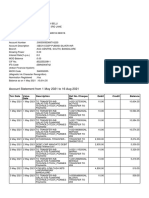

- Account Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceLoan LoanNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHiten AhirNo ratings yet

- Application of Online Payment Method ProposalDocument3 pagesApplication of Online Payment Method ProposalTrang Vu Ha QTKD-3KT-17No ratings yet

- IDRBT Launches Chief Analytics Officers ForumDocument28 pagesIDRBT Launches Chief Analytics Officers Forumvaraprasad_ganjiNo ratings yet

- 7college - Du.ac - BD Admission Apply Pay 2017032830Document1 page7college - Du.ac - BD Admission Apply Pay 2017032830Dhoni Khan0% (1)

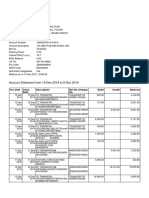

- Casa Statement 201028130002457 PDFDocument2 pagesCasa Statement 201028130002457 PDFSiti MariamNo ratings yet

- Cross-border payment service application detailsDocument1 pageCross-border payment service application detailsAnkur VermaNo ratings yet

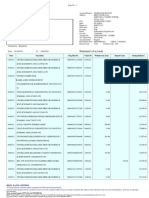

- Transaction Statement SummaryDocument13 pagesTransaction Statement SummaryMohammad Farhan Roll 16No ratings yet

- Jiofiber Postpaid Bill FormatDocument2 pagesJiofiber Postpaid Bill FormatMohit Jain0% (1)

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument29 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceawadhNo ratings yet

- Western Union tutorial for earning moneyDocument2 pagesWestern Union tutorial for earning moneyjoseph100% (7)

- Briefing Guide July Week2&3 Metrobank EMVCardsDocument3 pagesBriefing Guide July Week2&3 Metrobank EMVCardsRafael-Cheryl Tupas-LimboNo ratings yet

- Verifone Vx670 ManualDocument36 pagesVerifone Vx670 ManualC-Ayelen GirolaNo ratings yet

- E StatementDocument3 pagesE StatementTimmy Sze0% (1)

- Virtual Visa and Mastercard Cards GuideDocument36 pagesVirtual Visa and Mastercard Cards GuideReinier Hernández AvilaNo ratings yet

- Estatement20190415 000638169 PDFDocument2 pagesEstatement20190415 000638169 PDFZaki ZafriNo ratings yet

- PFMS PaymentDocument14 pagesPFMS PaymentDTO HailakandiNo ratings yet

- S 610Document15 pagesS 610najeemNo ratings yet

- Detailed Statement: SearchDocument2 pagesDetailed Statement: SearchSomasekharNo ratings yet

- CA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Document21 pagesCA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Palani Muthusamy100% (1)