You might also like

- Dev Evidence of CitizenshipDocument84 pagesDev Evidence of CitizenshipElisabeth JohnsonNo ratings yet

- Skilled Nominated Visa (Subclass 190) Document ChecklistDocument6 pagesSkilled Nominated Visa (Subclass 190) Document ChecklistChoon Hua100% (1)

- Problems On Internal ReconstructionDocument24 pagesProblems On Internal ReconstructionYashodhan Mithare100% (5)

- DB Aabefiffggea0x040ADocument2 pagesDB Aabefiffggea0x040AKhabirIslamNo ratings yet

- Heirs of Fabillar vs. Paler (Filiation)Document2 pagesHeirs of Fabillar vs. Paler (Filiation)Ariane EspinaNo ratings yet

- Conflicts of law-SALONGADocument84 pagesConflicts of law-SALONGAPrincess ParasNo ratings yet

- 05 Medina v. ValdellonDocument2 pages05 Medina v. Valdellonkmand_lustregNo ratings yet

- Defence Cross Examination Can Be in This Manner To PW1Document3 pagesDefence Cross Examination Can Be in This Manner To PW1Arjita SinghNo ratings yet

- OJT FormsDocument14 pagesOJT FormsJad OrdonioNo ratings yet

- Petition For Appointment As Notary Public 1Document9 pagesPetition For Appointment As Notary Public 1Lou Nonoi Tan100% (1)

- Statutory Construction MidtermsDocument2 pagesStatutory Construction MidtermsmagenNo ratings yet

- 2.2e Coating Formulation CalculationDocument6 pages2.2e Coating Formulation CalculationNitesh Shah100% (2)

- Accounting-Bonus Issue and Right-Issue-1653399117076303Document17 pagesAccounting-Bonus Issue and Right-Issue-1653399117076303Badhrinath ShanmugamNo ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- Xii Accountancy Question Bank 1Document46 pagesXii Accountancy Question Bank 1KavoNo ratings yet

- Presentation On Internal ReconstructionDocument23 pagesPresentation On Internal Reconstructionneeru79200040% (5)

- Marking Scheme Sample Question Paper Accountancy, Class XII Board Examination, March, 2015Document13 pagesMarking Scheme Sample Question Paper Accountancy, Class XII Board Examination, March, 2015kamalNo ratings yet

- Corporate AccountingDocument93 pagesCorporate AccountingKalp JainNo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- QUESTION PAPER 36195 (Solution)Document17 pagesQUESTION PAPER 36195 (Solution)Faizu KhamNo ratings yet

- 637617311650478425SM Session12Document4 pages637617311650478425SM Session12kreshmith2No ratings yet

- Internal ReconsrtuctionDocument33 pagesInternal ReconsrtuctionRenuNo ratings yet

- 5 6084915055709651012Document8 pages5 6084915055709651012Ajit Yadav100% (1)

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- 637617309804853146SM Session10Document3 pages637617309804853146SM Session10kreshmith2No ratings yet

- Shares & Debentures TestDocument10 pagesShares & Debentures TestAthul Krishna KNo ratings yet

- 12 Accountancy Accounting For Share Capital and Debenture Impq 1Document8 pages12 Accountancy Accounting For Share Capital and Debenture Impq 1Aejaz MohamedNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Internal ReconstructionDocument8 pagesInternal Reconstructionsmit9993No ratings yet

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Internal Reconstruction Part-IIDocument13 pagesInternal Reconstruction Part-IIINTER SMARTIANSNo ratings yet

- 12 Accountancy Lyp 2017 Delhi Set1 PDFDocument39 pages12 Accountancy Lyp 2017 Delhi Set1 PDFAshish GangwalNo ratings yet

- Internal Reconstruction P-1 Liabilities Rs Assets RsDocument8 pagesInternal Reconstruction P-1 Liabilities Rs Assets RsPaulomi LahaNo ratings yet

- 5 Internal ReconstructionDocument31 pages5 Internal ReconstructionHariom PatidarNo ratings yet

- Redemption of Preference SharesDocument13 pagesRedemption of Preference Sharessunil agarwalNo ratings yet

- Internal Reconstruction NotesDocument16 pagesInternal Reconstruction NotesAkash Mehta100% (1)

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- Model Test Paper-5Document26 pagesModel Test Paper-5Lavagreat The greatNo ratings yet

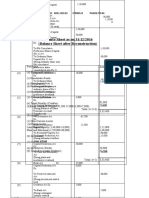

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Document8 pagesBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNo ratings yet

- Dwaraka Doss Goverdhan Doss Vaishnav College (Autonomous) Arumbakkam, Chennai - 600 106. Department of Corporate Secretaryship Core Paper V-Corporate AccountingDocument4 pagesDwaraka Doss Goverdhan Doss Vaishnav College (Autonomous) Arumbakkam, Chennai - 600 106. Department of Corporate Secretaryship Core Paper V-Corporate AccountingNeeraj DNo ratings yet

- 12 Accountancy sp07Document26 pages12 Accountancy sp07vivekdaiv55No ratings yet

- Question SheetDocument2 pagesQuestion SheetHarsh DubeNo ratings yet

- Accountancy 12 SapnleDocument21 pagesAccountancy 12 Sapnlemohit pandeyNo ratings yet

- Marking Scheme PRE-BOARD (2009-10) : Part ADocument9 pagesMarking Scheme PRE-BOARD (2009-10) : Part AIsha KembhaviNo ratings yet

- 1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033Document21 pages1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033jiya.mehra.2306No ratings yet

- 12 Accountancy Lyp 2017 Foreign Set3Document41 pages12 Accountancy Lyp 2017 Foreign Set3Ashish GangwalNo ratings yet

- K VJa Pfa CYOae 91 JFTLNCDocument17 pagesK VJa Pfa CYOae 91 JFTLNCAshwin MurthyNo ratings yet

- Accounts 2Document41 pagesAccounts 2SubodhSaxenaNo ratings yet

- 12 Accountancy sp06Document28 pages12 Accountancy sp06Jaydev JaydevNo ratings yet

- MS Accountancy PB Xii Set 2Document9 pagesMS Accountancy PB Xii Set 2DakshitaNo ratings yet

- Forfeiture of Shares Cancellation of Shareholders Name From Register of Company Due To Non - Payment of First and Final Call Money On 200 SharesDocument3 pagesForfeiture of Shares Cancellation of Shareholders Name From Register of Company Due To Non - Payment of First and Final Call Money On 200 SharesAarya KhedekarNo ratings yet

- DK Goal 6Document52 pagesDK Goal 6sahiltiwariii225No ratings yet

- Pany Accounts - 8Document10 pagesPany Accounts - 8Aaditya SaratheNo ratings yet

- Corporate Accounting Exam Questions PaperDocument7 pagesCorporate Accounting Exam Questions PaperAmmar Bin NasirNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Sample Question Paper Accountancy (055) Class-Xii 2016 Time Allowed - Three Hours Max Marks 80Document21 pagesSample Question Paper Accountancy (055) Class-Xii 2016 Time Allowed - Three Hours Max Marks 80mohit pandeyNo ratings yet

- CBSE 12 Accountancy 2017-1Document21 pagesCBSE 12 Accountancy 2017-1mohit pandeyNo ratings yet

- Problem No.: 1 (March 2018) Assets : Solution.: - Capital Reduction A/CDocument3 pagesProblem No.: 1 (March 2018) Assets : Solution.: - Capital Reduction A/CAnshrNo ratings yet

- Unit 3 Retirement of A Partner - Problems With AnswersDocument13 pagesUnit 3 Retirement of A Partner - Problems With Answersds1619231No ratings yet

- Dissolution With Journal Entries For Winter CampDocument10 pagesDissolution With Journal Entries For Winter CampDev RathiNo ratings yet

- Accountancy Set 3 Ms - DocxDocument7 pagesAccountancy Set 3 Ms - DocxKunal GauravNo ratings yet

- R21 Capital Budgeting Q Bank PDFDocument10 pagesR21 Capital Budgeting Q Bank PDFZidane KhanNo ratings yet

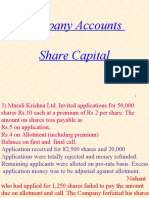

- Problems On Issue of SharesDocument8 pagesProblems On Issue of SharesgeddadaarunNo ratings yet

- XII Acc SQP 1 (AP 23-24)Document11 pagesXII Acc SQP 1 (AP 23-24)Vaidehi BagraNo ratings yet

- 11 Redemption of Preference SharesDocument6 pages11 Redemption of Preference SharesRohith KumarNo ratings yet

- Ans. Chapter-9Document6 pagesAns. Chapter-9upscmindworksNo ratings yet

- 12 Accountancy Lyp 2017 Outside Delhi Set1 PDFDocument42 pages12 Accountancy Lyp 2017 Outside Delhi Set1 PDFAshish GangwalNo ratings yet

- Toward a National Eco-compensation Regulation in the People's Republic of ChinaFrom EverandToward a National Eco-compensation Regulation in the People's Republic of ChinaNo ratings yet

- Ansay vs. DBPDocument2 pagesAnsay vs. DBPGendale Am-isNo ratings yet

- Sworn Statement of Assets, Liabilities and Net WorthDocument3 pagesSworn Statement of Assets, Liabilities and Net WorthSanta Dela Cruz NaluzNo ratings yet

- La Economía Social de Mercado. Orígenes e Intérpretes. Flavio FeliceDocument16 pagesLa Economía Social de Mercado. Orígenes e Intérpretes. Flavio FeliceJuan Pablo SerraNo ratings yet

- 416E Backhoe Loader Single Tilt Center Pivot, Powered by 3054C Engine (SEBP3701 - 45) - SwingDocument2 pages416E Backhoe Loader Single Tilt Center Pivot, Powered by 3054C Engine (SEBP3701 - 45) - Swingmanuel230387No ratings yet

- Brault PerraultDocument6 pagesBrault Perraultgrtela100% (2)

- Physics ElasticityDocument23 pagesPhysics ElasticityDaniel Danille KristianNo ratings yet

- RizalDocument6 pagesRizalcresha mae necesario100% (1)

- Boticano V Chu DigestDocument1 pageBoticano V Chu DigestJermone MuaripNo ratings yet

- VOL. 270, MARCH 26, 1997 503: China Banking Corporation vs. Court of AppealsDocument21 pagesVOL. 270, MARCH 26, 1997 503: China Banking Corporation vs. Court of AppealsElizabeth Jade D. CalaorNo ratings yet

- B.A.LL.B. Sem IX - Land Law - Question Paper April 2016Document2 pagesB.A.LL.B. Sem IX - Land Law - Question Paper April 2016salve786No ratings yet

- CT DUFf SDX9 NPQEd CDocument10 pagesCT DUFf SDX9 NPQEd C19ME094 S.Suresh KumarNo ratings yet

- Comprehensive ProblemDocument2 pagesComprehensive ProblemErik NavarroNo ratings yet

- Easo Application Form 20151Document11 pagesEaso Application Form 20151Ioana IoanaNo ratings yet

- Tax Audit Form 3CDDocument18 pagesTax Audit Form 3CDaishwarya raikarNo ratings yet

- Article 2 The Teacher and The StateDocument17 pagesArticle 2 The Teacher and The StateMelissa PummaNo ratings yet

- Senator Jinggoy Ejercito EstradaDocument7 pagesSenator Jinggoy Ejercito EstradaNatsudeeNo ratings yet

- YES - Show Guide Elizabeth WongDocument2 pagesYES - Show Guide Elizabeth WongalamsekitarselangorNo ratings yet

- Ca FoundationDocument16 pagesCa Foundationsuresh prasadNo ratings yet

- The Standard 07.05.2014Document80 pagesThe Standard 07.05.2014Zachary Monroe67% (3)