You might also like

- CPA Audit NotesDocument136 pagesCPA Audit NotesRamachNo ratings yet

- Auditing For Non-AccountantsDocument229 pagesAuditing For Non-AccountantsRheneir Mora100% (2)

- Auditing Notes - Chapter 3Document24 pagesAuditing Notes - Chapter 3Future CPA100% (7)

- Master Budget With AnswersDocument13 pagesMaster Budget With AnswersCillian Reeves75% (4)

- Audit Body of KnowledgeDocument51 pagesAudit Body of Knowledgeadelayounis100% (1)

- At.3006-Planning An Audit of Financial StatementsDocument5 pagesAt.3006-Planning An Audit of Financial StatementsSadAccountantNo ratings yet

- Mathematics: Quarter 4 - Module 5Document25 pagesMathematics: Quarter 4 - Module 5Cillian Reeves50% (2)

- Math10 3RDQUARTER Module-5Document24 pagesMath10 3RDQUARTER Module-5Cillian Reeves100% (2)

- Auditing Theory Material For DLSU Dasma - Batch 21 - StudentsDocument41 pagesAuditing Theory Material For DLSU Dasma - Batch 21 - StudentsMa. BeatriceNo ratings yet

- CH 1 Quiz With AnswersDocument7 pagesCH 1 Quiz With AnswersBeverly Ann Caparoso100% (3)

- AT Quizzer 6 - Planning and Risk Assessment PDFDocument18 pagesAT Quizzer 6 - Planning and Risk Assessment PDFJimmyChao0% (1)

- Cameron MctaggartDocument2 pagesCameron MctaggartJoao SousaNo ratings yet

- Needs and Expectations, Turtle ChartDocument1 pageNeeds and Expectations, Turtle ChartChiheb GNo ratings yet

- II - Audit Strategy, PlanningDocument8 pagesII - Audit Strategy, PlanningAlphy maria cherianNo ratings yet

- Mathematics: Quarter 3 - Module 2Document24 pagesMathematics: Quarter 3 - Module 2Cillian Reeves0% (1)

- Mathematics: Quarter 4 - Module 6Document21 pagesMathematics: Quarter 4 - Module 6Cillian Reeves100% (1)

- Zig Ziglars Secrets of Closing The Sale PDFDocument10 pagesZig Ziglars Secrets of Closing The Sale PDFhuguesNo ratings yet

- Corporate Governance Complete ProjectDocument21 pagesCorporate Governance Complete ProjectEswar Stark100% (1)

- Auditing Theory ReviewerDocument9 pagesAuditing Theory ReviewerChristian MaritoNo ratings yet

- ASR Quizzer 6 - Planning and Risk AssessmenttDocument18 pagesASR Quizzer 6 - Planning and Risk AssessmenttInsatiable LifeNo ratings yet

- Assets User GuideDocument36 pagesAssets User GuidemohdbilalmaqsoodNo ratings yet

- Handouts For Credit TransactionsDocument15 pagesHandouts For Credit TransactionsIrene Sheeran100% (1)

- Classic Theories of Economic Development: Four Approaches: Linear Stages TheoryDocument4 pagesClassic Theories of Economic Development: Four Approaches: Linear Stages TheoryCillian ReevesNo ratings yet

- Employment ContractDocument2 pagesEmployment ContractLoucienne Leigh Diestro100% (1)

- AUD 1.2 Client Acceptance and PlanningDocument10 pagesAUD 1.2 Client Acceptance and PlanningAimee Cute100% (1)

- Lesson 2 Quiz MaterialDocument4 pagesLesson 2 Quiz Materiallinkin soyNo ratings yet

- OutlineDocument9 pagesOutlineMARIA THERESA ABRIONo ratings yet

- Chapter 4 - Overview of Audit Process and Preliminary ActivitiesDocument42 pagesChapter 4 - Overview of Audit Process and Preliminary ActivitiesCarlos Miguel MendozaNo ratings yet

- 07 FS Audit Process - Audit PlanningDocument6 pages07 FS Audit Process - Audit Planningrandomlungs121223No ratings yet

- Chapter - 2 "Audit Strategy, Planning & Execution": Lecture - 18Document6 pagesChapter - 2 "Audit Strategy, Planning & Execution": Lecture - 18Aruna RajappaNo ratings yet

- Topic 5 - Planning, Risk Assessment and Audit RiskDocument20 pagesTopic 5 - Planning, Risk Assessment and Audit RiskSandile Henry DlaminiNo ratings yet

- Multiple Choice QuestionsDocument3 pagesMultiple Choice QuestionsEjoyce KimNo ratings yet

- Audit Uas SGDocument6 pagesAudit Uas SGJung JessicaNo ratings yet

- HO2-A - Risk-Based Audit of Financial Statements Part 1 (Overview) - RevisedDocument8 pagesHO2-A - Risk-Based Audit of Financial Statements Part 1 (Overview) - RevisedJaynalyn MonasterialNo ratings yet

- Overview of Working Papers in RAMDocument21 pagesOverview of Working Papers in RAMIsha PopNo ratings yet

- Lecture 16 - Standards On Auditing (SA 300 and 315)Document8 pagesLecture 16 - Standards On Auditing (SA 300 and 315)Aruna RajappaNo ratings yet

- Fam Chapter 6 21092005Document15 pagesFam Chapter 6 21092005Humayoun Ahmad FarooqiNo ratings yet

- Apd 1 NotesDocument8 pagesApd 1 NotesHelios HexNo ratings yet

- Chapter 7: Audit PlanningDocument7 pagesChapter 7: Audit PlanningAngela RamosNo ratings yet

- Class Notes 6-8Document11 pagesClass Notes 6-8Omnia HassanNo ratings yet

- CH 2 - Audit StrategyDocument10 pagesCH 2 - Audit StrategyvedthkNo ratings yet

- Chapter TwoDocument38 pagesChapter TwoGemechu GuduNo ratings yet

- (Effective October 2006 Examination) : The Cpa Licensure Examination Syllabus - Auditing TheoryDocument7 pages(Effective October 2006 Examination) : The Cpa Licensure Examination Syllabus - Auditing TheoryJanine Bernadette C. Bautista3180270No ratings yet

- Ch-2 Audit PlanningDocument3 pagesCh-2 Audit PlanningSavya Sachi100% (1)

- Audit Strategy, Audit Planning and Audit ProgrammeDocument9 pagesAudit Strategy, Audit Planning and Audit ProgrammePrachi GuptaNo ratings yet

- A3 - Topic 1Document7 pagesA3 - Topic 1jgames777No ratings yet

- PSA 200 - Bravo, Carol Sarah O.Document5 pagesPSA 200 - Bravo, Carol Sarah O.Jonas MondalaNo ratings yet

- Aud Theory ReviewerDocument6 pagesAud Theory ReviewerPhia TeoNo ratings yet

- Auditing Reviewer 3 Auditing Reviewer 3Document4 pagesAuditing Reviewer 3 Auditing Reviewer 3Ryan PedroNo ratings yet

- E BookDocument5 pagesE BookSavit BansalNo ratings yet

- Modern Auditing: Modern AuditingDocument26 pagesModern Auditing: Modern AuditingIbnu Rasyid HamidiNo ratings yet

- Auditing Theory Chapter 9 Summary NotesDocument10 pagesAuditing Theory Chapter 9 Summary NotesJwyneth Royce DenolanNo ratings yet

- DocDocument3 pagesDocMarvine MagaddatuNo ratings yet

- A424 Chapter 10: Primary Concern To Auditors?Document6 pagesA424 Chapter 10: Primary Concern To Auditors?mohammad.mamdooh9472No ratings yet

- AT Quiz 2 - B1Document3 pagesAT Quiz 2 - B1AMNo ratings yet

- Audit PlanningDocument46 pagesAudit PlanninglaronrichelleeNo ratings yet

- This Study Resource WasDocument9 pagesThis Study Resource Wasvenice cambryNo ratings yet

- Sa 200 "Overall Objectives of The Independent Auditor and Conduct of Audit in Accordance With Sas"Document5 pagesSa 200 "Overall Objectives of The Independent Auditor and Conduct of Audit in Accordance With Sas"Padsariya SureshNo ratings yet

- ICPA Audit Planning HandoutDocument4 pagesICPA Audit Planning Handoutmichelle angela maramagNo ratings yet

- 2 Multiple ChoiceDocument57 pages2 Multiple ChoiceMichael Brian TorresNo ratings yet

- Session 7 - AUDITING AND ASSURANCE PRINCIPLESDocument31 pagesSession 7 - AUDITING AND ASSURANCE PRINCIPLESSharjaaahNo ratings yet

- Chapter8 ReviewerDocument18 pagesChapter8 Reviewermisonim.eNo ratings yet

- AT.3203 Audit Responsibilities and ObjectivesDocument5 pagesAT.3203 Audit Responsibilities and ObjectivesNancy Jane LaurelNo ratings yet

- Audit Phase IDocument48 pagesAudit Phase Iadi darmawanNo ratings yet

- ACCT 3109 - Auditing: Professional Auditing Standards and The Audit Opinion Formulation ProcessDocument50 pagesACCT 3109 - Auditing: Professional Auditing Standards and The Audit Opinion Formulation ProcessChung CFNo ratings yet

- Audit Process-OverviewDocument5 pagesAudit Process-OverviewJennelyn CapenditNo ratings yet

- AT05-Planning An Audit of Financial StatementsDocument11 pagesAT05-Planning An Audit of Financial StatementsZyrelle DelgadoNo ratings yet

- Excel Professional Services, Inc.: Discussion QuestionsDocument5 pagesExcel Professional Services, Inc.: Discussion QuestionskæsiiiNo ratings yet

- Chapter - 3Document8 pagesChapter - 3ApuNo ratings yet

- 10 Risk Assessment & Response To Assessed RisksDocument6 pages10 Risk Assessment & Response To Assessed Risksrandomlungs121223No ratings yet

- Super Summary Auditing Assurance StandardssDocument23 pagesSuper Summary Auditing Assurance StandardssRishabh GuptaNo ratings yet

- Application Controls and General ControlsDocument65 pagesApplication Controls and General ControlsCillian ReevesNo ratings yet

- Controlling Database Management Systems: Access ControlsDocument6 pagesControlling Database Management Systems: Access ControlsCillian ReevesNo ratings yet

- Self Assessment-Partnership LiquidationDocument54 pagesSelf Assessment-Partnership LiquidationCillian Reeves0% (1)

- Taxation Services - TAX RETURN PREPARATION - Involve Assisting Clients With Their Tax Reporting ObligationsDocument15 pagesTaxation Services - TAX RETURN PREPARATION - Involve Assisting Clients With Their Tax Reporting ObligationsCillian ReevesNo ratings yet

- Master Budget ProblemDocument2 pagesMaster Budget ProblemCillian ReevesNo ratings yet

- Mathematics: Quarter 3 - Module 3Document24 pagesMathematics: Quarter 3 - Module 3Cillian ReevesNo ratings yet

- Installment Sales AccountingDocument9 pagesInstallment Sales AccountingCillian ReevesNo ratings yet

- Efficient Market Hypothesis Also Referred To As The Theory of Efficient Capital Markets States ThatDocument3 pagesEfficient Market Hypothesis Also Referred To As The Theory of Efficient Capital Markets States ThatCillian ReevesNo ratings yet

- Mansci 1Document25 pagesMansci 1Cillian ReevesNo ratings yet

- Effective Rate-WPS OfficeDocument1 pageEffective Rate-WPS OfficeCillian ReevesNo ratings yet

- Standard CostingDocument19 pagesStandard CostingCillian ReevesNo ratings yet

- Master Budget ProblemDocument2 pagesMaster Budget ProblemCillian ReevesNo ratings yet

- College of Accountancy and FinanceDocument2 pagesCollege of Accountancy and FinanceMike BadilloNo ratings yet

- Deductible Vs Excess (Insurance)Document1 pageDeductible Vs Excess (Insurance)gopinathan_karuthedaNo ratings yet

- April 7, 2022Document12 pagesApril 7, 2022Rina EscaladaNo ratings yet

- Paper 4 Jeff BezosDocument5 pagesPaper 4 Jeff Bezosapi-535584932100% (1)

- Unit 6 (Workbook) : 6A-Love in The SupermarketDocument4 pagesUnit 6 (Workbook) : 6A-Love in The SupermarketLưu Văn SángNo ratings yet

- Customer StatementDocument20 pagesCustomer StatementDonaldNo ratings yet

- Electronic Banking and Employees' Job Security in Lafia Nasarawa State, Nigeria Taiwo Olusegun AdelaniDocument19 pagesElectronic Banking and Employees' Job Security in Lafia Nasarawa State, Nigeria Taiwo Olusegun AdelaniNayab AkhtarNo ratings yet

- Automobile Corporation of Goa LTD: Federal-Mogul Goetze (India) LTDDocument4 pagesAutomobile Corporation of Goa LTD: Federal-Mogul Goetze (India) LTDShashikant VaidyanathanNo ratings yet

- Sbaa1504 - Business Policy and Strategy - Unit Ii - PPT (3) 2Document55 pagesSbaa1504 - Business Policy and Strategy - Unit Ii - PPT (3) 2abcdNo ratings yet

- 3-1I Feasibility StudyDocument36 pages3-1I Feasibility StudytesfaNo ratings yet

- Energy Investment Opportunities 2019Document51 pagesEnergy Investment Opportunities 2019Marce MangaoangNo ratings yet

- Let's Create Local and Global Ads: Activity 2: Home Business! Lead inDocument3 pagesLet's Create Local and Global Ads: Activity 2: Home Business! Lead inwendy barillasNo ratings yet

- Iffco at A GlanceDocument74 pagesIffco at A Glancelokesharya1No ratings yet

- Unit 1: Module 1 BA121 Basic MicroeconomicsDocument8 pagesUnit 1: Module 1 BA121 Basic Microeconomicsnek ocinrocNo ratings yet

- mgt613 Mega Files of McqsssDocument203 pagesmgt613 Mega Files of McqsssSalman SikandarNo ratings yet

- AER Presentation On RAB MultiplesDocument18 pagesAER Presentation On RAB MultiplesKGNo ratings yet

- Proposed Research Topic On Retail IndustriesDocument12 pagesProposed Research Topic On Retail Industriesparuaru0767% (9)

- Paul Clement Resignation Letter - King and SpaldingDocument2 pagesPaul Clement Resignation Letter - King and SpaldingjoshblackmanNo ratings yet

- Price List Grand I10 Nios DT 01.05.2022Document1 pagePrice List Grand I10 Nios DT 01.05.2022VijayNo ratings yet

- Entrep Week 1-3 ReviewerDocument7 pagesEntrep Week 1-3 ReviewerdelpinadoelaineNo ratings yet

- Role of CRM in MarketingDocument19 pagesRole of CRM in MarketingVivek Kumar Gupta86% (14)

- 2021 Annual Member StatementDocument9 pages2021 Annual Member Statementkz2w4tx6prNo ratings yet

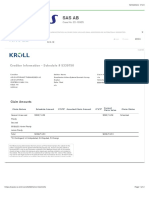

- Kroll Restructuring AdministrationDocument2 pagesKroll Restructuring AdministrationMarNo ratings yet