You might also like

- CH 1 Assignment - An Overview of Financial Management PDFDocument13 pagesCH 1 Assignment - An Overview of Financial Management PDFPhil SingletonNo ratings yet

- Acquisition valuation of Talbros AutomotiveDocument9 pagesAcquisition valuation of Talbros Automotivetech& GamingNo ratings yet

- Financial Management AssignmentDocument16 pagesFinancial Management AssignmentNishant goyalNo ratings yet

- JSC Student Roll ListDocument50 pagesJSC Student Roll Listprits1310No ratings yet

- Nestle Pakistan Project Report by Dilawer Askari - 180795Document16 pagesNestle Pakistan Project Report by Dilawer Askari - 180795mirza dilawerNo ratings yet

- Financial Reporting ProjectDocument11 pagesFinancial Reporting Projecttech& GamingNo ratings yet

- OR Test of Solvency: (A) Liquidity RatiosDocument24 pagesOR Test of Solvency: (A) Liquidity RatiosshivaniNo ratings yet

- Liquidity Ratios AnalysisDocument10 pagesLiquidity Ratios Analysistech& GamingNo ratings yet

- Name: Hammad Ali (180811) Class: BSAF 4A Submitted To: Sir Khalid Subject: Financial Reporting 2Document14 pagesName: Hammad Ali (180811) Class: BSAF 4A Submitted To: Sir Khalid Subject: Financial Reporting 2tech& GamingNo ratings yet

- Ratio AnalysisDocument8 pagesRatio AnalysisikramNo ratings yet

- FinalReport On Financial Health of Company With Suggested Measures For Improvement NithishaDocument15 pagesFinalReport On Financial Health of Company With Suggested Measures For Improvement NithishaShiva Sai VikasNo ratings yet

- Financial Management Mid Term Kirti, ShailjaDocument46 pagesFinancial Management Mid Term Kirti, ShailjaShailja JajodiaNo ratings yet

- Finance Project: Sir Usman AkmalDocument51 pagesFinance Project: Sir Usman AkmalRehan AbdullahNo ratings yet

- GAIL 2015 Financial Ratio AnalysisDocument8 pagesGAIL 2015 Financial Ratio AnalysisVarun PatelNo ratings yet

- Data Analysis and InterpretationDocument27 pagesData Analysis and InterpretationeshuNo ratings yet

- Ratio Analysis ReviewDocument9 pagesRatio Analysis ReviewmuhammadTzNo ratings yet

- Ratio Analysis: D.G. Khan Cement Company LTDDocument59 pagesRatio Analysis: D.G. Khan Cement Company LTDrizwan ziaNo ratings yet

- Template FM ProjectDocument32 pagesTemplate FM Projectsana shahidNo ratings yet

- Analysis Onn FisDocument8 pagesAnalysis Onn Fistungeena waseemNo ratings yet

- Project: Packages LimitedDocument10 pagesProject: Packages LimitedAleena IdreesNo ratings yet

- Ass1 AuditDocument10 pagesAss1 AuditMoinNo ratings yet

- Reasons For Collapse of BanksDocument25 pagesReasons For Collapse of BanksMichael VuhaNo ratings yet

- Analyzing Liquidity Ratios and Working Capital of a CompanyDocument5 pagesAnalyzing Liquidity Ratios and Working Capital of a CompanyJoanna Pauline GamboaNo ratings yet

- Cadbury Ratio AnalysisDocument11 pagesCadbury Ratio AnalysisShanza Maryam100% (1)

- Adani ports and Special Economic Zone Ltd. company profileDocument29 pagesAdani ports and Special Economic Zone Ltd. company profileRohith NNo ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisSandesha Weerasinghe0% (1)

- Cash Conversion Cycle of Rafhan Maize ProductsDocument5 pagesCash Conversion Cycle of Rafhan Maize Productsmuhammad farhanNo ratings yet

- 1) Current Ratio:: FormulaDocument6 pages1) Current Ratio:: FormulaniceprachiNo ratings yet

- Financial RatiosDocument8 pagesFinancial Ratios21AD01 - ABISHEK JNo ratings yet

- Liquidity Ratios: Current RatioDocument19 pagesLiquidity Ratios: Current RatiovarunNo ratings yet

- Analyse Activity Ratios of CompanyDocument8 pagesAnalyse Activity Ratios of CompanyGudise Divya BharathiNo ratings yet

- Ratio Analysis of Sainsbury PLCDocument4 pagesRatio Analysis of Sainsbury PLCshuvossNo ratings yet

- Capitaland CoDocument11 pagesCapitaland CoLucas ThuitaNo ratings yet

- Unilever Financial AnalysisDocument6 pagesUnilever Financial AnalysisMehwish IlyasNo ratings yet

- FishboneDocument5 pagesFishboneGhibran MaulanaNo ratings yet

- ANALYZING LIQUIDITY AND PROFITABILITY RATIOSDocument7 pagesANALYZING LIQUIDITY AND PROFITABILITY RATIOShamnah lateefNo ratings yet

- Submitted To: Sir Adeel NasirDocument21 pagesSubmitted To: Sir Adeel NasirshEikh umArNo ratings yet

- Financial Statement Ratios Reveal DBE Gurney's PerformanceDocument18 pagesFinancial Statement Ratios Reveal DBE Gurney's PerformancePohyun YongNo ratings yet

- Financial Ratios Analysis of Nestle 2013-2015Document20 pagesFinancial Ratios Analysis of Nestle 2013-2015Hebatallah FahmyNo ratings yet

- Project: Flying Cement CompanyDocument21 pagesProject: Flying Cement CompanyAleena IdreesNo ratings yet

- Searle Company Ratio Analysis 2010 2011 2012Document63 pagesSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasNo ratings yet

- Financial Analysis: RevenueDocument9 pagesFinancial Analysis: RevenueMaithri Vidana KariyakaranageNo ratings yet

- Ratio Analysis of "RAK Ceramics" and "Shinepukur Ceramics" 2011-2015Document34 pagesRatio Analysis of "RAK Ceramics" and "Shinepukur Ceramics" 2011-2015SAEID RAHMAN100% (2)

- University of Swabi: Group Leader:-Awais Ali (02) Group Members: - Waqas Ali (05) Sohail IqbalDocument23 pagesUniversity of Swabi: Group Leader:-Awais Ali (02) Group Members: - Waqas Ali (05) Sohail IqbalFarhan IsrarNo ratings yet

- Ratio - Dutch LadyDocument7 pagesRatio - Dutch Ladyushanthini santhirasegarNo ratings yet

- Inventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andDocument23 pagesInventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andrajendranSelviNo ratings yet

- Measurement LevelsDocument67 pagesMeasurement LevelsEllixander LanuzoNo ratings yet

- Ratio Analysis of Company Report (2012/13) : Short Term Solvency Ratios/liquidity RatiosDocument8 pagesRatio Analysis of Company Report (2012/13) : Short Term Solvency Ratios/liquidity RatiosRehan AbdullahNo ratings yet

- Financial Ratio Analysis: L'Oreal vs Unilever & Estee LauderDocument8 pagesFinancial Ratio Analysis: L'Oreal vs Unilever & Estee LauderFasha RoslanNo ratings yet

- Submitted To Khuram ShaffiDocument12 pagesSubmitted To Khuram Shaffiharis meerNo ratings yet

- Financial Ratios Analysis of NestleDocument17 pagesFinancial Ratios Analysis of NestleKAINAT MUSHTAQNo ratings yet

- Financial Ratios Analysis of Nestle: 1062474@adu - Ac.aeDocument17 pagesFinancial Ratios Analysis of Nestle: 1062474@adu - Ac.aeAqsaNo ratings yet

- Financial Ratios Analysis of NestleDocument17 pagesFinancial Ratios Analysis of NestleAnuj SharmaNo ratings yet

- Nestle Financial Analysis RatiosDocument17 pagesNestle Financial Analysis RatiosUsman MaqboolNo ratings yet

- Financial Ratios Analysis of Nestle: 1062474@adu - Ac.aeDocument17 pagesFinancial Ratios Analysis of Nestle: 1062474@adu - Ac.aeHager SalahNo ratings yet

- Document Karthi Ratio - 5 - 16.5Document10 pagesDocument Karthi Ratio - 5 - 16.5raj kumarNo ratings yet

- Assignment Fin516Document26 pagesAssignment Fin516mumtaz.aliNo ratings yet

- Liquidity RatioDocument3 pagesLiquidity RatioTanya JunejaNo ratings yet

- KATHMANDU UNIVERSITY SCHOOL OF MANAGEMENTDocument32 pagesKATHMANDU UNIVERSITY SCHOOL OF MANAGEMENTShuvam DotelNo ratings yet

- ICI Pakistan Today: Looking Ahead To TomorrowDocument13 pagesICI Pakistan Today: Looking Ahead To TomorrowAmna FarooquiNo ratings yet

- Working Capital & Dividend PolicyDocument9 pagesWorking Capital & Dividend PolicyLipi Singal0% (1)

- A Study On Financial AnalysisDocument37 pagesA Study On Financial AnalysisVarun KumarNo ratings yet

- Strategic Managemet Project On JazzDocument2 pagesStrategic Managemet Project On Jazztech& GamingNo ratings yet

- Least Square MethodDocument2 pagesLeast Square Methodtech& GamingNo ratings yet

- Group AssignmentDocument6 pagesGroup Assignmenttech& GamingNo ratings yet

- Mad ErrorDocument2 pagesMad Errortech& GamingNo ratings yet

- Time Series AnalysisDocument3 pagesTime Series Analysistech& GamingNo ratings yet

- Operations ManagementDocument3 pagesOperations Managementtech& GamingNo ratings yet

- Seasonal IndicesDocument2 pagesSeasonal Indicestech& GamingNo ratings yet

- Assignment 2Document2 pagesAssignment 2tech& GamingNo ratings yet

- Netflix International Expansion SWOT Analysis and Strategic RecommendationsDocument4 pagesNetflix International Expansion SWOT Analysis and Strategic Recommendationstech& GamingNo ratings yet

- Investment and Portfolio Management Assignment 1Document7 pagesInvestment and Portfolio Management Assignment 1tech& GamingNo ratings yet

- Corp Governance Assignment PDFDocument3 pagesCorp Governance Assignment PDFtech& GamingNo ratings yet

- IF Quiz 2Document2 pagesIF Quiz 2tech& GamingNo ratings yet

- United Food Pakistan Balance SheetDocument34 pagesUnited Food Pakistan Balance Sheettech& GamingNo ratings yet

- Student Name: Usman AftabDocument4 pagesStudent Name: Usman Aftabtech& GamingNo ratings yet

- Business Ethics AssignmentDocument2 pagesBusiness Ethics Assignmenttech& GamingNo ratings yet

- Corp Governance Assignment PDFDocument3 pagesCorp Governance Assignment PDFtech& GamingNo ratings yet

- 2013 2014 2015 Income Statement: Total ExpensesDocument5 pages2013 2014 2015 Income Statement: Total Expensestech& GamingNo ratings yet

- Ethics Quiz 4Document2 pagesEthics Quiz 4tech& GamingNo ratings yet

- Advance Tax AssignmentDocument1 pageAdvance Tax Assignmenttech& GamingNo ratings yet

- Altman Z-Score Altman Z-Score: Fauji Fertilizer Company 2019 National Foods Company 2019Document4 pagesAltman Z-Score Altman Z-Score: Fauji Fertilizer Company 2019 National Foods Company 2019tech& GamingNo ratings yet

- Justice and Fairness (Jails/Prisoners)Document3 pagesJustice and Fairness (Jails/Prisoners)tech& GamingNo ratings yet

- Understand Pakistan's Tax Amnesty SchemesDocument2 pagesUnderstand Pakistan's Tax Amnesty Schemestech& GamingNo ratings yet

- International Finance Assignment 01Document3 pagesInternational Finance Assignment 01tech& GamingNo ratings yet

- OM Project 2021 OM Project 2021: July 4Document3 pagesOM Project 2021 OM Project 2021: July 4tech& GamingNo ratings yet

- Student ID: Usman Aftab 180759Document2 pagesStudent ID: Usman Aftab 180759tech& GamingNo ratings yet

- Investment and Portfolio Management Assignment 1Document7 pagesInvestment and Portfolio Management Assignment 1tech& GamingNo ratings yet

- OM Quiz 1Document2 pagesOM Quiz 1tech& GamingNo ratings yet

- Usman Aftab 180759 Tax AssignmentDocument4 pagesUsman Aftab 180759 Tax Assignmenttech& GamingNo ratings yet

- Assignment 3: Mobile Robotics Masters of Electrical Engineering (Ai)Document7 pagesAssignment 3: Mobile Robotics Masters of Electrical Engineering (Ai)tech& GamingNo ratings yet

- Mid Term Test in International MarketingDocument9 pagesMid Term Test in International MarketingTron TrxNo ratings yet

- 101 Ways Measure Portfolio PerformanceDocument40 pages101 Ways Measure Portfolio Performancesaisurya10No ratings yet

- Fin Mgt Syllabus Spr 2010Document2 pagesFin Mgt Syllabus Spr 2010Economiks PanviewsNo ratings yet

- International Money MarketDocument18 pagesInternational Money Markeths927071No ratings yet

- emerson 806Document1 pageemerson 806mark fakundinyNo ratings yet

- Lai Inc Had The Following Investment Transactions 1 Purchased Chang CorporationDocument1 pageLai Inc Had The Following Investment Transactions 1 Purchased Chang CorporationMiroslav GegoskiNo ratings yet

- Latihan UAS Manacc TUTORKU (Answered)Document10 pagesLatihan UAS Manacc TUTORKU (Answered)Della BianchiNo ratings yet

- Fine003 PDFDocument27 pagesFine003 PDFNageshwar SinghNo ratings yet

- Master ProspectusDocument238 pagesMaster ProspectusafkarputraNo ratings yet

- Marketing Plan - Ruwan LakmalDocument10 pagesMarketing Plan - Ruwan Lakmalsam rosNo ratings yet

- Analyzing Financial Ratios to Evaluate a CompanyDocument38 pagesAnalyzing Financial Ratios to Evaluate a Companymuzaire solomon100% (1)

- Share Based CompensationDocument5 pagesShare Based CompensationStacy Smith0% (1)

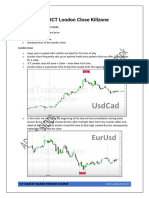

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- 1992 Indian Stock Market ScamDocument5 pages1992 Indian Stock Market ScamParitosh SinglaNo ratings yet

- FX European-Commodities Mean Reversion StrategyDocument14 pagesFX European-Commodities Mean Reversion Strategy848 Anirudh ChaudheriNo ratings yet

- ExoCharts by SassyDocument7 pagesExoCharts by SassycabbattNo ratings yet

- Ias 28 Investment in Associate IllustrationDocument6 pagesIas 28 Investment in Associate IllustrationVatchdemonNo ratings yet

- Assignment 14Document7 pagesAssignment 14Satishkumar NagarajNo ratings yet

- EBRD Local Currency FinancingDocument25 pagesEBRD Local Currency FinancingSandraNo ratings yet

- Ross12e Chapter30 TB AnswerkeyDocument57 pagesRoss12e Chapter30 TB AnswerkeyHà HoàngNo ratings yet

- Ca Final SFM (New Scheme) Dawn 2022 - ForexDocument98 pagesCa Final SFM (New Scheme) Dawn 2022 - Forexanand kachwaNo ratings yet

- FINN 117 Ch. 6 - Financial Ratios Formula GuideDocument3 pagesFINN 117 Ch. 6 - Financial Ratios Formula GuidePatrick MendozaNo ratings yet

- Introduction of Investment BankingDocument18 pagesIntroduction of Investment Bankingshubham100% (2)

- Unclaimed Dividend 201415 PDFDocument197 pagesUnclaimed Dividend 201415 PDFVamsibabu RatnakumarNo ratings yet

- Fin Sight - Apr 2013Document4 pagesFin Sight - Apr 2013rohitgupta234No ratings yet

- Presentation 1Document14 pagesPresentation 1Tanvi SidhayeNo ratings yet

- Review in General Mathematics (Quiz Bee)Document26 pagesReview in General Mathematics (Quiz Bee)cherrie annNo ratings yet

- Buy-Side Financial Modeling Slides 65cc55ad90b30Document474 pagesBuy-Side Financial Modeling Slides 65cc55ad90b30Nick JamesNo ratings yet