You might also like

- 2010 Handbook On Discovery Practice, Trial Lawyers Section of The Florida Bar & Conferences of The Circuit and County Courts JudgesDocument124 pages2010 Handbook On Discovery Practice, Trial Lawyers Section of The Florida Bar & Conferences of The Circuit and County Courts JudgesFloridaLegalBlog100% (3)

- 11 Blues Piano Voicings AnalysisDocument11 pages11 Blues Piano Voicings AnalysisBHNo ratings yet

- Taller de Ejercicios de PresupuestosDocument11 pagesTaller de Ejercicios de PresupuestosalexNo ratings yet

- Assignment1 Answer KahootDocument5 pagesAssignment1 Answer KahootLysss EpssssNo ratings yet

- Master PowerShell Tricks Volume 1Document88 pagesMaster PowerShell Tricks Volume 1ZoranZasovski100% (1)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Operations Management Assignment 1Document10 pagesOperations Management Assignment 1Muhammad SajidNo ratings yet

- Kripal, Debating The Mystical As The Ethical: An Indological Map, in Crossing Boundaries: Essays On The Ethical Status of Mysticism (2002) : 15-69Document28 pagesKripal, Debating The Mystical As The Ethical: An Indological Map, in Crossing Boundaries: Essays On The Ethical Status of Mysticism (2002) : 15-69Keren MiceNo ratings yet

- BudgetingDocument28 pagesBudgetingJade Gomez50% (2)

- Final 17ncDocument10 pagesFinal 17ncKevin James Sedurifa OledanNo ratings yet

- FinMan Planning Master-BudgetDocument3 pagesFinMan Planning Master-Budgetjim malajatNo ratings yet

- Pastor. The History of The Popes, From The Close of The Middle Ages. 1891. Vol. 31Document540 pagesPastor. The History of The Popes, From The Close of The Middle Ages. 1891. Vol. 31Patrologia Latina, Graeca et Orientalis100% (1)

- Straight ProblemDocument3 pagesStraight ProblemAldrin Liwanag89% (9)

- SPL Bar Exam Questions With Answers: BP 22 Memorandum Check (1994)Document38 pagesSPL Bar Exam Questions With Answers: BP 22 Memorandum Check (1994)Carla January Ong100% (1)

- Exercise 3 BudgetingDocument4 pagesExercise 3 BudgetingGabrielleNo ratings yet

- Financial PlanDocument16 pagesFinancial PlanSenpai Kun0% (1)

- Harry Potter and The Sorceror's StoneDocument17 pagesHarry Potter and The Sorceror's StoneParth Tiwari50% (4)

- RTCDocument27 pagesRTCMaple De los SantosNo ratings yet

- Pre-Installation Manual: Standard Frequency Series GeneratorsDocument20 pagesPre-Installation Manual: Standard Frequency Series GeneratorsLuis Fernando Garcia SNo ratings yet

- Operating Budget DiscussionDocument3 pagesOperating Budget DiscussionDavin DavinNo ratings yet

- Preparation of BudgetsDocument20 pagesPreparation of BudgetsAsri MustikaNo ratings yet

- Exercises 4 Financial Planning BudgetingDocument2 pagesExercises 4 Financial Planning BudgetingKyle PereiraNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Practice Set Short Term Budgeting PDFDocument12 pagesPractice Set Short Term Budgeting PDFRujean Salar AltejarNo ratings yet

- Budgeting Quiz QuestionnaireDocument7 pagesBudgeting Quiz QuestionnaireNinaNo ratings yet

- BudgetingDocument74 pagesBudgetingRevathi AnandNo ratings yet

- Proj 2Document15 pagesProj 2Shahan AsifNo ratings yet

- BudgetingDocument130 pagesBudgetingRevathi AnandNo ratings yet

- Problem On Cash Budget: 8 (The End of The Prior Quarter), The Company's Balance Were As FollowsDocument4 pagesProblem On Cash Budget: 8 (The End of The Prior Quarter), The Company's Balance Were As Followsshreya chapagainNo ratings yet

- Cash Sales Credit Sales: ACCT201B Practice Questions Chapter 8Document9 pagesCash Sales Credit Sales: ACCT201B Practice Questions Chapter 8GuinevereNo ratings yet

- Performance Management Pada Umkm Tahu: Analsis Decision Making, Master Budget DanDocument5 pagesPerformance Management Pada Umkm Tahu: Analsis Decision Making, Master Budget Danadzani maulidaNo ratings yet

- Review Problem: Budget Schedules: RequiredDocument8 pagesReview Problem: Budget Schedules: RequiredShafa AlyaNo ratings yet

- Budgeting Multiple ChoiceDocument2 pagesBudgeting Multiple ChoiceRachel Mae FajardoNo ratings yet

- ACFrOgBR3zmYIfST M04WW9MOxJsCDOY8ij K10c8jFzoDesUe4hmgtwitQThRfZx9zgdfBbbfAPg9fYbdGwDnuwcmqyJhSe8wLpgC1wkMIV6jGps45E YC2ro8e WakacYQ6ARdjCeTf76iCHtdDocument6 pagesACFrOgBR3zmYIfST M04WW9MOxJsCDOY8ij K10c8jFzoDesUe4hmgtwitQThRfZx9zgdfBbbfAPg9fYbdGwDnuwcmqyJhSe8wLpgC1wkMIV6jGps45E YC2ro8e WakacYQ6ARdjCeTf76iCHtdMario FiskaNo ratings yet

- Geme CostDocument6 pagesGeme CostBiruk Chuchu NigusuNo ratings yet

- Chap07 Rev. FI5 Ex PRDocument11 pagesChap07 Rev. FI5 Ex PRKhryzha Hanne Dela CruzNo ratings yet

- Completing A Master BudgetDocument2 pagesCompleting A Master BudgetPines MacapagalNo ratings yet

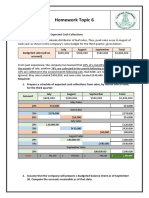

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Merchandise Business Class PerformanceDocument5 pagesMerchandise Business Class PerformanceGrace GamillaNo ratings yet

- Quiz 4 Budgeting (For Students)Document5 pagesQuiz 4 Budgeting (For Students)agaceram9090No ratings yet

- This Study Resource Was: Strategic Cost Management Master BudgetDocument5 pagesThis Study Resource Was: Strategic Cost Management Master BudgetNCTNo ratings yet

- Cost Accounting Assignment #2Document5 pagesCost Accounting Assignment #2BRIANNIE ASRI VIVASNo ratings yet

- AE 19 Exercise Problem Financial Planning and Forecasting 2Document2 pagesAE 19 Exercise Problem Financial Planning and Forecasting 2John Anjelo MoraldeNo ratings yet

- Merchandising Hand OutDocument7 pagesMerchandising Hand OutElla Mae SaludoNo ratings yet

- Chap07 Rev. FI5 Ex PR 1Document10 pagesChap07 Rev. FI5 Ex PR 1Beyond ThatNo ratings yet

- Week 1 - Ruth Theodora - AccountingDocument5 pagesWeek 1 - Ruth Theodora - AccountingRuth AritonangNo ratings yet

- Operational Budgeting ReviewerDocument5 pagesOperational Budgeting ReviewerMilcah Deloso Santos100% (1)

- Master Budget Assignment SollutionDocument7 pagesMaster Budget Assignment Sollutionatinafu assefaNo ratings yet

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Sept 21 ExercisesDocument12 pagesSept 21 ExercisesPeachyNo ratings yet

- Actg 26A - Strategic Cost Management Take Home Quiz: RequirementsDocument2 pagesActg 26A - Strategic Cost Management Take Home Quiz: RequirementsseviNo ratings yet

- Hillyard CompanyDocument3 pagesHillyard CompanyJea BalagtasNo ratings yet

- Budgeting Problems PDFDocument5 pagesBudgeting Problems PDFER Aditya DasNo ratings yet

- Assignment Cost Final Edition1Document5 pagesAssignment Cost Final Edition1Bekama Abdii Koo TesfayeNo ratings yet

- Comprehensive Problem Master BudgetDocument1 pageComprehensive Problem Master BudgethdejnNo ratings yet

- Assignment 2Document4 pagesAssignment 2Ella Davis0% (1)

- Final ExamDocument3 pagesFinal ExamLopez, Azzia M.No ratings yet

- SOAL LATIHAN OSN tHE AKUNTANSIDocument2 pagesSOAL LATIHAN OSN tHE AKUNTANSIBiEbbah MiszDhieysieysiey GitäLoversNo ratings yet

- Budgeting - 1Document3 pagesBudgeting - 1Muhammad MansoorNo ratings yet

- Pak NotoDocument9 pagesPak NotopanjiNo ratings yet

- Budgeting - 2Document4 pagesBudgeting - 2Muhammad MansoorNo ratings yet

- Budgeting and Budgetary ControlDocument13 pagesBudgeting and Budgetary ControlRenu PoddarNo ratings yet

- ILYJADocument5 pagesILYJALopez, Azzia M.No ratings yet

- M2 Q Cfs and FinplnDocument7 pagesM2 Q Cfs and FinplnLeane MarcoletaNo ratings yet

- BUDGETINGDocument3 pagesBUDGETINGkhyla Marie NooraNo ratings yet

- Pre Finals Manacc 1Document8 pagesPre Finals Manacc 1Gesselle Acebedo0% (1)

- Comp. ExamDocument11 pagesComp. ExamProf. Nisaif JasimNo ratings yet

- Master BudgetingDocument20 pagesMaster Budgetingjoinme2dayNo ratings yet

- CAS 11 Midterm QuizDocument7 pagesCAS 11 Midterm QuizShariine BestreNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- NovelDocument2 pagesNovelBlnd RahimNo ratings yet

- United States v. Troy Stephens, 7 F.3d 285, 2d Cir. (1993)Document8 pagesUnited States v. Troy Stephens, 7 F.3d 285, 2d Cir. (1993)Scribd Government DocsNo ratings yet

- Library Etymology - WiktionaryDocument4 pagesLibrary Etymology - WiktionarySamuel D. AdeyemiNo ratings yet

- Chapter 176Document13 pagesChapter 176Intan Sanditiya AlifNo ratings yet

- Nutrients 10 00096Document11 pagesNutrients 10 00096OcZzNo ratings yet

- LibreView Guide - Italian PaperDocument12 pagesLibreView Guide - Italian PaperJesus MuñozNo ratings yet

- COVID-19 Student Mental Health CheckDocument15 pagesCOVID-19 Student Mental Health CheckAwalil ArisandiNo ratings yet

- PIL Lecture Notes - Week 1Document3 pagesPIL Lecture Notes - Week 1Yoshita SoodNo ratings yet

- 1-Data UnderstandingDocument21 pages1-Data UnderstandingMahander OadNo ratings yet

- PssDocument174 pagesPssdavev2005No ratings yet

- Ds 42 Upgrade enDocument118 pagesDs 42 Upgrade enJaviera OrellanaNo ratings yet

- The Drum Magazine 23 OctoberDocument40 pagesThe Drum Magazine 23 OctoberFa BaNo ratings yet

- Technical Analysis of Sun PharmaDocument7 pagesTechnical Analysis of Sun PharmaAshutosh TulsyanNo ratings yet

- Corporation PDFDocument8 pagesCorporation PDFKAMALINo ratings yet

- BKM CH 01 AnswersDocument4 pagesBKM CH 01 AnswersDeepak OswalNo ratings yet

- Dicision MakingDocument34 pagesDicision MakingArpita PatelNo ratings yet

- Cornel Fratica ResumeDocument4 pagesCornel Fratica ResumeCatalina CarabasNo ratings yet

- TASK 1 JustificationDocument3 pagesTASK 1 JustificationsweetzazaNo ratings yet

- Basic Résumé Types: 1. Chronological ResumeDocument9 pagesBasic Résumé Types: 1. Chronological ResumeDegee O. GonzalesNo ratings yet

- Comparative Study of BanksDocument8 pagesComparative Study of BanksSaurabh RajNo ratings yet