You might also like

- This Study Resource Was: Strategic Cost Management Master BudgetDocument5 pagesThis Study Resource Was: Strategic Cost Management Master BudgetNCTNo ratings yet

- Exercise 3 BudgetingDocument4 pagesExercise 3 BudgetingGabrielleNo ratings yet

- CAS 11 Midterm QuizDocument7 pagesCAS 11 Midterm QuizShariine BestreNo ratings yet

- 04 Budgeting 15PROBLEMSDocument5 pages04 Budgeting 15PROBLEMSNicoleNo ratings yet

- Chapter 07 BillingsDocument1 pageChapter 07 Billingsdeusvanfadri0905No ratings yet

- Cash Sales Credit Sales: ACCT201B Practice Questions Chapter 8Document9 pagesCash Sales Credit Sales: ACCT201B Practice Questions Chapter 8GuinevereNo ratings yet

- Profit Planning and BudgetingDocument3 pagesProfit Planning and BudgetingRoyce Maenard EstanislaoNo ratings yet

- Quiz 4 Budgeting (For Students)Document5 pagesQuiz 4 Budgeting (For Students)agaceram9090No ratings yet

- Budgeting Quiz QuestionnaireDocument7 pagesBudgeting Quiz QuestionnaireNinaNo ratings yet

- Group Quizbowl FormattedDocument17 pagesGroup Quizbowl FormattedSarah BalisacanNo ratings yet

- BudgetingDocument28 pagesBudgetingJade Gomez50% (2)

- Financial Management Practice Problem - Financial PlanningDocument4 pagesFinancial Management Practice Problem - Financial PlanningJeremy James AlbayNo ratings yet

- Completing A Master BudgetDocument2 pagesCompleting A Master BudgetPines MacapagalNo ratings yet

- BUDGETINGDocument3 pagesBUDGETINGkhyla Marie NooraNo ratings yet

- ACTDocument2 pagesACTjonalyn arellanoNo ratings yet

- Budget Problems-Homework Help1Document1 pageBudget Problems-Homework Help1Ryoma EchizenNo ratings yet

- Example Cash BudgetDocument1 pageExample Cash BudgetPamela GalangNo ratings yet

- Final 17ncDocument10 pagesFinal 17ncKevin James Sedurifa OledanNo ratings yet

- Exercises 4 Financial Planning BudgetingDocument2 pagesExercises 4 Financial Planning BudgetingKyle PereiraNo ratings yet

- Comprehensive Problem Master BudgetDocument1 pageComprehensive Problem Master BudgethdejnNo ratings yet

- Riyadh Final PB Far 2019Document17 pagesRiyadh Final PB Far 2019jhaizonNo ratings yet

- Master Budget.9Document3 pagesMaster Budget.9Hiraya ManawariNo ratings yet

- Short-Term Budgeting ExercisesDocument2 pagesShort-Term Budgeting Exercisesahyenn cabelloNo ratings yet

- Pre Finals Manacc 1Document8 pagesPre Finals Manacc 1Gesselle Acebedo0% (1)

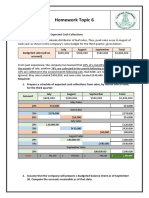

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Asia Pacific College of Advanced Studies Prelims Exam MGMT Acctg 2 Management Accounting 2Document7 pagesAsia Pacific College of Advanced Studies Prelims Exam MGMT Acctg 2 Management Accounting 2geminailnaNo ratings yet

- Budgeting Multiple ChoiceDocument2 pagesBudgeting Multiple ChoiceRachel Mae FajardoNo ratings yet

- Strat Cost Man Prelim QuizDocument1 pageStrat Cost Man Prelim QuizKena Montes Dela PeñaNo ratings yet

- ILYJADocument5 pagesILYJALopez, Azzia M.No ratings yet

- Ala in Finacct 3Document4 pagesAla in Finacct 3VIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Exercises D. Some Other Number - 4,350Document1 pageExercises D. Some Other Number - 4,350Meng DanNo ratings yet

- Quiz Number 3Document3 pagesQuiz Number 3Lopez, Azzia M.No ratings yet

- FAR Preboard SolutionsDocument4 pagesFAR Preboard SolutionsHikariNo ratings yet

- Assignment1 Answer KahootDocument5 pagesAssignment1 Answer KahootLysss EpssssNo ratings yet

- San Pedro College: Accounting & Financial ManagementDocument4 pagesSan Pedro College: Accounting & Financial ManagementJuan FrivaldoNo ratings yet

- Auditing 2019 P S CH 8Document16 pagesAuditing 2019 P S CH 8barakat801No ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Performance Task No 2 - Group Work - Planning Concepts and Tools P1Document8 pagesPerformance Task No 2 - Group Work - Planning Concepts and Tools P1Corn SaladNo ratings yet

- ACCTG-206B-FIRST-PREBOARD Without AnswerDocument16 pagesACCTG-206B-FIRST-PREBOARD Without AnswerRheu ReyesNo ratings yet

- AE 19 Exercise Problem Financial Planning and Forecasting 2Document2 pagesAE 19 Exercise Problem Financial Planning and Forecasting 2John Anjelo MoraldeNo ratings yet

- Master Budget With SolutionsDocument12 pagesMaster Budget With SolutionsDea Andal100% (4)

- Second PreboardDocument6 pagesSecond PreboardBella AyabNo ratings yet

- Drills - Comprehensive BudgetingDocument11 pagesDrills - Comprehensive BudgetingDan RyanNo ratings yet

- Assignment 2Document4 pagesAssignment 2Ella Davis0% (1)

- Acctg 13 - Midterm ExamDocument8 pagesAcctg 13 - Midterm ExamMary Grace Castillo AlmonedaNo ratings yet

- Chapter 9 Review QuestionsDocument8 pagesChapter 9 Review QuestionsKanika DahiyaNo ratings yet

- ACC-122 Inventory QuizDocument2 pagesACC-122 Inventory QuizPea Del Monte Añana100% (1)

- Problem 20Document4 pagesProblem 20Kath Chu100% (1)

- College of Business & Accountancy Manila City 1 Sem SY 2021-22Document2 pagesCollege of Business & Accountancy Manila City 1 Sem SY 2021-22Shiela Mae Pon AnNo ratings yet

- Cash Budget . Feb 2020: Q 1 Calgon ProductsDocument11 pagesCash Budget . Feb 2020: Q 1 Calgon Products신두No ratings yet

- Activity # 1: Management Advisory Services Part 1Document2 pagesActivity # 1: Management Advisory Services Part 1Vince BesarioNo ratings yet

- Diagnostic in Basic AccountingDocument5 pagesDiagnostic in Basic Accountingjapvivi cece100% (2)

- Activity BudgetingDocument5 pagesActivity BudgetingHotcheeseramyeonNo ratings yet

- 1617 2ndS 3rde JonaldBDocument11 pages1617 2ndS 3rde JonaldBAlyssa Andrea SabinoNo ratings yet

- A. P 600,000 and P5,500,000: Financial Statement AnalysisDocument20 pagesA. P 600,000 and P5,500,000: Financial Statement AnalysisDivine Cuasay100% (1)

- Session 7 Practice Questions - Profit Planning: Multiple ChoiceDocument4 pagesSession 7 Practice Questions - Profit Planning: Multiple ChoiceLee Freckles Haengbok0% (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Quiz Number 3Document3 pagesQuiz Number 3Lopez, Azzia M.No ratings yet

- Finish Finish Start Start Start: Lorna Llamas Allia Lopez Divina Mineses Mary Ghel Muyalde Loreanne NabuaDocument3 pagesFinish Finish Start Start Start: Lorna Llamas Allia Lopez Divina Mineses Mary Ghel Muyalde Loreanne NabuaLopez, Azzia M.No ratings yet

- Questions 31 Thru 38 Are Based On The Following InformationDocument2 pagesQuestions 31 Thru 38 Are Based On The Following InformationLopez, Azzia M.No ratings yet

- EXAMMINEEEEENNNNDocument5 pagesEXAMMINEEEEENNNNLopez, Azzia M.No ratings yet

- Level of Awareness On The Impact of Train LawDocument2 pagesLevel of Awareness On The Impact of Train LawLopez, Azzia M.No ratings yet

- ILYJADocument5 pagesILYJALopez, Azzia M.No ratings yet

- IOPDocument4 pagesIOPLopez, Azzia M.No ratings yet

- Expected and Required Returns Answer: C Diff: MDocument6 pagesExpected and Required Returns Answer: C Diff: MLopez, Azzia M.No ratings yet

- ENGMMDocument2 pagesENGMMLopez, Azzia M.No ratings yet

- Finman Asnwer KeyDocument6 pagesFinman Asnwer KeyLopez, Azzia M.No ratings yet

- Acc 6666Document7 pagesAcc 6666Lopez, Azzia M.No ratings yet

- Required Return Answer: B Diff: E N IDocument8 pagesRequired Return Answer: B Diff: E N ILopez, Azzia M.No ratings yet

- Market Risk Answer: B Diff: MDocument5 pagesMarket Risk Answer: B Diff: MLopez, Azzia M.No ratings yet

- Examination 7Document6 pagesExamination 7Lopez, Azzia M.No ratings yet

- Examination 8Document5 pagesExamination 8Lopez, Azzia M.No ratings yet

- ERTDocument4 pagesERTLopez, Azzia M.No ratings yet

- VCCDocument8 pagesVCCLopez, Azzia M.No ratings yet

- ACC1AIS - Homework Exercises - Workshop 9: Excel Exercise 1Document8 pagesACC1AIS - Homework Exercises - Workshop 9: Excel Exercise 1SuptoNo ratings yet

- Sample Paper Accountancy: Class: - Xii SET-2, (2022-23)Document13 pagesSample Paper Accountancy: Class: - Xii SET-2, (2022-23)Kunwar PalNo ratings yet

- Fabozzi Gupta MarDocument16 pagesFabozzi Gupta MarNurwahidah AbidinNo ratings yet

- LC Accounting Q5 Part B Analysis - Lenders PerspectiveDocument7 pagesLC Accounting Q5 Part B Analysis - Lenders PerspectiveChloe KeaneNo ratings yet

- Explain - Module 2Document13 pagesExplain - Module 2Carlos Luis MalapitanNo ratings yet

- In The Books of Sangeeta, Anita and Smita Realisation A/c DR CRDocument2 pagesIn The Books of Sangeeta, Anita and Smita Realisation A/c DR CRHarendra PrajapatiNo ratings yet

- Model Sample Paper-2Document8 pagesModel Sample Paper-2arihant jainNo ratings yet

- Budgets in Tallyprime: Create A BudgetDocument8 pagesBudgets in Tallyprime: Create A BudgetpapuNo ratings yet

- Key Financial IndicatorsDocument21 pagesKey Financial IndicatorsLayNo ratings yet

- ACC100.101 Preliminary Examination - For PostingDocument5 pagesACC100.101 Preliminary Examination - For PostingRAMOS, Aliyah Faith P.No ratings yet

- 2cp Ce 23Document12 pages2cp Ce 23rodrigoNo ratings yet

- Csec Poa June 2007 p1Document10 pagesCsec Poa June 2007 p1Tavia LordNo ratings yet

- 2122 s3 Bafs Notes STDocument3 pages2122 s3 Bafs Notes STKiu YipNo ratings yet

- Government Accounting Overview: Korbel Foundation College, IncDocument16 pagesGovernment Accounting Overview: Korbel Foundation College, IncRuby Amor DoligosaNo ratings yet

- Effects of The Contract When The Thing Sold Has Been Lost 1. Loss (1493-1494)Document3 pagesEffects of The Contract When The Thing Sold Has Been Lost 1. Loss (1493-1494)ChaNo ratings yet

- Ts Grewal Solutions For Class 11 Accountancy Chapter 10 TrialDocument22 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 10 TrialMantejNo ratings yet

- Cash and Accrual BasisDocument4 pagesCash and Accrual BasisSeulgi KangNo ratings yet

- Constantino vs. CuisiaDocument37 pagesConstantino vs. CuisiaElephantNo ratings yet

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- AICO - Unbundling November 2013Document3 pagesAICO - Unbundling November 2013addyNo ratings yet

- Bar Essays Contracts Short Review Outline PDFDocument7 pagesBar Essays Contracts Short Review Outline PDFno contractNo ratings yet

- Fixed 215Document52 pagesFixed 215jusper wendoNo ratings yet

- Chapter 5 PDFDocument3 pagesChapter 5 PDFthatfuturecpaNo ratings yet

- Winding Up Petition: Hotels Limited Vs Tropicana Hotels Lilmited (2018) Eklr That TheDocument3 pagesWinding Up Petition: Hotels Limited Vs Tropicana Hotels Lilmited (2018) Eklr That TheBeverlyne MokayaNo ratings yet

- Financial Accounting (Bbaw2103)Document10 pagesFinancial Accounting (Bbaw2103)tachaini2727No ratings yet

- The New Central Bank Act: 1. Responsibility and Primary Objective of The BSPDocument28 pagesThe New Central Bank Act: 1. Responsibility and Primary Objective of The BSPflordeluna ayingNo ratings yet

- Tax Hacks The Tax Survival Tournament With Answers 1 PDFDocument23 pagesTax Hacks The Tax Survival Tournament With Answers 1 PDFjane dillanNo ratings yet

- Level Whitepaper On Financial WellbeingDocument15 pagesLevel Whitepaper On Financial WellbeingHajji AnwerNo ratings yet

- Espiritu V LandritoDocument2 pagesEspiritu V LandritorengieNo ratings yet

- VJ2Document4 pagesVJ2Thư TrầnNo ratings yet