You might also like

- Maximize Total Area Using Lagrange MultipliersDocument4 pagesMaximize Total Area Using Lagrange MultipliersninoNo ratings yet

- LagrangeDocument7 pagesLagrangeujwala_512No ratings yet

- COMP 567 Exe3: Min 2 S.T. 4 6 9 4, 0, Integer + +Document2 pagesCOMP 567 Exe3: Min 2 S.T. 4 6 9 4, 0, Integer + +zizo sosoNo ratings yet

- Algorithms Chapter 10 Exercises and SolutionsDocument43 pagesAlgorithms Chapter 10 Exercises and Solutionsc_noneNo ratings yet

- Quantum MechanicsDocument11 pagesQuantum MechanicsEverly NNo ratings yet

- Hmwk1 Solutions WatermarkDocument6 pagesHmwk1 Solutions Watermarkv8p4prncfxNo ratings yet

- Industrial Engineering (IE)Document22 pagesIndustrial Engineering (IE)محمد ناصر عليويNo ratings yet

- Karush-Kuhn-Tucker (KKT) Conditions: Lecture 11: Convex OptimizationDocument4 pagesKarush-Kuhn-Tucker (KKT) Conditions: Lecture 11: Convex OptimizationaaayoubNo ratings yet

- Analythical MethodsDocument45 pagesAnalythical MethodsVlad SuciuNo ratings yet

- ECN 2115 Lecture 1 - 2Document6 pagesECN 2115 Lecture 1 - 2GABRIEL CHIKUSELANo ratings yet

- Linear Programming Problem Graphical SolutionDocument22 pagesLinear Programming Problem Graphical SolutionARNo ratings yet

- Linear Programming (LP) FundamentalsDocument57 pagesLinear Programming (LP) FundamentalsPratibha GoswamiNo ratings yet

- 11.8 Constraint Optimization: Lagrange's MultipliersDocument4 pages11.8 Constraint Optimization: Lagrange's MultipliersAlexander MonroeNo ratings yet

- Econ 3030: Math Review of Monotonic TransformationsDocument4 pagesEcon 3030: Math Review of Monotonic TransformationsSafal AryalNo ratings yet

- Cours Optim Ch3Document16 pagesCours Optim Ch3mondherNo ratings yet

- INDE 513 hw1 SolDocument7 pagesINDE 513 hw1 SolWei GuoNo ratings yet

- HW04Document5 pagesHW04Zunaash Rasheed0% (1)

- Lagrangian Duality Geometric Visualization Convex Optimization ProblemsDocument8 pagesLagrangian Duality Geometric Visualization Convex Optimization ProblemsGandhimathinathanNo ratings yet

- Linear Programming: Graphical Method (Two Variables)Document11 pagesLinear Programming: Graphical Method (Two Variables)Choi TeumeNo ratings yet

- Duality 2 PDFDocument10 pagesDuality 2 PDFNoel Saycon Jr.No ratings yet

- Duality Theory in Mathematical ProgrammingDocument10 pagesDuality Theory in Mathematical ProgrammingNoel Saycon Jr.No ratings yet

- Non-Serial Dynamic Programming. Academic Press, 1972. Another Reference Used inDocument37 pagesNon-Serial Dynamic Programming. Academic Press, 1972. Another Reference Used inAmrendra KumarNo ratings yet

- Vanessa-Linear ProgrammingDocument13 pagesVanessa-Linear ProgrammingVanessa PallarNo ratings yet

- Notes LagrangeDocument8 pagesNotes LagrangeLennard PangNo ratings yet

- Constrained Optimization Problem SolvedDocument6 pagesConstrained Optimization Problem SolvedMikeHuynhNo ratings yet

- 5-The Dual and Mix ProblemsDocument23 pages5-The Dual and Mix Problemsthe_cool48No ratings yet

- 3 The Utility Maximization ProblemDocument10 pages3 The Utility Maximization ProblemDaniel Lee Eisenberg JacobsNo ratings yet

- The Kernel Trick: Transforming Data to Make it Linearly SeparableDocument4 pagesThe Kernel Trick: Transforming Data to Make it Linearly SeparableShankaranarayanan GopalNo ratings yet

- A Few More Past Exam Questions (Multiple Choice)Document6 pagesA Few More Past Exam Questions (Multiple Choice)exams_sbsNo ratings yet

- Modified Section 01Document7 pagesModified Section 01Eric ShiNo ratings yet

- Midterm ReviewDocument72 pagesMidterm ReviewOgonna NwabuikwuNo ratings yet

- HW 4Document6 pagesHW 4Alexander MackeyNo ratings yet

- Section 3 7 PDFDocument12 pagesSection 3 7 PDFUmer YounasNo ratings yet

- Solu 10Document43 pagesSolu 10Eric FansiNo ratings yet

- Representation and Types of Functions: 1 in This SectionDocument8 pagesRepresentation and Types of Functions: 1 in This SectionMichael PearsonNo ratings yet

- Constrained OptimizationDocument9 pagesConstrained OptimizationananyaajatasatruNo ratings yet

- Business Maths Chapter 4Document23 pagesBusiness Maths Chapter 4鄭仲抗No ratings yet

- Mathematics of Decision MakingDocument40 pagesMathematics of Decision MakingSilvia SacconeNo ratings yet

- Mat495 Chapter 9Document13 pagesMat495 Chapter 9MuhamadSadiqNo ratings yet

- Management Science Lesson Seven and EightDocument6 pagesManagement Science Lesson Seven and EightAyoniseh CarolNo ratings yet

- Part A: Texas A&M University MEEN 683 Multidisciplinary System Design Optimization (MSADO) Spring 2021 Assignment 2Document5 pagesPart A: Texas A&M University MEEN 683 Multidisciplinary System Design Optimization (MSADO) Spring 2021 Assignment 2BobaNo ratings yet

- Constrained OptimizationDocument19 pagesConstrained OptimizationVikram SharmaNo ratings yet

- Midterm Questions and Answers Part I: Short AnswerDocument5 pagesMidterm Questions and Answers Part I: Short AnswerDerbern99No ratings yet

- Const OptDocument22 pagesConst OptSaujanya SahuNo ratings yet

- University of Maryland: Econ 600Document22 pagesUniversity of Maryland: Econ 600TABIBI11No ratings yet

- Math 5610 Fall 2018 Notes of 09/25-26/18 Linear ProgrammingDocument14 pagesMath 5610 Fall 2018 Notes of 09/25-26/18 Linear Programmingbb sparrowNo ratings yet

- Ee/Econ 458 Introduction To Linear Programming: J. MccalleyDocument25 pagesEe/Econ 458 Introduction To Linear Programming: J. Mccalleykaren dejoNo ratings yet

- Problem Set 1 - Econ 217 PDFDocument3 pagesProblem Set 1 - Econ 217 PDFmiraNo ratings yet

- Httpsmoodle - Usth.edu - Vnpluginfile.php51389mod resourcecontent1Calculus20I20-20Tutorial20231 PDFDocument6 pagesHttpsmoodle - Usth.edu - Vnpluginfile.php51389mod resourcecontent1Calculus20I20-20Tutorial20231 PDFThanh VuquangNo ratings yet

- ASTU Lecture 05: Numerical Methods in MATLABDocument80 pagesASTU Lecture 05: Numerical Methods in MATLABBirhex FeyeNo ratings yet

- 4.8 Lagrange Multipliers - Calculus Volume 3 - OpenStaxDocument15 pages4.8 Lagrange Multipliers - Calculus Volume 3 - OpenStaxdebbieleeohyeahNo ratings yet

- Lagrange Multipliers: Solving Multivariable Optimization ProblemsDocument5 pagesLagrange Multipliers: Solving Multivariable Optimization ProblemsOctav DragoiNo ratings yet

- Problem 2.5: Calculation of Cost Per Unit of Each ProductDocument18 pagesProblem 2.5: Calculation of Cost Per Unit of Each ProductTrixie HicaldeNo ratings yet

- MATH21Document11 pagesMATH21NilushaNo ratings yet

- Calculating Limits in Calculus IDocument7 pagesCalculating Limits in Calculus IBunga RosanggreniNo ratings yet

- CalcII Probability SolutionsDocument5 pagesCalcII Probability SolutionsD Princess ShailashreeNo ratings yet

- FHMM1314 MBI Topic 3 Student Version 202301Document58 pagesFHMM1314 MBI Topic 3 Student Version 202301Rhinndhi SakthyvelNo ratings yet

- DonatoDocument11 pagesDonatoHuỳnh NguyênNo ratings yet

- Ee/Econ 458 The Simplex Method: J. MccalleyDocument36 pagesEe/Econ 458 The Simplex Method: J. Mccalleykaren dejoNo ratings yet

- Ee/Econ 458 Lpopf: J. MccalleyDocument45 pagesEe/Econ 458 Lpopf: J. Mccalleykaren dejoNo ratings yet

- Elec LpopfDocument22 pagesElec Lpopfchet_duttsNo ratings yet

- Ee/Econ 458 Integer Programming: J. MccalleyDocument33 pagesEe/Econ 458 Integer Programming: J. Mccalleykaren dejoNo ratings yet

- Real-Time Electricity MarketsDocument35 pagesReal-Time Electricity Marketskaren dejoNo ratings yet

- LP Simplex 3Document12 pagesLP Simplex 3karen dejoNo ratings yet

- Solving Linear Programs 1.0 Basic Form: C) X (H X FDocument17 pagesSolving Linear Programs 1.0 Basic Form: C) X (H X Fkaren dejoNo ratings yet

- LPOPF SettlementsDocument33 pagesLPOPF Settlementskaren dejoNo ratings yet

- LP Simplex 3Document9 pagesLP Simplex 3karen dejoNo ratings yet

- Real Time PDFDocument7 pagesReal Time PDFKandlakuntaBhargavaNo ratings yet

- LP Simplex 2Document25 pagesLP Simplex 2karen dejoNo ratings yet

- Market SummaryDocument40 pagesMarket Summarykaren dejoNo ratings yet

- Market SummaryDocument40 pagesMarket Summarykaren dejoNo ratings yet

- Miso1 2009Document8 pagesMiso1 2009karen dejoNo ratings yet

- Op Tim Ization BasicsDocument32 pagesOp Tim Ization Basicskaren dejoNo ratings yet

- Miso3 2009Document6 pagesMiso3 2009karen dejoNo ratings yet

- Op Tim Ization IntroDocument49 pagesOp Tim Ization Introkaren dejoNo ratings yet

- HW7Document2 pagesHW7karen dejoNo ratings yet

- Ee/Econ 458 PF Equations: J. MccalleyDocument34 pagesEe/Econ 458 PF Equations: J. Mccalleykaren dejoNo ratings yet

- The Power Flow Equations 1.0 The Admittance Matrix: Current Injections at A Bus Are Analogous To Power Injections. TheDocument29 pagesThe Power Flow Equations 1.0 The Admittance Matrix: Current Injections at A Bus Are Analogous To Power Injections. TheJose A. Regalado RojasNo ratings yet

- PJM ArevaDocument8 pagesPJM Arevakaren dejoNo ratings yet

- Payment Vs Bid CostDocument12 pagesPayment Vs Bid Costkaren dejoNo ratings yet

- HW 6 SolutionsDocument11 pagesHW 6 Solutionskaren dejoNo ratings yet

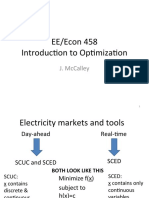

- Ee/Econ 458 Market Overview: Time-Line and Scuc, Rac, Sced: J. MccalleyDocument10 pagesEe/Econ 458 Market Overview: Time-Line and Scuc, Rac, Sced: J. Mccalleykaren dejoNo ratings yet

- Introduction To CPLEX 1.0 OverviewDocument13 pagesIntroduction To CPLEX 1.0 Overviewkaren dejoNo ratings yet

- Unit Commitment,: Jdm@linux3.ece - Iastate.eduDocument33 pagesUnit Commitment,: Jdm@linux3.ece - Iastate.edukaren dejoNo ratings yet

- Ee/Econ 458 Scuc: J. MccalleyDocument42 pagesEe/Econ 458 Scuc: J. Mccalleykaren dejoNo ratings yet

- HW 7 SolutionsDocument9 pagesHW 7 Solutionskaren dejoNo ratings yet

- Ee/Econ 458 Introduction To Linear Programming: J. MccalleyDocument25 pagesEe/Econ 458 Introduction To Linear Programming: J. Mccalleykaren dejoNo ratings yet

- Chapter 6. Mining Frequent Patterns, Associations and Correlations - Basic Concepts and MethodsDocument68 pagesChapter 6. Mining Frequent Patterns, Associations and Correlations - Basic Concepts and MethodsNhat ThanhNo ratings yet

- Queue Laboratory Exercise PDFDocument6 pagesQueue Laboratory Exercise PDFEdmark AldeaNo ratings yet

- LeetCode Common Templates & ProblemsDocument8 pagesLeetCode Common Templates & ProblemsGaurav SinghNo ratings yet

- Artificial Intelligence Analyst (27nov20)Document2 pagesArtificial Intelligence Analyst (27nov20)adil dahbiNo ratings yet

- Topic 8 - Maxima MinimaDocument27 pagesTopic 8 - Maxima MinimaAynul Bashar AmitNo ratings yet

- Caesar Cipher (Shift) - Online Decoder, Encoder, Solver, TranslatorDocument1 pageCaesar Cipher (Shift) - Online Decoder, Encoder, Solver, TranslatorCarter SneedNo ratings yet

- Numerical Analysis of Mechanical SystemsDocument20 pagesNumerical Analysis of Mechanical SystemsCKNo ratings yet

- CH 2. ForecastingBDocument59 pagesCH 2. ForecastingBMuhammad Rizky ParamartaNo ratings yet

- Solution Assignment 11Document7 pagesSolution Assignment 11sushant sharmaNo ratings yet

- AVL Trees: Initially Prepared by Dr. İlyas Çiçekli Improved by Various Bilkent CS202 InstructorsDocument28 pagesAVL Trees: Initially Prepared by Dr. İlyas Çiçekli Improved by Various Bilkent CS202 InstructorsAzizNo ratings yet

- Backgroundofcommunication Systems20201Document2 pagesBackgroundofcommunication Systems20201Vũ Hoàng LongNo ratings yet

- hm5 2015Document2 pageshm5 2015Mickey WongNo ratings yet

- Gandhinagar Institute of Technology: Mechanical Engineering DepartmentDocument19 pagesGandhinagar Institute of Technology: Mechanical Engineering DepartmentAnonymous JJTulAtUXn100% (1)

- Sample 7394Document11 pagesSample 7394insan100% (1)

- Artificial Intelligence in Gravel PackingDocument22 pagesArtificial Intelligence in Gravel PackingUgomuoh Tochukwu TheophineNo ratings yet

- Identification of Synchronous Generator Transfer FunctionsDocument9 pagesIdentification of Synchronous Generator Transfer FunctionsjandazNo ratings yet

- A Full - and Half-Cycle DFT-based Technique For Fault AnalysisDocument6 pagesA Full - and Half-Cycle DFT-based Technique For Fault AnalysisYaraRajashekarMudirajNo ratings yet

- NUS laboratory report analysis of process modelsDocument10 pagesNUS laboratory report analysis of process modelsKai Hee GohNo ratings yet

- 8-5 Study Guide and Intervention: Using The Distributive PropertyDocument2 pages8-5 Study Guide and Intervention: Using The Distributive Propertybd6cpynwmpNo ratings yet

- VTU e-learning Courseware: System Compensation Classifies Controllers (PID, PI, PD, PDocument9 pagesVTU e-learning Courseware: System Compensation Classifies Controllers (PID, PI, PD, Pvidya_sagar826No ratings yet

- Coupled TanksDocument32 pagesCoupled TanksAnkur MondalNo ratings yet

- Uncertainty Budget TemplateDocument4 pagesUncertainty Budget TemplateshahazadNo ratings yet

- STAT 608 II: Monte Carlo Methods in Statistics. Winter 2015Document2 pagesSTAT 608 II: Monte Carlo Methods in Statistics. Winter 2015Jesús DanielNo ratings yet

- Feature Based Techniques For A Face Recognition Using Supervised Learning Algorithms Based On Fixed Monocular Video CameraDocument29 pagesFeature Based Techniques For A Face Recognition Using Supervised Learning Algorithms Based On Fixed Monocular Video CameraINNOVATIVE COMPUTING REVIEWNo ratings yet

- Q-Deformed Lie Algebras and Fractional CalculusDocument8 pagesQ-Deformed Lie Algebras and Fractional CalculusFahd ElshemaryNo ratings yet

- Assignment 9 SolutionsDocument5 pagesAssignment 9 Solutions张浩然No ratings yet

- Goldstein 21 7 12 PDFDocument8 pagesGoldstein 21 7 12 PDFbgiangre8372100% (2)

- Lab Assignment 1 Title: Data Wrangling I: Problem StatementDocument12 pagesLab Assignment 1 Title: Data Wrangling I: Problem StatementMr. LegendpersonNo ratings yet

- Jim Dai TextbookDocument168 pagesJim Dai TextbookParthNo ratings yet