You might also like

- Accounting Cheat SheetDocument7 pagesAccounting Cheat Sheetopty100% (16)

- Case Assignment 8 - Diamond Energy Resources PDFDocument3 pagesCase Assignment 8 - Diamond Energy Resources PDFAudrey Ang100% (1)

- Cafes Monte Bianco MemoDocument4 pagesCafes Monte Bianco Memocatspajamas 1167% (6)

- Module 004 Accounting For Cash: Definition, Nature and Composition of Cash and Cash Equivalents CashDocument12 pagesModule 004 Accounting For Cash: Definition, Nature and Composition of Cash and Cash Equivalents CashLee-chard EboeboNo ratings yet

- 05 Cash Cash EquivalentsDocument54 pages05 Cash Cash EquivalentsFordan Antolino85% (13)

- Cash PDFDocument10 pagesCash PDFGabriel JonNo ratings yet

- Charles Case StudyDocument4 pagesCharles Case StudyTracy KiarieNo ratings yet

- Microport ProspectusDocument445 pagesMicroport ProspectusAtom Peace0% (1)

- Carlsberg Case StudyDocument8 pagesCarlsberg Case StudyYusra KhanNo ratings yet

- Lesson 1 Cash and Cash EquivalentsDocument10 pagesLesson 1 Cash and Cash EquivalentsRica Lei N. DomingoNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document15 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Chapter 4 PAS 7 Statement of Cash FlowsDocument20 pagesChapter 4 PAS 7 Statement of Cash FlowsSimon RavanaNo ratings yet

- Module 1.1Document13 pagesModule 1.1Althea mary kate MorenoNo ratings yet

- Week 02 - 01 - Module 04 - Accounting For CashDocument12 pagesWeek 02 - 01 - Module 04 - Accounting For Cash지마리No ratings yet

- Cash and Cash Equivalents - SCDocument33 pagesCash and Cash Equivalents - SCKaren Estrañero LuzonNo ratings yet

- FMA Project (Cash Flow Statement)Document16 pagesFMA Project (Cash Flow Statement)PowerPoint GoNo ratings yet

- Cash Flow of ChakraDocument18 pagesCash Flow of ChakrabhargaviNo ratings yet

- Financial Accounting and Reporting - Cash and Cash EquivalentsDocument6 pagesFinancial Accounting and Reporting - Cash and Cash EquivalentsLuisitoNo ratings yet

- Summary - Cash and Cash EquivalentDocument9 pagesSummary - Cash and Cash EquivalentDyenNo ratings yet

- Summary - Cash and Cash EquivalentDocument9 pagesSummary - Cash and Cash EquivalentDyenNo ratings yet

- Chapter 3Document20 pagesChapter 3Hussien AdemNo ratings yet

- Module 1 - Cash and Cash EquivalentsDocument9 pagesModule 1 - Cash and Cash Equivalentsjay classroomNo ratings yet

- Assessment Task 1 (IA)Document4 pagesAssessment Task 1 (IA)Jonalyn BañegaNo ratings yet

- 6 Cash Flow StatementDocument255 pages6 Cash Flow StatementJaskaran KharoudNo ratings yet

- Nature of Cash AccountDocument10 pagesNature of Cash AccountLorena PernatoNo ratings yet

- QUESTIONSDocument3 pagesQUESTIONSEl AgricheNo ratings yet

- Accounting 3 - Cash and Cash EquivalentsDocument6 pagesAccounting 3 - Cash and Cash EquivalentsNoah HNo ratings yet

- Statement of Cash Flows: International Accounting Standard 7Document9 pagesStatement of Cash Flows: International Accounting Standard 7Phương Vy Hà MaiNo ratings yet

- Cashand Cash Equivalents101Document38 pagesCashand Cash Equivalents101Wynphap podiotanNo ratings yet

- FIN AC 1 - Module 3Document4 pagesFIN AC 1 - Module 3Ashley ManaliliNo ratings yet

- Cash Flow AnalysisDocument7 pagesCash Flow AnalysisDeepalaxmi BhatNo ratings yet

- 231301AP23 - IAS 7 Identification of Cash EquivalentsDocument13 pages231301AP23 - IAS 7 Identification of Cash EquivalentsKwadwo AsaseNo ratings yet

- Definition of 'Short-Term Investments': Cash and Cash Equivalents Are The Most LiquidDocument3 pagesDefinition of 'Short-Term Investments': Cash and Cash Equivalents Are The Most LiquidHazel San JuanNo ratings yet

- Chapter 7Document11 pagesChapter 7Louie Ann CasabarNo ratings yet

- Chapter 2 Cash and Cash EquivalentsDocument12 pagesChapter 2 Cash and Cash EquivalentslorieferpaloganNo ratings yet

- Estelar: Deposit Mobilization &lending Policies of State Bank of IndiaDocument42 pagesEstelar: Deposit Mobilization &lending Policies of State Bank of IndiaBalwinder SinghNo ratings yet

- 20.0 NAS 7 - SetPasswordDocument8 pages20.0 NAS 7 - SetPasswordDhruba AdhikariNo ratings yet

- IND AS 7 Cash Flow Statement by Rahul MalkanDocument13 pagesIND AS 7 Cash Flow Statement by Rahul Malkanvishwas jagrawalNo ratings yet

- IA1-ASSDocument3 pagesIA1-ASSElexie RollonNo ratings yet

- Cash and Cash EquivalentsDocument15 pagesCash and Cash EquivalentsVon Rother Celoso DiazNo ratings yet

- Chapter 3 Cash Flow StatementDocument38 pagesChapter 3 Cash Flow Statementswarna dasNo ratings yet

- Welcome To Our Presentation: Topic: Management of Cash & Marketable SecuritiesDocument23 pagesWelcome To Our Presentation: Topic: Management of Cash & Marketable SecuritiesAkash BhowmikNo ratings yet

- Module 1Document12 pagesModule 1bhettyna noayNo ratings yet

- UntitledDocument6 pagesUntitledThelma DancelNo ratings yet

- Intermediate Accounting Cash and Cash Equivalents Reviewer For 1st YearDocument10 pagesIntermediate Accounting Cash and Cash Equivalents Reviewer For 1st YearGUNDA, NICOLE ANNE T.No ratings yet

- Bus Fin Topic 3Document18 pagesBus Fin Topic 3Nadjmeah AbdillahNo ratings yet

- Required?: Complexities of International Cash Management or Why Working Capital Management IsDocument3 pagesRequired?: Complexities of International Cash Management or Why Working Capital Management IsAnmol GrewalNo ratings yet

- What Is A Cash Flow Forecast?: Financial DistressDocument5 pagesWhat Is A Cash Flow Forecast?: Financial DistressSai TejaNo ratings yet

- 4 Pas 7 - Statement of Cash Flows: Objective and ScopeDocument17 pages4 Pas 7 - Statement of Cash Flows: Objective and ScopeRose Aubrey A Cordova100% (1)

- Ramiro, Lorren - Money MarketsDocument4 pagesRamiro, Lorren - Money Marketslorren ramiroNo ratings yet

- Ifa C1Document59 pagesIfa C1melkamuaemiro1No ratings yet

- Cash ManagementDocument16 pagesCash ManagementAppy9No ratings yet

- Assignment of Management of Working Capital On Cash ManagementDocument7 pagesAssignment of Management of Working Capital On Cash ManagementShubhamNo ratings yet

- Working Capital CashDocument6 pagesWorking Capital CashNiña Rhocel YangcoNo ratings yet

- Webinar 7: Standards To Bank On: PFRS and PAS For BanksDocument2 pagesWebinar 7: Standards To Bank On: PFRS and PAS For BanksRoland Vincent JulianNo ratings yet

- Cash Flow Statements - Pas 7Document1 pageCash Flow Statements - Pas 7JyNo ratings yet

- Management of CashDocument6 pagesManagement of CashVIVEKNo ratings yet

- Speeding Up CollectionsDocument3 pagesSpeeding Up CollectionsAshree AgarwalNo ratings yet

- Cash and Receivables: Chapter ReviewDocument6 pagesCash and Receivables: Chapter ReviewOmar HosnyNo ratings yet

- AUDT03 1 Cash Cash Equivalents PDFDocument2 pagesAUDT03 1 Cash Cash Equivalents PDFAngeline VergaraNo ratings yet

- Report No.08 Angel Marie Butsayo and Alaica Dannieca TambisDocument40 pagesReport No.08 Angel Marie Butsayo and Alaica Dannieca TambisCamille EscoteNo ratings yet

- CH 1 - Cash FlowDocument7 pagesCH 1 - Cash Flow李承翰No ratings yet

- Meaning of CashDocument22 pagesMeaning of CashShashi Kant SinghNo ratings yet

- Portfolio Management - Part 2: Portfolio Management, #2From EverandPortfolio Management - Part 2: Portfolio Management, #2Rating: 5 out of 5 stars5/5 (9)

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Liabilities Arising From Participating in A Specific Market-Waste Electrical and Electronic EquipmentDocument6 pagesLiabilities Arising From Participating in A Specific Market-Waste Electrical and Electronic EquipmentYtb AccntNo ratings yet

- Extinguishing Financial Liabilities With Equity Instruments: Ifric 19Document8 pagesExtinguishing Financial Liabilities With Equity Instruments: Ifric 19Ytb AccntNo ratings yet

- Making Materiality Judgements: IFRS Practice Statement 2Document44 pagesMaking Materiality Judgements: IFRS Practice Statement 2Ytb AccntNo ratings yet

- Hedges of A Net Investment in A Foreign Operation: Ifric 16Document14 pagesHedges of A Net Investment in A Foreign Operation: Ifric 16Ytb AccntNo ratings yet

- Noli Me Tangere-WPS OfficeDocument10 pagesNoli Me Tangere-WPS OfficeYtb AccntNo ratings yet

- Editorial Corrections - May 2019 - v4 - 127Document4 pagesEditorial Corrections - May 2019 - v4 - 127Ytb AccntNo ratings yet

- Existentialism QuestionsDocument18 pagesExistentialism QuestionsYtb AccntNo ratings yet

- Module 7 - Statement of Cash Flows: Ifrs Foundation: Training Material For The Ifrs® For SmesDocument73 pagesModule 7 - Statement of Cash Flows: Ifrs Foundation: Training Material For The Ifrs® For SmesYtb AccntNo ratings yet

- Risk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24Document3 pagesRisk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24anon_355962815100% (1)

- INB 372 Final ProjectDocument17 pagesINB 372 Final ProjectAniruddha Islam Khan DeshNo ratings yet

- Joint Ventures Between Private Equity Funds and Shipping CompaniesDocument3 pagesJoint Ventures Between Private Equity Funds and Shipping CompaniesShelly WuNo ratings yet

- Templeton Global Bond Fund: Key Investor InformationDocument2 pagesTempleton Global Bond Fund: Key Investor Informationspsc059891No ratings yet

- Security Analysis (Book)Document3 pagesSecurity Analysis (Book)LinaNo ratings yet

- ABC Brochure and Executive LeadershipDocument5 pagesABC Brochure and Executive Leadershipangel.miguele0% (1)

- Grow Your Wealth - 095904Document23 pagesGrow Your Wealth - 095904Amenye IssahNo ratings yet

- Exercise 3: Part I. Multiple ChoiceDocument3 pagesExercise 3: Part I. Multiple ChoiceAnwar AdemNo ratings yet

- Corporate Governance - Christine Mallin - Role of Institutional Investors in Corporate GovernanceDocument3 pagesCorporate Governance - Christine Mallin - Role of Institutional Investors in Corporate GovernanceUzzal Sarker - উজ্জ্বল সরকারNo ratings yet

- Masbate Polytechnic and Development College, Inc.: VisionDocument7 pagesMasbate Polytechnic and Development College, Inc.: VisionRobelyn Fababier VeranoNo ratings yet

- BTG Pactual - LocawebDocument6 pagesBTG Pactual - LocawebV Borges EngenhariaNo ratings yet

- Debt and Equity FinancingDocument4 pagesDebt and Equity FinancingGrace MutheuNo ratings yet

- Fin420 Financial Management NotesDocument286 pagesFin420 Financial Management NotesAthirah RoslanNo ratings yet

- Assignment 1 1Document2 pagesAssignment 1 1Fizza Jaffery100% (1)

- Fugro 2013 PDFDocument214 pagesFugro 2013 PDFJasper Laarmans Teixeira de MattosNo ratings yet

- BPC Annual Report 2010 PDFDocument38 pagesBPC Annual Report 2010 PDFSonam PhuntshoNo ratings yet

- Neraca PT Adaro Energy TBKDocument11 pagesNeraca PT Adaro Energy TBKDINANNo ratings yet

- Algebra Word Problems - Worksheet 8 - Interest ProblemsDocument28 pagesAlgebra Word Problems - Worksheet 8 - Interest ProblemsZeinab ElkholyNo ratings yet

- Finance Project ReportDocument7 pagesFinance Project Reporthamzaa mazharNo ratings yet

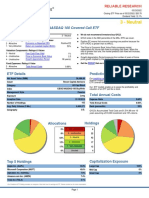

- 3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFDocument3 pages3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFphysicallen1791No ratings yet

- Investment and Speculation WorkDocument5 pagesInvestment and Speculation WorkWinifridaNo ratings yet

- Mutual Fund AssignmentDocument4 pagesMutual Fund AssignmentJenifer Chrisla TNo ratings yet

- Fin 515 Final ProjDocument5 pagesFin 515 Final Projitlnkicker100% (1)

- A Study On Savings and Investment Pattern of Salaried Women in Coimbatore DistrictDocument6 pagesA Study On Savings and Investment Pattern of Salaried Women in Coimbatore DistrictJananiNo ratings yet