You might also like

- The Merger or Insolvency Alternative in The Insurance IndustryDocument26 pagesThe Merger or Insolvency Alternative in The Insurance IndustrySrujan JNo ratings yet

- Risk Management With Help of InsuranceDocument22 pagesRisk Management With Help of InsuranceKurosaki IchigoNo ratings yet

- Lemonade TextDocument2 pagesLemonade TextSanti Hernandez RoncancioNo ratings yet

- Executive SummaryDocument53 pagesExecutive SummaryRohit VkNo ratings yet

- Longevity Risk: U.S. Insurers Tackle The Challenges of "Happily Ever After"Document5 pagesLongevity Risk: U.S. Insurers Tackle The Challenges of "Happily Ever After"api-227433089No ratings yet

- The Allocation of Catastrophe RiskDocument12 pagesThe Allocation of Catastrophe RiskAlex PutuhenaNo ratings yet

- InsuranceDocument53 pagesInsuranceRohit VkNo ratings yet

- Go Policy (Insurance Broker) : Student's Name: Student's Id: Date: Word Count: 2000Document12 pagesGo Policy (Insurance Broker) : Student's Name: Student's Id: Date: Word Count: 2000Mayur SoNo ratings yet

- Understanding Disaster Insurance: New Tools for a More Resilient FutureFrom EverandUnderstanding Disaster Insurance: New Tools for a More Resilient FutureNo ratings yet

- InsuranceDocument2 pagesInsuranceRavi AgarwalNo ratings yet

- Recruitment of Advisors in IciciDocument77 pagesRecruitment of Advisors in Icicipadamheena123No ratings yet

- Risk Management in Insurance PDFDocument51 pagesRisk Management in Insurance PDFathar100% (3)

- Risk Management Full NotesDocument40 pagesRisk Management Full NotesKelvin Namaona NgondoNo ratings yet

- Risk Management: How to Use Different Insurance to Your BenefitFrom EverandRisk Management: How to Use Different Insurance to Your BenefitNo ratings yet

- Insurance Industry in IndiaDocument91 pagesInsurance Industry in IndiaOne's JourneyNo ratings yet

- Dissertation ReinsuranceDocument4 pagesDissertation ReinsuranceWriteMyPaperSingapore100% (1)

- Insurance CompanyDocument54 pagesInsurance CompanyDhoni KhanNo ratings yet

- Risk Management in General Insurance BusDocument20 pagesRisk Management in General Insurance BusSuhas SiddarthNo ratings yet

- Avrupada Vicdani Ret Sorunu Istemden NorDocument36 pagesAvrupada Vicdani Ret Sorunu Istemden NorengineuurNo ratings yet

- Key Trends in Risk Management Further ReadingDocument6 pagesKey Trends in Risk Management Further ReadingSiddhantpsinghNo ratings yet

- Lazear20070411Document6 pagesLazear20070411losangelesNo ratings yet

- Insurance Companies As Financial Intermediaries: Risk and ReturnDocument54 pagesInsurance Companies As Financial Intermediaries: Risk and Returnfareha riazNo ratings yet

- SwissRe Understanding ReinsuranceDocument23 pagesSwissRe Understanding ReinsuranceHaldi Zusrijan PanjaitanNo ratings yet

- Insurance Concepts: January 1998Document18 pagesInsurance Concepts: January 1998sunny rockyNo ratings yet

- Sigma4 2014 enDocument36 pagesSigma4 2014 enHarry CerqueiraNo ratings yet

- The Economics of Catastrophe Risk InsuranceDocument19 pagesThe Economics of Catastrophe Risk Insurancelosangeles100% (1)

- Reinsurance: January 1998Document28 pagesReinsurance: January 1998Shubham KanojiaNo ratings yet

- Key Principles For Climate-Related Risk InsuranceDocument24 pagesKey Principles For Climate-Related Risk InsuranceCenter for American ProgressNo ratings yet

- EconomicsofRMI8 23 2018Document42 pagesEconomicsofRMI8 23 2018manisha_jha_11No ratings yet

- Statistical Concepts of A Priori and A Posteriori Risk Classification in InsuranceDocument38 pagesStatistical Concepts of A Priori and A Posteriori Risk Classification in InsuranceAhmed FenneurNo ratings yet

- Student Name: L. Sai Radha Krishna Topic Name: Reinsurance Related Laws ROLL - NO: 2016055 / ADocument15 pagesStudent Name: L. Sai Radha Krishna Topic Name: Reinsurance Related Laws ROLL - NO: 2016055 / Apradeep punuruNo ratings yet

- A Guide To Directors' Officers' Liability in Europe1 - tcm915-520123Document20 pagesA Guide To Directors' Officers' Liability in Europe1 - tcm915-520123AbhishekNo ratings yet

- Progressive Final PaperDocument16 pagesProgressive Final PaperJordyn WebreNo ratings yet

- POI MaterialDocument11 pagesPOI MaterialMukesh ChoudharyNo ratings yet

- Parametric Insurance For DisastersDocument6 pagesParametric Insurance For DisastersMohammed Touhami GOUASMINo ratings yet

- Reinsurance - Insuring The InsurerDocument61 pagesReinsurance - Insuring The Insurerkristokuns100% (1)

- Chapter - I Enterprise Risk Management: An IntroductionDocument37 pagesChapter - I Enterprise Risk Management: An IntroductionkshitijsaxenaNo ratings yet

- Risk Management: Alternative Risk Transfer: StructureDocument21 pagesRisk Management: Alternative Risk Transfer: StructureRADHIKAFULPAGARNo ratings yet

- 9629 PDFDocument12 pages9629 PDFfherremansNo ratings yet

- Commentary 454 0Document24 pagesCommentary 454 0Juan M. Nava DavilaNo ratings yet

- Financial Risks and Management: GlossaryDocument6 pagesFinancial Risks and Management: GlossaryhbNo ratings yet

- Document PDFDocument22 pagesDocument PDFMahedrz Gavali100% (1)

- Rahul File848848484884184Document61 pagesRahul File848848484884184Rahul GargNo ratings yet

- Actuary: Occupation Names Occupation Type Activity Sectors Description Competencies Education Required See Related JobsDocument13 pagesActuary: Occupation Names Occupation Type Activity Sectors Description Competencies Education Required See Related Jobsrohit utekarNo ratings yet

- FAIS AssignmentDocument17 pagesFAIS AssignmentSalman SaeedNo ratings yet

- Intern ReportDocument39 pagesIntern ReportSAKIB AL HASANNo ratings yet

- The Relation Between Capital Structure, Interest Rate Sensitivity, and Market Value in The Property-Liability Insurance IndustryDocument30 pagesThe Relation Between Capital Structure, Interest Rate Sensitivity, and Market Value in The Property-Liability Insurance Industrystephyl0722No ratings yet

- 120 Financial Planning Handbook PDPDocument10 pages120 Financial Planning Handbook PDPMoh. Farid Adi PamujiNo ratings yet

- Introduction PDF 2Document12 pagesIntroduction PDF 2Vijay GilatarNo ratings yet

- BMA 2020 Climate Change Survey ReportDocument16 pagesBMA 2020 Climate Change Survey ReportBernewsAdminNo ratings yet

- Blackbook Project On Insurance PDFDocument77 pagesBlackbook Project On Insurance PDFMayuri L0% (1)

- Blackbook Project On Insurance PDFDocument77 pagesBlackbook Project On Insurance PDFMayuri L100% (1)

- A Simulation of The Insurance Industry The ProblemDocument43 pagesA Simulation of The Insurance Industry The ProblemDavidon JaniNo ratings yet

- 14 Reinsurance PDFDocument28 pages14 Reinsurance PDFHalfani MoshiNo ratings yet

- 14 Reinsurance PDFDocument28 pages14 Reinsurance PDFHaider AliNo ratings yet

- EWS ReportDocument21 pagesEWS ReportppayonggNo ratings yet

- EY Credit Risk ManagementDocument10 pagesEY Credit Risk ManagementTroden MukwasiNo ratings yet

- Risk Management NotesDocument86 pagesRisk Management NotesbabuNo ratings yet

- Before Analysing Whether To Go For 1Document2 pagesBefore Analysing Whether To Go For 1Shivani KarkeraNo ratings yet

- Ship Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionDocument1 pageShip Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionShivani KarkeraNo ratings yet

- 2009 12 JRC White Certificates PDFDocument62 pages2009 12 JRC White Certificates PDFShivani KarkeraNo ratings yet

- The Ceiling On Project Capacity and Contracted Load RemovedDocument1 pageThe Ceiling On Project Capacity and Contracted Load RemovedShivani KarkeraNo ratings yet

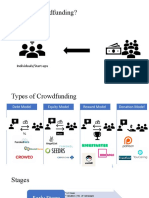

- What Is Crowdfunding?: Individuals/Start-ups FundingDocument3 pagesWhat Is Crowdfunding?: Individuals/Start-ups FundingShivani KarkeraNo ratings yet

- Caprica Energy and Its ChoicesDocument1 pageCaprica Energy and Its ChoicesShivani KarkeraNo ratings yet

- Pros and ConsDocument4 pagesPros and ConsShivani KarkeraNo ratings yet

- Energy Management 20-21Document11 pagesEnergy Management 20-21Shivani KarkeraNo ratings yet

- SITUATION ANALYSIS Morgan StanleyDocument1 pageSITUATION ANALYSIS Morgan StanleyShivani KarkeraNo ratings yet

- Real World Examples of Successful Crowdfunding Ventures: Social MediaDocument2 pagesReal World Examples of Successful Crowdfunding Ventures: Social MediaShivani KarkeraNo ratings yet

- Case Facts and AnalysisDocument2 pagesCase Facts and AnalysisShivani KarkeraNo ratings yet

- 2019 AnalysisDocument3 pages2019 AnalysisShivani KarkeraNo ratings yet

- Instruments For Financing Carbon Savings For Large ProgrammesDocument20 pagesInstruments For Financing Carbon Savings For Large ProgrammesShivani KarkeraNo ratings yet

- Template Positive Case With Exposure in Schools - 07202020Document2 pagesTemplate Positive Case With Exposure in Schools - 07202020Shivani KarkeraNo ratings yet

- Sample Notification Letters SchoolDocument3 pagesSample Notification Letters SchoolShivani KarkeraNo ratings yet

- Venture Capital Method With Multiple Rounds.Document4 pagesVenture Capital Method With Multiple Rounds.Shivani KarkeraNo ratings yet

- Venture Capital Method: Investment ScenariosDocument2 pagesVenture Capital Method: Investment ScenariosShivani KarkeraNo ratings yet

- PGDM - V - SM (Tri-IV) Course Outline - 2020 - 2.5 CreditDocument5 pagesPGDM - V - SM (Tri-IV) Course Outline - 2020 - 2.5 CreditShivani KarkeraNo ratings yet

- Adani Institute of Infrastructure Management (AIIM) PGDM 20219-21 (Trim. IV) Managing Energy BusinessDocument2 pagesAdani Institute of Infrastructure Management (AIIM) PGDM 20219-21 (Trim. IV) Managing Energy BusinessShivani KarkeraNo ratings yet

- Venture Capital Method With Dilution.Document6 pagesVenture Capital Method With Dilution.Shivani KarkeraNo ratings yet

- Adani Institute of Infrastructure Management Trimester IV Port and Shipping ManagementDocument3 pagesAdani Institute of Infrastructure Management Trimester IV Port and Shipping ManagementShivani KarkeraNo ratings yet

- Stats SumsDocument2 pagesStats SumsShivani KarkeraNo ratings yet

- Adani Institute of Infrastructure Management (AIIM) PGDM 20219-21 (Trim. IV) Global Carbon FinanceDocument3 pagesAdani Institute of Infrastructure Management (AIIM) PGDM 20219-21 (Trim. IV) Global Carbon FinanceShivani KarkeraNo ratings yet

- Learner Achievement VerificationDocument2 pagesLearner Achievement VerificationShivani KarkeraNo ratings yet

- Jetblue: Relevant Sustainability Leadership (A) : Situational AnalysisDocument1 pageJetblue: Relevant Sustainability Leadership (A) : Situational AnalysisShivani KarkeraNo ratings yet

- Transportation Policymaking in Beijing and Shanghai: Contributors, Obstacles and ProcessDocument23 pagesTransportation Policymaking in Beijing and Shanghai: Contributors, Obstacles and ProcessShivani KarkeraNo ratings yet